Oracle 2005 Annual Report Download - page 31

Download and view the complete annual report

Please find page 31 of the 2005 Oracle annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

|

|

Table of Contents

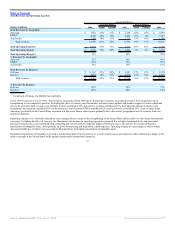

when we receive final acceptance from the customer. When total cost estimates exceed revenues, we accrue for the estimated losses immediately using cost

estimates that are based upon an average fully burdened daily rate applicable to the consulting organization delivering the services. The complexity of the

estimation process and factors relating to the assumptions, risks and uncertainties inherent with the application of the proportional performance method of

accounting affect the amounts of revenue and related expenses reported in our consolidated financial statements. A number of internal and external factors can

affect our estimates, including labor rates, utilization and efficiency variances and specification and testing requirement changes.

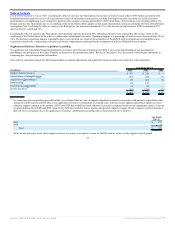

If an arrangement does not qualify for separate accounting of the software license and consulting transactions, then new software license revenue is generally

recognized together with the consulting services based on contract accounting using either the percentage-of-completion or completed-contract method. Contract

accounting is applied to any arrangements: (1) that include milestones or customer specific acceptance criteria that may affect collection of the software license

fees; (2) where services include significant modification or customization of the software; (3) where significant consulting services are provided for in the

software license contract without additional charge or are substantially discounted; or (4) where the software license payment is tied to the performance of

consulting services.

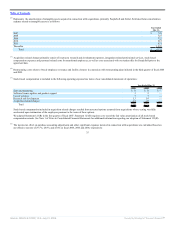

On Demand is comprised of Oracle On Demand and Advanced Customer Services. Oracle On Demand provides multi-featured software and hardware

management and maintenance services for our database, middleware and applications software. Advanced Customer Services are earned by providing customers

configuration and performance analysis, personalized support and annual on-site technical services. Revenues from On Demand services are recognized over the

term of the service contract, which is generally one year.

Education revenues include instructor-led, media-based and internet-based training in the use of our products. Education revenues are recognized as the classes or

other education offerings are delivered.

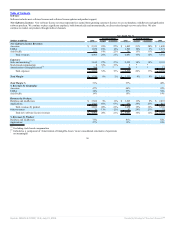

For arrangements with multiple elements, we allocate revenue to each element of a transaction based upon its fair value as determined by “vendor specific

objective evidence.” Vendor specific objective evidence of fair value for all elements of an arrangement is based upon the normal pricing and discounting

practices for those products and services when sold separately and for software license updates and product support services, is additionally measured by the

renewal rate offered to the customer. We may modify our pricing practices in the future, which could result in changes in our vendor specific objective evidence

of fair value for these undelivered elements. As a result, our future revenue recognition for multiple element arrangements could differ significantly from our

historical results.

We defer revenue for any undelivered elements, and recognize revenue when the product is delivered or over the period in which the service is performed, in

accordance with our revenue recognition policy for such element. If we cannot objectively determine the fair value of any undelivered element included in

bundled software and service arrangements, we defer revenue until all elements are delivered and services have been performed, or until fair value can

objectively be determined for any remaining undelivered elements. When the fair value of a delivered element has not been established, we use the residual

method to record revenue if the fair value of all undelivered elements is determinable. Under the residual method, the fair value of the undelivered elements is

deferred and the remaining portion of the arrangement fee is allocated to the delivered elements and is recognized as revenue.

Substantially all of our software license arrangements do not include acceptance provisions. However, if acceptance provisions exist as part of public policy, for

example in agreements with government entities when acceptance periods are required by law, or within previously executed terms and conditions that are

referenced in the current agreement and are short-term in nature, we provide for a sales return allowance in accordance with FASB Statement No. 48, Revenue

Recognition when Right of Return Exists. If acceptance provisions are long-term in nature or are not included as standard terms of an arrangement or if we cannot

reasonably estimate the incidence of returns, revenue is recognized upon the earlier of receipt of written customer acceptance or expiration of the acceptance

period.

28

Source: ORACLE CORP, 10-K, July 21, 2006 Powered by Morningstar® Document Research℠