Oracle 2005 Annual Report Download - page 56

Download and view the complete annual report

Please find page 56 of the 2005 Oracle annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

|

|

Table of Contents

As permitted by Statement 123, we accounted for share-based payments to employees using Opinion 25’s intrinsic value method up to May 31, 2006. Although

the adoption of Statement 123(R)’s fair value method will have no adverse impact on our balance sheet or total cash flows, it will affect our net income and

earnings per share. The actual effects of adopting Statement 123(R) will depend on numerous factors including the amounts of share-based payments granted in

the future, the valuation model we use to value future share-based payments to employees and estimated forfeiture rates. We estimate that stock-based

compensation expense will reduce diluted earnings per share by $0.02 to $0.03 in fiscal 2007 as a result of the adoption of Statement 123(R).

Accounting Changes and Error Corrections: On June 7, 2005, the FASB issued Statement No. 154, Accounting Changes and Error Corrections, a replacement

of APB Opinion No. 20, Accounting Changes, and Statement No. 3, Reporting Accounting Changes in Interim Financial Statements. Statement 154 changes the

requirements for the accounting for and reporting of a change in accounting principle. Previously, most voluntary changes in accounting principles required

recognition of a cumulative effect adjustment within net income of the period of the change. Statement 154 requires retrospective application to prior periods’

financial statements, unless it is impracticable to determine either the period-specific effects or the cumulative effect of the change. Statement 154 is effective for

accounting changes made in fiscal years beginning after December 15, 2005; however, the Statement does not change the transition provisions of any existing

accounting pronouncements. We do not believe adoption of Statement 154 will have a material effect on our consolidated financial position, results of operations

or cash flows.

Accounting for Uncertainty in Income Taxes: On July 13, 2006, the FASB issued Interpretation No. 48, Accounting for Uncertainty in Income Taxes—an

interpretation of FASB Statement No. 109. Interpretation 48 clarifies the accounting for uncertainty in income taxes recognized in an entity’s financial statements

in accordance with Statement 109 and prescribes a recognition threshold and measurement attribute for financial statement disclosure of tax positions taken or

expected to be taken on a tax return. Additionally, Interpretation 48 provides guidance on derecognition, classification, interest and penalties, accounting in

interim periods, disclosure and transition. Interpretation 48 is effective for fiscal years beginning after December 15, 2006, with early adoption permitted. We are

currently evaluating whether the adoption of Interpretation 48 will have a material effect on our consolidated financial position, results of operations or cash

flows.

Item 7A. Quantitative and Qualitative Disclosures About Market Risk

Interest Income Rate Risk. Based on our intentions regarding our investments, we classify our investments as either held-to-maturity or available-for-sale.

Held-to-maturity investments are reported on the balance sheet at amortized cost. Available-for-sale securities are reported at market value. Auction rate

securities, which are classified as available-for-sale, are reported on the balance sheet at par value, which equals market value, as the rate on such securities

re-sets generally every 7 to 28 days. As a majority of our investments are held-to-maturity, interest rate movements do not affect the balance sheet valuation of

the fixed income investments. Changes in the overall level of interest rates affect our interest income that is generated from our investments. For fiscal 2006, total

interest income was $170 million with investments yielding an average 3.04% on a worldwide basis. This interest rate level was up approximately 111 basis

points from 1.93% for fiscal 2005. If overall interest rates fell by a similar amount (111 basis points) in fiscal 2007, our interest income would decline

approximately $64 million, assuming consistent investment levels.

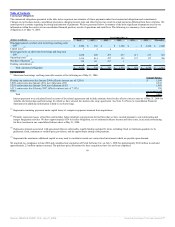

The table below presents the cash, cash equivalent and marketable securities balances and the related weighted average interest rates for our investment portfolio

at May 31, 2006. The cash, cash equivalent and marketable securities balances approximate fair value at May 31, 2006:

(Dollars in millions)

Amortized

Principal Amount

Weighted Average

Interest Rate

Cash and cash equivalents $ 6,659 4.08%

Marketable securities 946 2.18%

Total cash, cash equivalents and marketable securities $ 7,605 3.84%

53

Source: ORACLE CORP, 10-K, July 21, 2006 Powered by Morningstar® Document Research℠