Motorola 2015 Annual Report Download - page 75

Download and view the complete annual report

Please find page 75 of the 2015 Motorola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

|

|

74

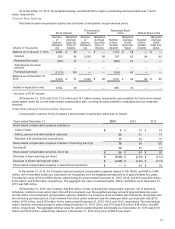

Investment Policy

The individual plans have adopted an investment policy designed to meet or exceed the expected rate of return on plan

assets assumption. To achieve this, the plans retain professional advisors and investment managers that invest plan assets into

various classes including, but not limited to, equity and fixed income securities, cash, cash equivalents, commodities, hedge

funds, infrastructure/utilities, insurance contracts, leveraged loan funds and real estate. The Company uses long-term historical

actual return experience with consideration of the expected investment mix of the plans’ assets, as well as future estimates of

long-term investment returns, to develop its expected rate of return assumption used in calculating the net periodic cost. The

individual plans have target mixes for these asset classes, which are readjusted periodically when an asset class weighting

deviates from the target mix, with the goal of achieving the required return at a reasonable risk level.

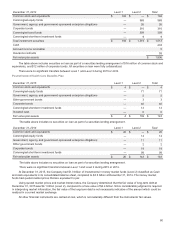

The weighted-average asset allocations by asset categories for all pension and the Postretirement Health Care Benefits

plans were as follows:

All Pension Benefit Plans

Postretirement Health Care

Benefits Plan

December 31 2015 2014 2015 2014

Target Mix:

Equity securities 37% 41% 36% 37%

Fixed income securities 45% 44% 42% 42%

Cash and other investments 18% 15% 22% 21%

Actual Mix:

Equity securities 37% 43% 37% 20%

Fixed income securities 44% 44% 41% 20%

Cash and other investments 19% 13% 22% 60%

Within the equity securities asset class, the investment policy provides for investments in a broad range of publicly-traded

securities including both domestic and foreign equities. Within the fixed income securities asset class, the investment policy

provides for investments in a broad range of publicly-traded debt securities including: U.S. Treasury issues, corporate debt

securities, mortgage and asset-backed securities, as well as foreign debt securities. In the cash and other investments asset

class, investments may include, but are not limited to: cash, cash equivalents, commodities, hedge funds, infrastructure/utilities,

insurance contracts, leveraged loan funds and real estate.

Cash Funding

The Company made $3 million of contributions to its U.S. Pension Benefit Plans during 2015, compared to $1.1 billion

contributed in 2014. The Company contributed $10 million to its Non U.S. Pension Benefit Plans during 2015, compared to $237

million contributed in 2014. The Company made no contributions to its Postretirement Health Care Benefits Plan in 2015 or

2014.

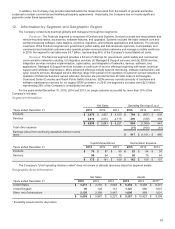

Expected Future Benefit Payments

The following benefit payments are expected to be paid:

Year

U.S. Pension

Benefit Plans

Non U.S.

Pension

Benefit Plans

Postretirement

Health Care

Benefits Plan

2016 $94$47$19

2017 108 46 18

2018 124 52 17

2019 141 55 16

2020 162 62 15

2021-2025 1,128 376 63

Other Benefit Plans

Split-Dollar Life Insurance Arrangements

The Company maintains a number of endorsement split-dollar life insurance policies on now-retired officers under a plan

that was frozen prior to December 31, 2004. The Company had purchased the life insurance policies to insure the lives of

employees and then entered into a separate agreement with the employees that split the policy benefits between the Company

and the employee. Motorola Solutions owns the policies, controls all rights of ownership, and may terminate the insurance

policies. To effect the split-dollar arrangement, Motorola Solutions endorsed a portion of the death benefits to the employee and

upon the death of the employee, the employee’s beneficiary typically receives the designated portion of the death benefits