National Grid 2010 Annual Report Download - page 39

Download and view the complete annual report

Please find page 39 of the 2010 National Grid annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

|

|

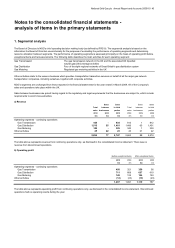

National Grid Gas plc Annual Report and Accounts 2009/10 37

New IFRS accounting standards and interpretations not yet adopted

The following standards and interpretations were not effective for the year ended 31 March 2010. None of these are expected to have

a material impact on NGG’s consolidated results or assets and liabilities.

IFRS 3R on business combinations Makes a number of changes to the accounting for business combinations, including requirements that all

payments to purchase a business are to be recorded at fair value at the acquisition date, with some contingent

payments subsequently remeasured at fair value through income; an option to calculate goodwill based on the

parent’s share of net assets only or to include goodwill related to the minority interest; and a requirement that

all transaction costs be expensed. IFRS 3R has been adopted by the Company with effect from 1 April 2010.

IAS 27R on consolidated and individual

financial statements

Requires the effects of all transactions with non-controlling interests to be recorded in equity if there is no

change in control. The revised standard also specifies the accounting when control is lost. IAS 27R has been

adopted by the Company with effect from 1 April 2010.

Amendment to IAS 39 Financial

Instruments: Recognition and

measurement on eligible

hedged items

Prohibits designating inflation as a hedgeable component of an instrument, unless cash flows relating to the

separate inflation component are contractual and also prohibits the designation of a purchased option in its

entirety as the hedge of a one-sided risk in a forecast transaction. The amendment to IAS 39 has been adopted

by the Company with effect from 1 April 2010.

Revised IFRS 1 on first-time adoption

of IFRS

Changes the structure, while retaining the substance, of the previously issued version of IFRS 1. The revised

version of IFRS 1 has been adopted by the Company with effect from 1 April 2010.

IFRIC 17 on distribution of non-cash

assets to owners

Requires such a distribution to be measured at the fair value of the asset and any difference between the

carrying amount of the asset and its fair value to be recognised in profit or loss. IFRIC 17 has been adopted by

the Company with effect from 1 April 2010.

Improvements to IFRS 2009 Contains amendments to various existing standards. The amendments have been adopted by the Company

with effect from 1 April 2010.

Amendment to IFRS 2 on group cash

settled share based payments

Clarifies the scope and accounting for group cash settled share based payment transactions in separate or

individual financial statements when there is no obligation to settle the share based payment transaction. The

amendment to IFRS 2 has been adopted by the Company with effect from 1 April 2010.

Amendment to IFRS 1 on first time

adoption of IFRS

Provides additional exemptions for first time adopters. The amendment to IFRS 1 will be adopted by the

Company with effect from 1 April 2010, subject to endorsement by the European Union.

Amendment to IAS 32 on classification

of rights issues

Defines as an equity instrument a financial instrument that gives the holder the right to acquire a fixed number

of the entity’s equity instruments for a fixed amount of any currency, if the financial instrument is offered pro

rata to all existing owners of the same class of non-derivative equity instruments. The amendment to IAS 32

has been adopted by the Company with effect from 1 April 2010.

Revised IAS 24 on related

party disclosures

Simplifies the definition of a related party and provides a partial exemption for government-related entities. The

revised version of IAS 24 will be adopted by the Company with effect from 1 April 2011, subject to endorsement

by the European Union.

IFRS 9 on financial instruments Requires that financial assets should be classified as at either amortised cost or fair value on the basis of the

entity’s business model and contractual cash flows. IFRS 9 will be adopted by the Company with effect from 1

April 2013, subject to endorsement by the European Union.

IFRIC 19 on extinguishing financial

liabilities with equity instruments

Clarifies that equity instruments issued to extinguish a financial liability should be measured at fair value, unless

fair value cannot reasonably be determined in which case the fair value of the liabilities extinguished should be

used. IFRIC 19 will be adopted by the Company with effect from 1 April 2011, subject to endorsement by the

European Union.

Amendment to IFRIC 14 on

prepayments of a minimum funding

requirement

Permits an entity to treat early payments of contributions to cover a minimum funding requirement as an asset.

The amendment to IFRIC 14 will be adopted by the Company with effect from 1 April 2011, subject to

endorsement by the European Union.

Amendment to IFRS 1 on comparative

IFRS 7 disclosures

Provides limited disclosure exemptions in respect of financial instruments for first-time adopters of IFRS. The

amendment to IFRS 1 will be adopted by the Company with effect from 1 April 2011, subject to endorsement by

the European Union.