Pizza Hut 2002 Annual Report Download - page 52

Download and view the complete annual report

Please find page 52 of the 2002 Pizza Hut annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

|

|

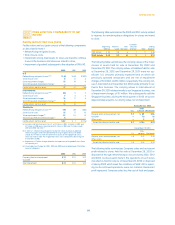

Refranchising gains (losses) includes the gains or losses from

the sales of our restaurants to new and existing franchisees and

the related initial franchise fees, reduced by transaction costs and

direct administrative costs of refranchising. In executing our refran-

chising initiatives, we most often offer groups of restaurants. We

classify restaurants as held for sale and suspend depreciation and

amortization when (a) we make a decision to refranchise; (b) the

stores can be immediately removed from operations; (c) we have

begun an active program to locate a buyer; (d) significant changes

to the plan of sale are not likely; and (e) the sale is probable within

one year. We recognize losses on refranchisings when the restau-

rants are classified as held for sale. We recognize gains on

restaurant refranchisings when the sale transaction closes, the

franchisee has a minimum amount of the purchase price in at-risk

equity, and we are satisfied that the franchisee can meet its finan-

cial obligations. If the criteria for gain recognition are not met, we

defer the gain to the extent we have a remaining financial expo-

sure in connection with the sales transaction. Deferred gains are

recognized when the gain recognition criteria are met or as our

financial exposure is reduced. When we make a decision to retain

a store previously held for sale, we revalue the store at the lower

of its (a) net book value at our original sale decision date less nor-

mal depreciation and amortization that would have been recorded

during the period held for sale or (b) its current fair market value.

This value becomes the store’s new cost basis. We charge (or

credit) any difference between the store’s carrying amount and its

new cost basis to refranchising gains (losses). When we make a

decision to close a store previously held for sale, we reverse any

previously recognized refranchising loss and then record impair-

ment and store closure costs as described above. Refranchising

gains (losses) also include charges for estimated exposures

related to those partial guarantees of franchisee loan pools and

contingent lease liabilities which arose from refranchising activi-

ties. These exposures are more fully discussed in Note 24.

SFAS 144 also requires the results of operations of a compo-

nent entity that is classified as held for sale or has been disposed

of be reported as discontinued operations in the Consolidated

Statements of Income if certain conditions are met. These condi-

tions include elimination of the operations and cash flows of the

component entity from the ongoing operations of the Company

and no significant continuing involvement by the Company in the

operations of the component entity after the disposal transaction.

The results of operations of stores meeting both these conditions

that were disposed of in 2002 or classified as held for sale at

December 28, 2002 were not material for any of the three years

ended December 28, 2002.

Considerable management judgment is necessary to esti-

mate future cash flows, including cash flows from continuing use,

terminal value, closure costs, sublease income, and refranchising

proceeds. Accordingly, actual results could vary significantly from

our estimates.

Impairment of Investments in Unconsolidated Affiliates

Our methodology for determining and measuring impairment of

our investments in unconsolidated affiliates is similar to the

methodology we use for our restaurants except we use cash flows

after interest and taxes instead of cash flows before interest and

taxes as we use for our restaurants. Also, we record impairment

charges related to investments in unconsolidated affiliates if cir-

cumstances indicate that a decrease in the value of an investment

has occurred which is other than temporary.

Considerable management judgment is necessary to esti-

mate future cash flows. Accordingly, actual results could vary

significantly from our estimates.

Cash and Cash Equivalents

Cash equivalents represent funds we have temporarily invested

(with original maturities not exceeding three months) as part of man-

aging our day-to-day operating cash receipts and disbursements.

Inventories

We value our inventories at the lower of cost (computed on the

first-in, first-out method) or net realizable value.

Property, Plant and Equipment

We state property, plant and equipment at cost less accumulated

depreciation and amortization, impairment writedowns and val-

uation allowances. We calculate depreciation and amortization

on a straight-line basis over the estimated useful lives of the assets

as follows: 5 to 25 years for buildings and improvements, 3 to 20

years for machinery and equipment and 3 to 7 years for capital-

ized software costs. As discussed above, we suspend depreciation

and amortization on assets related to restaurants that are held for

sale.

Internal Development Costs and Abandoned Site Costs

We capitalize direct costs associated with the site acquisition and

construction of a Company unit on that site, including direct inter-

nal payroll and payroll-related costs. Only those site-specific

costs incurred subsequent to the time that the site acquisition is

considered probable are capitalized. We consider acquisition

probable upon final site approval. If we subsequently make a

determination that a site for which internal development costs

have been capitalized will not be acquired or developed, any pre-

viously capitalized internal development costs are expensed and

included in general and administrative expenses.

Goodwill and Intangible Assets

The Company has adopted SFAS No. 141, “Business Combinations”

(“SFAS 141”). SFAS 141 requires the use of the purchase method of

50.