Pizza Hut 2002 Annual Report Download - page 53

Download and view the complete annual report

Please find page 53 of the 2002 Pizza Hut annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

|

|

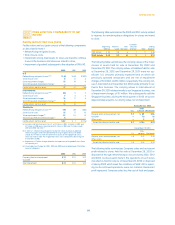

accounting for all business combinations and modifies the appli-

cation of the purchase accounting method. Goodwill represents

the excess of the cost of a business acquired over the net of the

amounts assigned to assets acquired, including identifiable intan-

gible assets, and liabilities assumed. SFAS 141 specifies criteria to

be used in determining whether intangible assets acquired in a

purchase method business combination must be recognized and

reported separately from goodwill. We base amounts assigned to

goodwill and other identifiable intangible assets on independent

appraisals or internal estimates.

The Company has also adopted SFAS No. 142, “Goodwill and

Other Intangible Assets” (“SFAS 142”). SFAS 142 eliminates the

requirement to amortize goodwill and indefinite-lived intangible

assets, addresses the amortization of intangible assets with a

defined life, and addresses impairment testing and recognition for

goodwill and indefinite-lived intangible assets. SFAS 142 applies

to goodwill and intangible assets arising from transactions com-

pleted both before and after its effective date. As a result of

adopting SFAS 142, we ceased amortization of goodwill and indef-

inite-lived intangible assets beginning December 30, 2001. Prior

to the adoption of SFAS 142, we amortized goodwill on a straight-

line basis up to 20 years and indefinite-lived intangible assets on

a straight-line basis over 3 to 40 years. Amortizable intangible

assets continue to be amortized on a straight-line basis over 3 to

40 years. As discussed above, we suspend amortization on those

intangible assets with a defined life that are allocated to restau-

rants that are held for sale.

In accordance with the requirements of SFAS 142, goodwill

has been assigned to reporting units for purposes of impairment

testing. Our reporting units are our operating segments in the U.S.

(see Note 23) and our business management units internationally

(typically individual countries). Goodwill impairment tests consist

of a comparison of each reporting unit’s fair value with its carry-

ing value. The fair value of a reporting unit is the amount for which

the unit as a whole could be sold in a current transaction between

willing parties. We generally estimate fair value based on dis-

counted cash flows. If the carrying value of a reporting unit

exceeds its fair value, goodwill is written down to its implied fair

value. As required by SFAS 142, we completed transitional impair-

ment tests of goodwill as of December 30, 2001, which indicated

that there was no impairment. We have selected the beginning of

our fourth quarter as the date on which to perform our ongoing

annual impairment test. As a result of the poor performance by

our Pizza Hut France reporting unit from the date of the transitional

impairment test through September 8, 2002 (the beginning of our

fourth quarter), goodwill assigned to that reporting unit of $5 mil-

lion was deemed impaired and written off in the fourth quarter.

See Note 12 for further discussion of SFAS 142.

Stock-Based Employee Compensation

At December 28, 2002, the Company had four stock-based

employee compensation plans in effect, which are described more

fully in Note 18. The Company accounts for those plans under the

recognition and measurement principles of APB Opinion No. 25,

“Accounting for Stock Issued to Employees,” and related

Interpretations. No stock-based employee compensation cost is

reflected in net income, as all options granted under those plans

had an exercise price equal to the market value of the underlying

common stock on the date of grant. The following table illustrates

the effect on net income and earnings per share if the Company

had applied the fair value recognition provisions of SFAS No. 123

“Accounting for Stock-Based Compensation,” to stock-based

employee compensation.

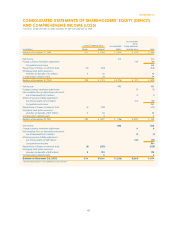

2002 2001 2000

Net Income, as reported $ 583 $ 492 $ 413

Deduct: Total stock-based employee

compensation expense determined

under fair value based method for

all awards, net of related tax effects (39) (37) (34)

Net Income, pro forma 544 455 379

Basic Earnings per Common Share

As reported $1.97 $ 1.68 $ 1.41

Pro forma 1.84 1.55 1.29

Diluted Earnings per Common Share

As reported $ 1.88 $ 1.62 $ 1.39

Pro forma 1.76 1.50 1.29

Derivative Financial Instruments

Our policy prohibits the use of derivative instruments for trading

purposes, and we have procedures in place to monitor and con-

trol their use. Our use of derivative instruments has included

interest rate swaps and collars, treasury locks and foreign cur-

rency forward contracts. In addition, on a limited basis we utilize

commodity futures and options contracts. Our interest rate and

foreign currency derivative contracts are entered into with finan-

cial institutions while our commodity derivative contracts are

exchange traded.

We account for derivative financial instruments in accordance

with SFAS No. 133, “Accounting for Derivative Instruments and

Hedging Activities” (“SFAS 133”). SFAS 133 requires that all deriva-

tive instruments be recorded on the Consolidated Balance Sheet

at fair value. The accounting for changes in the fair value (i.e., gains

or losses) of a derivative instrument is dependent upon whether

the derivative has been designated and qualifies as part of a

hedging relationship and further, on the type of hedging relation-

ship. For derivative instruments that are designated and qualify as

a fair value hedge, the gain or loss on the derivative instrument as

51.

Yum! Brands Inc.