Pizza Hut 2001 Annual Report Download - page 53

Download and view the complete annual report

Please find page 53 of the 2001 Pizza Hut annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

|

|

51

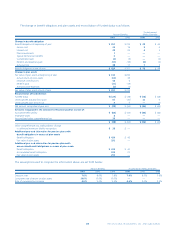

The annual maturities of long-term debt through 2006 and

thereafter, excluding capital lease obligations and the derivative

instrument adjustments, are 2002 – $537 million; 2003 – $1 mil-

lion; 2004 – $1 million; 2005 – $351 million; 2006 – $200 million

and $900 million thereafter.

LEASES

We have non-cancelable commitments under both capital and

long-term operating leases, primarily for our restaurants. Capital

and operating lease commitments expire at various dates through

2087 and, in many cases, provide for rent escalations and

renewal options. Most leases require us to pay related executory

costs, which include property taxes, maintenance and insurance.

Future minimum commitments and amounts to be

received as lessor or sublessor under non-cancelable leases are

set forth below:

Commitments Lease Receivables

Direct

Capital Operating Financing Operating

2002 $ 11 $ 221 $ 2 $ 9

2003 12 203 2 8

2004 10 180 1 7

2005 9 160 1 7

2006 8 134 1 6

Thereafter 87 893 8 33

$137 $1,791 $15 $ 70

At year-end 2001, the present value of minimum payments

under capital leases was $79 million.

The details of rental expense and income are set forth below:

2001 2000 1999

Rental expense

Minimum $ 283 $ 253 $ 263

Contingent 10 28 28

$ 293 $ 281 $ 291

Minimum rental income $14 $18 $20

Contingent rentals are generally based on sales levels in excess

of stipulated amounts contained in the lease agreements.

During 2001, we entered into sales-leaseback transactions

involving 17 of our restaurants. Under the transactions, the

restaurants were sold for approximately $18 million and have

been leased back for initial terms of 15 years. These leasebacks

have been accounted for as operating leases. The future lease

payments are included in the above tables. Gains on the sales,

which were not significant, were deferred and will be amortized

to rent expense over the initial term of the leases.

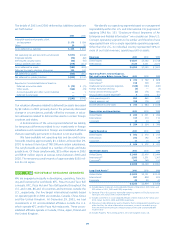

13

NOTE

FINANCIAL INSTRUMENTS

Derivative Instruments

Interest Rates

We enter into interest rate swaps, collars and forward rate

agreements with the objective of reducing our exposure to inter-

est rate risk and lowering interest expense for a portion of our

debt. Under the contracts, we agree with other parties to

exchange, at specified intervals, the difference between variable

rate and fixed rate amounts calculated on a notional principal

amount. At December 29, 2001 and December 30, 2000 we

had outstanding pay-variable interest rate swaps with notional

amounts of $350 million. These swaps have reset dates and float-

ing rate indices which match those of our underlying fixed-rate

debt and have been designated as fair value hedges of a por-

tion of that debt. As the swaps qualify for the short-cut method

under SFAS 133 no ineffectiveness has been recorded. The fair

value of these swaps as of December 29, 2001 was approxi-

mately $36 million and has been included in Other assets. The

portion of this fair value which has not yet been recognized as

a reduction to interest expense (approximately $34 million at

December 29, 2001) has been included in Long-term debt.

At December 29, 2001 and December 30, 2000, we also

had outstanding pay-fixed interest rate swaps with notional

amounts of $650 million and $450 million, respectively. These

swaps have been designated as cash flow hedges of a portion

of our variable-rate debt. As the critical terms of the swaps and

hedged interest payments are the same, we have determined

that the swaps are completely effective in offsetting the vari-

ability in cash flows associated with interest payments on that

debt due to interest rate fluctuations.

During 2000, we entered into interest rate collars to reduce

interest rate sensitivity on a portion of our variable rate bank

debt. Interest rate collars effectively lock in a range of interest

rates by establishing a cap and floor. Reset dates and the float-

ing index on the collars match those of the underlying bank

debt. If interest rates remain within the collared cap and floor,

no payments are made. If rates rise above the cap level, we

receive a payment. If rates fall below the floor level, we make a

payment. At December 29, 2001 and December 30, 2000, we

did not have any outstanding interest rate collars.

Foreign Exchange

We enter into foreign currency forward contracts with the objec-

tive of reducing our exposure to cash flow volatility arising from

foreign currency fluctuations associated with certain foreign cur-

rency denominated financial instruments, the majority of which

are intercompany short-term receivables and payables. The

notional amount, maturity date, and currency of these contracts

14

NOTE