Pizza Hut 2002 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2002 Pizza Hut annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

|

|

conditions and events of default) similar to those set forth in the

Old Credit Facilities. Specifically, the New Credit Facility contains

financial covenants relating to maintenance of leverage and fixed

charge coverage ratios. The New Credit Facility also contains affir-

mative and negative covenants including, among other things,

limitations on certain additional indebtedness, guarantees of

indebtedness, cash dividends, aggregate non-U.S. investment and

certain other transactions as defined in the agreement.

Under the terms of the New Credit Facility, we may borrow up

to the maximum borrowing limit less outstanding letters of credit.

At December 28, 2002, our unused New Credit Facility totaled $0.9

billion, net of outstanding letters of credit of $0.2 billion. The inter-

est rate for borrowings under the New Credit Facility ranges from

1.00% to 2.00% over the London Interbank Offered Rate (“LIBOR”)

or 0.00% to 0.65% over an Alternate Base Rate, which is the

greater of the Prime Rate or the Federal Funds Effective Rate plus

1%. The exact spread over LIBOR or the Alternate Base Rate, as

applicable, will depend upon our performance under specified

financial criteria. Interest is payable at least quarterly. In the third

quarter of 2002, we capitalized debt issuance costs of approxi-

mately $9 million related to the New Credit Facility. The costs will

be amortized into interest expense over the life of the New Credit

Facility. At December 28, 2002, the weighted average contractual

interest rate on borrowings outstanding under the New Credit

Facility was 2.6%.

In 2002, we expensed facility fees of approximately $5 mil-

lion, which was comprised of $3 million related to the New Credit

Facility and $2 million related to the Old Credit Facilities, prior to

being replaced. In both 2001 and 2000, we expensed facility fees

of approximately $4 million related to the Old Credit Facilities.

In 1997, we filed a shelf registration statement with the

Securities Exchange Commission for offerings of up to $2 billion of

senior unsecured debt. In June 2002, we issued $400 million of

7.70% Senior Unsecured Notes due July 1, 2012 (the “2012 Notes”).

The net proceeds from the issuance of the 2012 Notes were used

to repay indebtedness under the New Credit Facility. Additionally,

we capitalized debt issuance costs of approximately $5 million

related to the 2012 Notes in the third quarter of 2002. The follow-

ing table summarizes all Senior Unsecured Notes issued under

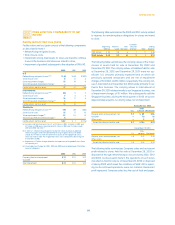

this shelf registration through December 28, 2002:

Maturity Principal Interest Rate

Issuance Date Date Amount Stated Effective(d)

May 1998 May 2005(a) $ 350 7.45% 7.62%

May 1998 May 2008(a) 250 7.65% 7.8 1%

April 2001 April 2006(b) 200 8.50% 9.04%

April 2001 April 2011(b) 650 8.88% 9.20%

June 2002 July 2012(c) 400 7.70% 8.04%

(a) Interest payments commenced on November 15, 1998 and are payable semi-annually

thereafter.

(b) Interest payments commenced on October 15, 2001 and are payable semi-annually

thereafter.

(c) Interest payments commenced on January 1, 2003 and are payable semi-annually

thereafter.

(d) Includes the effects of the amortization of any (1) premium or discount; (2) debt

issuance costs; and (3) gain or loss upon settlement of related treasury locks. Does

not include the effect of any interest rate swaps as described in Note 16.

We have $150 million remaining for issuance under the $2 billion

shelf registration.

As discussed in Note 4, upon the acquisition of YGR, we

assumed approximately $168 million in present value of future rent

obligations related to certain sale-leaseback agreements entered

into by YGR involving approximately 350 LJS units. As a result of

liens held by the buyer/lessor on certain personal property within

the units, the sale-leaseback agreements have been accounted

for as financings and are reflected as debt in our Consolidated

Financial Statements as of December 28, 2002. Rental payments

made under these agreements will be made on a monthly basis

through 2019 with an effective interest rate of approximately 11%.

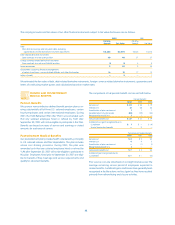

The annual maturities of long-term debt as of December 28,

2002, excluding capital lease obligations of $99 million and deriv-

ative instrument adjustments of $44 million, are as follows:

Year ended:

2003 $ 2

2004 2

2005 506

2006 203

2007 4

Thereafter 1,456

Total $2,17 3

Interest expense on short-term borrowings and long-term debt

was $180 million, $172 million and $190 million in 2002, 2001 and

2000, respectively. Net interest expense of $9 million on incre-

mental borrowings related to the AmeriServe bankruptcy

reorganization process was included in unusual items (income)

expense in 2000.

59.

Yum! Brands Inc.