Motorola 2015 Annual Report Download - page 21

Download and view the complete annual report

Please find page 21 of the 2015 Motorola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

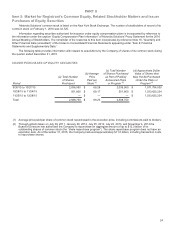

|

|

20

It may be difficult for us to recruit and retain the types of engineers and other highly-skilled employees that are

necessary to remain competitive and layoffs of such skilled employees as a result of divestitures, restructuring

activities or cost reductions may benefit our competitors.

Competition for key technical personnel in high-technology industries is intense. As we expand our solutions and services

business we have an even greater demand for technical personnel in areas like software development than we have historically

had and competition for such resources is greater. We believe that our future success depends in large part on our continued

ability to hire, assimilate, retain and leverage the skills of qualified engineers and other highly-skilled personnel needed to

develop successful new products or services. We may not be as successful as our competitors at recruiting, assimilating,

retaining and utilizing these highly-skilled personnel, which could have a negative impact on our business. In addition, as we

have divested businesses and restructured our operations we have, in some cases, had to layoff engineers and other highly

skilled employees. If these employees were to go to work for our competitors it could have a negative impact on our business.

We may not have the ability to settle the principal amount of the $1 billion of 2% Senior Convertible Notes (the "Senior

Convertible Notes") in cash in the event of conversion or to repurchase the Senior Convertible Notes upon the

occurrence of a fundamental change.

Our Senior Convertible Notes are convertible any time on or after two years from their issuance date, except in certain

limited circumstances. In the event of conversion, the Company currently intends to settle the principal amount of the Senior

Convertible Notes in cash.

If we do not have adequate cash available, either from cash on hand, funds generated from operations or existing

financing arrangements, or we cannot obtain additional financing arrangements, we may not be able to settle the principal

amount of the Senior Convertible Notes in cash and, in the case of settlement of conversion elections, will be required to settle

the principal amount of the Senior Convertible Notes in stock. If we settle any portion of the principal amount of the Senior

Convertible Notes in stock, it will result in immediate, and possibly material, dilution to the interests of existing security holders.

Following any conclusion that we no longer have the ability to settle the Senior Convertible Notes in cash, we will be

required on a going forward basis to change our accounting policy for earnings per share from the treasury stock method to the

if-converted method. Earnings per share will most likely be lower under the if-converted method as compared to the treasury

stock method.

Our ability to repurchase the Senior Convertible Notes in cash upon the occurrence of a fundamental change or make any

other required payments may be limited by law or the terms of other agreements relating to our indebtedness outstanding at the

time. Our failure to repurchase the Senior Convertible Notes when required would result in an event of default with respect to the

Senior Convertible Notes and may constitute an event of default or prepayment under, or result in the acceleration of the

maturity of, our then-existing indebtedness.

The accounting for convertible debt securities that may be settled in cash or in shares of common stock could have a

material effect on our reported financial results.

Under U.S. GAAP, an entity must separately account for the debt component and the embedded conversion option of

convertible debt instruments that may be settled entirely or partially in cash or in shares of common stock upon conversion, such

as our Senior Convertible Notes, in a manner that reflects the issuer’s effective interest cost. The fair value of the embedded

conversion option is classified as an addition to stockholder’s equity. The difference between book carrying cost and face value

of the debt represents a non-cash discount. This difference will be amortized into interest expense over the estimated life of the

Senior Convertible Notes using the effective yield method. As a result, we will be required to record a greater amount of non-

cash interest expense as a result of the amortization of their discount over the term of the Senior Convertible Notes. Accordingly,

we will report lower net income because of the recognition of both the current period’s discount amortization and the Senior

Convertible Notes’ coupon interest, which could adversely affect the trading price of our shares of common stock and the trading

price (if any) of the Senior Convertible Notes.

Under certain circumstances, convertible debt instruments (such as the Senior Convertible Notes) that may be settled

entirely or partially in cash are evaluated for their impact on earnings per share utilizing the treasury stock method, the effect of

which is that the shares issuable upon conversion of the Senior Convertible Notes are not included in the calculation of diluted

earnings per share except to the extent that the conversion value of the Senior Convertible Notes exceeds their principal

amount. Under the treasury stock method the number of shares outstanding for purposes of calculating diluted earnings per

share includes the number of shares that would be required to settle the excess of the conversion value of the Senior

Convertible Notes, if any, over the principal amounts of the Senior Convertible Notes (which would be settled in cash). The

conversion value of the Senior Convertible Notes will exceed the principal amount of the notes to the extent the trading price of a

share of our stock exceeds $68.50. We intend to settle the principal amount of the convertible notes in cash. However, we may

not have access to the capital markets for financing on acceptable terms and conditions, particularly if our credit ratings are

downgraded. Accordingly, we may be forced to fully settle the Senior Convertible Notes in shares of common stock upon

conversion, the effect of which would cause the dilutive impact to earnings per share to be significantly in excess of the dilutive

impact reflected by the treasury stock method.