National Grid 2010 Annual Report Download - page 27

Download and view the complete annual report

Please find page 27 of the 2010 National Grid annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

|

|

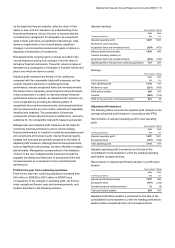

National Grid Gas plc Annual Report and Accounts 2009/10 25

Accounting policies

Basis of accounting

The consolidated financial statements present the results of

NGG for the years ended 31 March 2010 and 2009 and

financial position as at 31 March 2010 and 2009. They have

been prepared using the accounting policies shown, in

accordance with International Financial Reporting Standards

(IFRS).

In complying with IFRS, we are also complying with the version

of IFRS that has been endorsed by the European Union for use

by listed companies.

IFRS differ from UK Generally Accepted Accounting Principles

(UK GAAP).

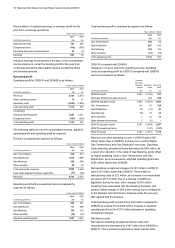

Choices permitted under IFRS

IFRS provide certain options available within accounting

standards. Material choices NGG has made, and continues to

make, include the following:

Presentation formats

We use the nature of expense method for our income statement

and total our balance sheet to net assets and total equity.

In the income statement, we present subtotals of total operating

profit, profit before tax and profit from continuing operations,

together with additional subtotals excluding exceptional items

and remeasurements. Exceptional items and remeasurements

are presented on the face of the income statement.

Capital contributions

Contributions received prior to 1 July 2009 towards capital

expenditure are recorded as deferred income and amortised in

line with depreciation on the associated asset.

Financial instruments

We normally opt to apply hedge accounting in most

circumstances where this is permitted.

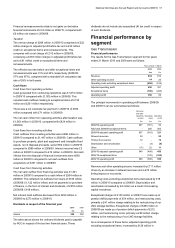

Critical accounting policies

The application of accounting principles requires us to make

estimates, judgments and assumptions that may affect the

reported amounts of assets, liabilities, revenue and expenses

and the disclosure of contingent assets and liabilities in the

accounts. On an ongoing basis, we evaluate our estimates

using historical experience, consultation with experts and other

methods that we consider reasonable in the particular

circumstances to ensure compliance with IFRS. Actual results

may differ significantly from our estimates, the effect of which

will be recognised in the period in which the facts that give rise

to the revision become known.

Certain accounting policies, described below, have been

identified as critical accounting policies, as these policies

involve particularly complex or subjective decisions or

assessments. The discussion of critical accounting policies

below should be read in conjunction with the description of our

accounting policies set out in our consolidated financial

statements.

Estimated economic lives of property, plant and equipment

The reported amounts for depreciation of property, plant and

equipment and amortisation of non-current intangible assets

can be materially affected by the judgments exercised in

determining their estimated economic lives.

Carrying value of assets and potential for impairments

The carrying value of assets recorded in the consolidated

balance sheet could be materially reduced if an impairment

were to be assessed as being required. Impairment reviews are

carried out when a change in circumstance is identified that

indicates an asset might be impaired. An impairment review

involves calculating either or both of the fair value or the value-

in-use of an asset or group of assets and comparing with the

carrying value in the balance sheet.

These calculations involve the use of assumptions as to the

price that could be obtained for, or the future cash flows that will

be generated by, an asset or group of assets, together with an

appropriate discount rate to apply to those cash flows.

Revenue

Revenue includes an assessment of transportation services

supplied to customers between the date of the last invoice and

the year end. Changes to the estimate of the transportation

services supplied during this period would have an impact on

the reported results.

Estimates of unbilled revenues amounted to £184 million at 31

March 2010 compared with £189 million at 31 March 2009.

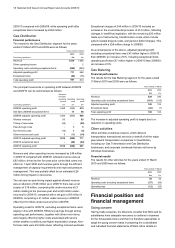

Assets and liabilities carried at fair value

Certain financial investments and derivative financial

instruments are carried in the balance sheet at their fair value

rather than historical cost.

The fair value of financial investments is based on market

prices, as are those of derivative financial instruments where

market prices exist. Other derivative financial instruments are

valued using financial models, which include judgements on, in

particular, future movements in exchange and interest rates.

Hedge accounting

Derivative financial instruments are used to hedge certain

economic exposures arising from movements in exchange and

interest rates or other factors that could affect either the value

of the Company’s assets or liabilities or affect future cash flows.

Movements in the fair values of derivative financial instruments

may be accounted for using hedge accounting where the

relevant eligibility, documentation and effectiveness testing

requirements are met. If a hedge does not meet the strict

criteria for hedge accounting, or where there is ineffectiveness

or partial ineffectiveness, then the movements will be recorded

in the income statement immediately instead of being

recognised in the statement of recognised income and expense

or by being offset by adjustments to the carrying value of debt.

Pensions

Defined benefit pension obligations are accounted for as if the

National Grid UK Pension Scheme were a defined contribution

scheme as there is neither a contractual arrangement, nor a