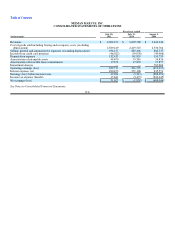

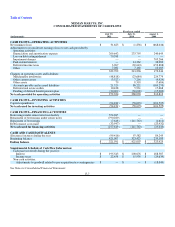

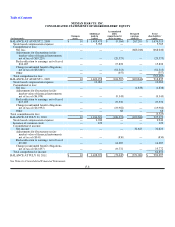

Neiman Marcus 2010 Annual Report Download - page 108

Download and view the complete annual report

Please find page 108 of the 2010 Neiman Marcus annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

|

|

Table of Contents

enterprise fair value of each of our reporting units to its recorded carrying value. We estimate the enterprise fair value based on

discounted cash flow techniques (Level 3). Inputs to the valuation model include:

• estimated future cash flows;

• growth assumptions for future revenues as well as future gross margin rates, expense rates, capital expenditures and

other estimates; and

• rates, based on our estimated weighted average cost of capital, used to discount our estimated future cash flow

projections to their present value (or estimated fair value).

The projected sales, gross margin and expense rate and capital expenditures assumptions are based on our annual business

plan or other forecasted results. Discount rates reflect market-based estimates of the risks associated with the projected cash flows

directly resulting from the use of those assets in our operations. The estimates of the enterprise fair values of our reporting units are

based on the best information available as of the date of the assessment.

If the recorded carrying value of a reporting unit exceeds its estimated enterprise fair value in the first step, a second step is

performed in which we allocate the enterprise fair value to the fair value of the reporting unit's net assets. The second step of the

impairment testing process requires, among other things, the estimation of the fair values of substantially all of our tangible and

intangible assets. Any enterprise fair value in excess of amounts allocated to such net assets represents the implied fair value of

goodwill for that reporting unit. If the recorded goodwill balance for a reporting unit exceeds the implied fair value of goodwill, an

impairment charge is recorded to write goodwill down to its fair value.

The goodwill impairment testing process is subject to inherent uncertainties and subjectivity. The use of different

assumptions, estimates or judgments in either step of the process, including with estimation of the projected future cash flows of our

reporting units, the discount rate used to reduce such projected future cash flows to their net present value, and the estimation of the

fair value of the reporting units' tangible and intangible assets and liabilities, could materially increase or decrease the fair value of the

reporting units' net assets and, accordingly, could materially increase or decrease any related impairment charge. We believe our

estimates are appropriate based upon current market conditions and the best information available at the assessment date. However,

future impairment charges could be required if we do not achieve our current revenue and profitability projections or the weighted

average cost of capital increases.

As more fully described in Note 4 of the Notes to Consolidated Financial Statements, we recorded significant impairment

charges in fiscal year 2009 to writedown our tradenames and goodwill to estimated fair value. No additional impairment charges were

recorded in either fiscal year 2010 or fiscal year 2011. At July 30, 2011, the estimated fair values of each of our tradenames exceeded

their recorded values by over 20%. The estimated fair values of our Bergdorf Goodman and Direct Marketing reporting units also

exceeded their net carrying values by over 20% while the estimated fair value of our Neiman Marcus reporting unit exceeded its net

carrying value by approximately 6%.

Leases. We lease certain retail stores and office facilities. Stores we own are often subject to ground leases. The terms of

our real estate leases, including renewal options, range from six to 121 years. Most leases provide for monthly fixed minimum rentals

or contingent rentals based upon sales in excess of stated amounts and normally require us to pay real estate taxes, insurance, common

area maintenance costs and other occupancy costs. For leases that contain predetermined, fixed calculations of minimum rentals, we

recognize rent expense on a straight-line basis over the lease term. We recognize contingent rent expenses when it is probable that the

sales thresholds will be reached during the year.

We receive allowances from developers related to the construction of our stores. We record these allowances as deferred real

estate credits, which we recognize as a reduction of rent expense on a straight-line basis over the lease term beginning with the date

the Company takes possession of the leased asset. We received construction allowances aggregating $10.5 million in fiscal year 2011,

$14.4 million in fiscal year 2010 and $10.0 million in fiscal year 2009.

Benefit Plans. We sponsor a noncontributory defined benefit pension plan (Pension Plan), an unfunded supplemental

executive retirement plan (SERP Plan) which provides certain employees additional pension benefits and a postretirement plan

providing eligible employees limited postretirement health care benefits (Postretirement Plan). In calculating our obligations and

related expense, we make various assumptions and estimates, after consulting with outside actuaries and advisors. The annual

determination of expense involves calculating the estimated total benefits ultimately payable to plan participants. We use the

projected unit credit method in recognizing pension liabilities. The Pension and SERP Plans are valued annually as of the end of each

fiscal year. As of the third quarter of fiscal year 2010, benefits offered to all employees under our Pension Plan and SERP Plan have

been frozen.

F-12