Pizza Hut 2001 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 2001 Pizza Hut annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

|

|

45

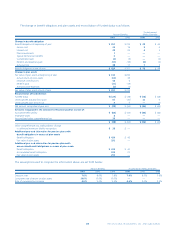

Stock-Based Employee Compensation

We measure stock-based employee compensation cost for finan-

cial statement purposes in accordance with Accounting

Principles Board (“APB”) Opinion No. 25, “Accounting for Stock

Issued to Employees,” and its related interpretations. We include

pro forma information in Note 16 as required by SFAS No. 123,

“Accounting for Stock-Based Compensation” (“SFAS 123”).

Accordingly, we measure compensation cost for stock option

grants to employees as the excess of the average market price

of the Common Stock at the grant date over the amount the

employee must pay for the stock. Our policy is to generally grant

stock options at the average market price of the underlying

Common Stock at the date of grant.

Derivative Financial Instruments

Our policy prohibits the use of derivative instruments for trad-

ing purposes, and we have procedures in place to monitor and

control their use. Our use of derivative instruments has included

interest rate swaps, collars, forward rate agreements and for-

eign currency forward contracts. In addition, we utilize on a

limited basis, commodity futures and options contracts. Our

interest rate and foreign currency derivative contracts are

entered into with financial institutions while our commodity

derivative contracts are exchange traded.

Effective December 31, 2000, we adopted SFAS No. 133,

“Accounting for Derivative Instruments and Hedging Activities”

(“SFAS 133”). SFAS 133 requires that all derivative instruments

be recorded on the Consolidated Balance Sheet at fair value.

The accounting for changes in the fair value (i.e., gains or losses)

of a derivative instrument is dependent upon whether the deriv-

ative has been designated and qualifies as part of a hedging

relationship and further, on the type of hedging relationship.

For derivative instruments that are designated and qualify as a

fair value hedge, the gain or loss on the derivative instrument

as well as the offsetting gain or loss on the hedged item attrib-

utable to the hedged risk are recognized in the results of

operations. For derivative instruments that are designated and

qualify as a cash flow hedge, the effective portion of the gain

or loss on the derivative instrument is reported as a component

of other comprehensive income (loss) (“OCI”) and reclassified

into earnings in the same period or periods during which the

hedged transaction affects earnings. Any ineffective portion of

the gain or loss on the derivative instrument is recorded in the

results of operations immediately. For derivative instruments not

designated as hedging instruments, the gain or loss is recog-

nized in the results of operations immediately. The cumulative

effect of adoption of SFAS 133 was insignificant. For fiscal years

prior to the adoption of SFAS 133, our treatment of derivative

instruments was as described in the following paragraphs.

We recognized the interest differential to be paid or

received on interest rate swap and forward rate agreements as

an adjustment to interest expense as the differential occurred.

We recognized the interest differential to be paid or received on

an interest rate collar as an adjustment to interest expense when

the interest rate fell below or rose above the collared range. We

reflected the recognized interest differential not yet settled in

cash in the accompanying Consolidated Balance Sheets as a cur-

rent receivable or payable.

Each period, we recognized in income foreign exchange

gains and losses on forward contracts that were designated and

effective as hedges of foreign currency receivables or payables

as the differential occurred. These gains or losses were largely

offset by the corresponding gain or loss recognized in income

on the currency translation of the receivable or payable, as both

amounts were based upon the same exchange rates. We

reflected the recognized foreign currency differential for forward

contracts not yet settled in cash on the accompanying

Consolidated Balance Sheets each period as a current receivable

or payable. Each period, we recognized in income the change in

fair value of foreign exchange gains and losses on forward con-

tracts that were entered into to mitigate the foreign exchange

risk of certain forecasted foreign currency denominated royalty

receipts. We reflected the fair value of these forward contracts

not yet settled on the Consolidated Balance Sheets as a current

receivable or payable. If a foreign currency forward contract was

terminated prior to maturity, the gain or loss recognized upon

termination was immediately recognized in income.

We deferred gains and losses on futures and options con-

tracts that were designated and effective as hedges of future

commodity purchases and included them in the cost of the

related raw materials when purchased. Changes in the value of

futures and options contracts that we used to hedge compo-

nents of our commodity purchases were highly correlated to

changes in the value of the purchased commodity attributable

to the hedged component.

New Accounting Pronouncements Not Yet Adopted

In 2001, the Financial Accounting Standards Board (“FASB”)

issued SFAS 141, which supersedes APB Opinion No. 16,

“Business Combinations.” SFAS 141 eliminates the pooling-of-

interests method of accounting for business combinations and

modifies the application of the purchase accounting method.

SFAS 141 also specifies criteria intangible assets acquired in a

purchase method business combination must meet to be rec-

ognized and reported separately from goodwill. The provisions

of SFAS 141 were effective for transactions accounted for using

the purchase method that were completed after June 30, 2001.