Pizza Hut 2002 Annual Report Download - page 51

Download and view the complete annual report

Please find page 51 of the 2002 Pizza Hut annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

|

|

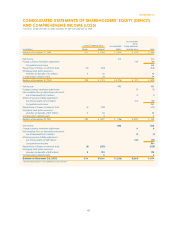

Reclassifications

We have reclassified certain items in the accompanying Consol-

idated Financial Statements and Notes thereto for prior periods to

be comparable with the classification we adopted for the fiscal

year ended December 28, 2002. These reclassifications had no

effect on previously reported net income.

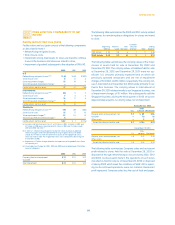

Franchise and License Operations

We execute franchise or license agreements for each unit which

sets out the terms of our arrangement with the franchisee or

licensee. Our franchise and license agreements typically require

the franchisee or licensee to pay an initial, non-refundable fee and

continuing fees based upon a percentage of sales. Subject to our

approval and payment of a renewal fee, a franchisee may gen-

erally renew the franchise agreement upon its expiration.

We recognize initial fees as revenue when we have per-

formed substantially all initial services required by the franchise

or license agreement, which is generally upon the opening of a

store. We recognize continuing fees as earned with an appropri-

ate provision for estimated uncollectible amounts, which is

included in franchise and license expenses. We recognize

renewal fees in income when a renewal agreement becomes

effective. We include initial fees collected upon the sale of a

restaurant to a franchisee in refranchising gains (losses). Fees for

development rights are capitalized and amortized over the life of

the development agreement.

We incur expenses that benefit both our franchise and license

communities and their representative organizations and our com-

pany operated restaurants. These expenses, along with other

costs of sales and servicing of franchise and license agreements

are charged to general and administrative expenses as incurred.

Certain direct costs of our franchise and license operations are

charged to franchise and license expenses. These costs include

provisions for estimated uncollectible fees, franchise and license

marketing funding, amortization expense for franchise related

intangible assets and certain other direct incremental franchise

and license support costs. Franchise and license expenses also

includes rental income from subleasing restaurants to franchisees

net of the related occupancy costs.

We monitor the financial condition of our franchisees and

licensees and record provisions for estimated losses on receiv-

ables when we believe that our franchisees or licensees are

unable to make their required payments. While we use the best

information available in making our determination, the ultimate

recovery of recorded receivables is also dependent upon future

economic events and other conditions that may be beyond our

control. Included in franchise and license expenses are provisions

for uncollectible franchise and license receivables of $15 million,

$24 million and $30 million in 2002, 2001 and 2000, respectively.

Direct Marketing Costs

We report substantially all of our direct marketing costs in occu-

pancy and other operating expenses. We charge direct marketing

costs to expense ratably in relation to revenues over the year in

which incurred and, in the case of advertising production costs, in

the year first shown. Deferred direct marketing costs, which are

classified as prepaid expenses, consist of media and related

advertising production costs which will generally be used for the

first time in the next fiscal year. To the extent we participate in

advertising cooperatives, we expense our contributions as

incurred. At the end of 2002 and 2001, we had deferred market-

ing costs of $8 million and $2 million, respectively. Our advertising

expenses were $384 million, $328 million and $325 million in

2002, 2001 and 2000, respectively.

Research and Development Expenses

Research and development expenses, which we expense as

incurred, were $23 million in 2002, $23 million in 2001 and $24

million in 2000.

Impairment or Disposal of Long-Lived Assets

Effective December 30, 2001, the Company adopted SFAS No. 144,

“Accounting for the Impairment or Disposal of Long-Lived Assets”

(“SFAS 144”). SFAS 144 retained many of the fundamental provisions

of SFAS No. 121, “Accounting for the Impairment of Long-Lived

Assets and for Long-Lived Assets to Be Disposed Of” (“SFAS 121”),

but resolved certain implementation issues associated with that

Statement. The adoption of SFAS 144 did not have a material

impact on the Company’s consolidated results of operations.

In accordance with SFAS 144, we review our long-lived assets

related to each restaurant to be held and used in the business,

including any allocated intangible assets subject to amortization,

semi-annually for impairment, or whenever events or changes in

circumstances indicate that the carrying amount of a restaurant

may not be recoverable. We evaluate restaurants using a “two-

year history of operating losses” as our primary indicator of

potential impairment. Based on the best information available, we

write down an impaired restaurant to its estimated fair market

value, which becomes its new cost basis. We generally measure

estimated fair market value by discounting estimated future cash

flows. In addition, when we decide to close a restaurant it is

reviewed for impairment and depreciable lives are adjusted. The

impairment evaluation is based on the estimated cash flows from

continuing use through the expected disposal date and the

expected terminal value.

Store closure costs include costs of disposing of the assets as

well as other facility-related expenses from previously closed

stores. These store closure costs are expensed as incurred.

Additionally, at the date the closure is considered probable, we

record a liability for the net present value of any remaining oper-

ating lease obligations subsequent to the expected closure date,

net of estimated sublease income, if any.

49.

Yum! Brands Inc.