Pentax 2008 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2008 Pentax annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

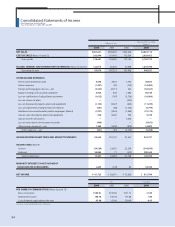

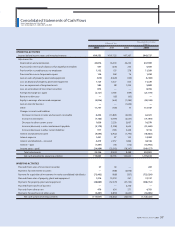

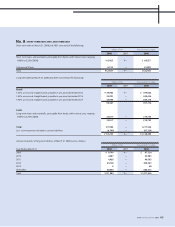

Notes to Consolidated Financial Statements

Hoya Corporation and Subsidiaries

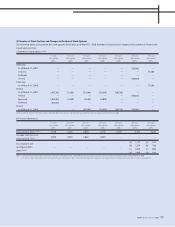

No. 7 NET ASSETS

“Net assets” comprises four subsections, which are shareholders’

equity, accumulated gains (losses) from revaluation and translation

adjustments, stock subscription rights and minority interests.

The Japanese Corporate Law (“the Law”) became effective on

May 1, 2006, replacing the Japanese Commercial Code (“the Code”).

Under Japanese laws and regulations, the entire amount paid for

new shares is required to be designated as common stock. However, a

company may, by a resolution of the Board of Directors, designate an

amount not exceeding one-half of the price of the new shares as

additional paid-in capital, which is included in capital surplus.

Under the Law, in cases where a dividend distribution of surplus is

made, the smaller of an amount equal to 10% of the dividend or the

excess, if any, of 25% of common stock over the total of additional

paid-in capital and legal earnings reserve must be set aside as

additional paid-in capital or legal earnings reserve. Legal earnings

reserve is included in retained earnings in the accompanying

consolidated balance sheets.

Under the Code, companies were required to set aside an amount

equal to at least 10% of the aggregate amount of cash dividends and

other cash appropriations as legal earnings reserve until the total of

legal earnings reserve and additional paid-in capital equaled 25% of

common stock.

Under the Code, legal earnings reserve and additional paid-in

capital could be used to eliminate or reduce a deficit by a resolution of

the shareholders’ meeting or could be capitalized by a resolution of the

Board of Directors. Under the Law, both of these appropriations

generally require a resolution of the shareholders’ meeting.

Additional paid-in capital and legal earnings reserve may not be

distributed as dividends. Under the Code, however, on condition that

the total amount of legal earnings reserve and additional paid in capital

remained equal to or exceeded 25% of common stock, they were

available for distribution by resolution of the shareholders’ meeting.

Under the Law, all additional paid-in capital and all legal earnings

reserve may be transferred to other capital surplus and retained

earnings, respectively, which are potentially available for dividends.

The maximum amount that the Company can distribute as

dividends is calculated based on the non-consolidated financial

statements of the Company in accordance with Japanese laws and

regulations.

Since the Company introduced the committees system in 2003,

dividends may be paid upon resolution of the Board of Directors,

subject to certain limitations imposed by the Law. Interim dividends

may also be paid upon resolution of the Board of Directors, subject to

certain limitations imposed by the Law.

On May 22, 2008, the Board of Directors resolved cash dividends

amounting to ¥15,150 million ($151,213 thousand). Such

appropriations have not been accrued in the consolidated financial

statements as of March 31, 2008. Such appropriations are recognized

when the Board of Directors resolves them.

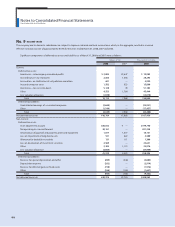

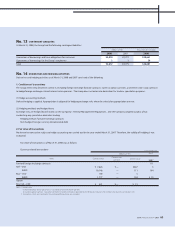

2008

Discount rate

Expected rate of return on plan assets

Amortization of unrecognized prior service cost

(Straight-line method)

Recognition of unrecognized acturial gain

(Straight-line method from the following fiscal year of recognition)

Mainly 2.0%

Mainly 3.5%

Mainly 10 years

Mainly 10 years

2007

—

—

—

—

Assumptions used for the years ended March 31, 2008 and 2007 are set forth as follows:

The estimated amount of all retirement benefits to be paid at the future retirement date is allocated equally to each service year using the estimated

number of total service years.

64