National Grid 2010 Annual Report Download - page 26

Download and view the complete annual report

Please find page 26 of the 2010 National Grid annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

|

|

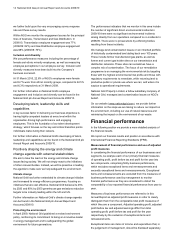

24 National Grid Gas plc Annual Report and Accounts 2009/10

changes to credit ratings and by prolonged periods of

market volatility or illiquidity.

We are subject to certain covenants and restrictions in relation

to our listed debt securities and our bank lending facilities. In

addition, restrictions imposed by regulators may also limit the

manner in which we service the financial requirements of our

business.

Our business is financed through cash generated from ongoing

operations and the capital markets, particularly the long-term

debt capital markets. The maturity and repayment profile of

debt we use to finance investments often does not correlate to

cash flows from our assets. As a result we access commercial

paper and money markets and longer-term bank and capital

markets as sources of finance. Some of the debt we issue is

rated by credit rating agencies and changes to these ratings

may affect both our borrowing capacity and the cost of those

borrowings. As evidenced during recent periods, financial

markets can be subject to periods of volatility and shortages of

liquidity and if we were unable to access the capital markets or

other sources of finance at competitive rates for a prolonged

period, our cost of financing may increase, the uncommitted

and discretionary elements of our proposed capital investment

programme may need to be reconsidered and the manner in

which we implement our strategy may need to reassessed. The

occurrence of any such events could have a material adverse

impact on our business, results of operations and prospects.

Our results of operations could be affected by deflation or

inflation.

Our income under our price controls is linked to the retail price

index. Therefore if the UK economy suffers from a prolonged

period of deflation, our revenues may decrease, which may not

be offset by reductions in operating costs. Conversely during a

period of inflation our operating costs may increase without a

corresponding increase in the retail price index and therefore

without a corresponding increase in revenues. Such increased

costs may materially adversely affect our results of operations.

In addition, even where increased costs are recoverable under

our price controls there may be a delay in our ability to recover

our increased costs.

Future funding requirements of our pension schemes

could materially adversely affect our results of operations.

Substantially all of our employees are members of a defined

benefit pension scheme where the scheme assets are held

independently of our own financial resources. Estimates of the

amount and timing of future funding for this scheme are based

on various actuarial assumptions and other factors including,

among other things, the actual and projected market

performance of the scheme assets, future long-term bond

yields, average life expectancies and relevant legal

requirements. The impact of these assumptions and other

factors may require us to make additional contributions to these

pension schemes which, to the extent they are not recoverable

under our price controls, could materially adversely affect our

results of operations and financial condition.

New or revised accounting standards, rules and

interpretations could have an adverse effect on our

reported financial results. Changes in law and accounting

standards could increase our effective rate of tax.

The accounting treatment under International Financial

Reporting Standards (IFRS), as adopted by the European

Union, of, among other things, replacement expenditure, rate

regulated entities, pension and post-retirement benefits,

derivative financial instruments and commodity contracts,

significantly affect the way we report our financial position and

results of operations. New or revised standards and

interpretations may be issued which could have a significant

impact on the financial results and financial position that we

report. The effective rate of tax we pay may be influenced by a

number of factors including changes in law and accounting

standards, the results of which could increase that rate and

therefore have a material adverse and therefore have a material

adverse impact on our results of operations.

Customers and counterparties to our transactions may fail

to perform their obligations, which could harm our results

of operations.

Our operations are exposed to the risk that customers and

counterparties to our transactions that owe us money or

commodities will not perform their obligations, which could

materially adversely affect our financial position. This risk is

most significant where there are concentrations of receivables

from utilities and their affiliates, as well as industrial customers

and other purchasers and may also arise where customers are

unable to pay us as a result of increasing commodity prices or

adverse economic conditions.

The loss of key personnel or the inability to attract, train or

retain qualified personnel could affect our ability to

implement our strategy and have a material adverse effect

on our business, financial condition, results of operations

and prospects.

Our ability to implement our long-term business strategy

depends on the capabilities and performance of our personnel.

Loss of key personnel or an inability to attract, train or retain

appropriately qualified personnel (in particular for technical

positions where availability of appropriately qualified personnel

may be limited) could affect our ability to implement our long-

term business strategy and may have a material adverse effect

on our business, financial condition, results of operations and

prospects.