MasterCard 2015 Annual Report Download - page 85

Download and view the complete annual report

Please find page 85 of the 2015 MasterCard annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

-

97

-

98

-

99

-

100

-

101

-

102

|

|

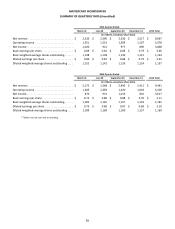

MASTERCARD INCORPORATED

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS – (Continued)

79

class litigation. As of December 31, 2015 and December 31, 2014, MasterCard had $541 million and $540 million, in the qualified

cash settlement fund classified as restricted cash on its balance sheet. The class settlement agreement provided for a return to

the defendants of a portion of the class cash settlement fund, based upon the percentage of purchase volume represented by

the opt-out merchants. This resulted in $164 million from the cash settlement fund being returned to MasterCard in January

2014 and reclassified at that time from restricted cash to cash and cash equivalents. In the fourth quarter of 2013, MasterCard

recorded an incremental net pre-tax charge of $95 million related to the opt-out merchants, representing a change in its estimate

of probable losses relating to these matters. MasterCard has executed settlement agreements with a number of opt-out

merchants and no adjustment to the amount previously recorded was deemed necessary. As of December 31, 2015, MasterCard

had accrued a liability of $709 million as a reserve for both the merchant class litigation and the filed and anticipated opt-out

merchant cases.

The portion of the accrued liability relating to the opt-out merchants does not represent an estimate of a loss, if any, if the opt-

out merchant matters were litigated to a final outcome, in which case MasterCard cannot estimate the potential liability.

MasterCard’s estimate involves significant judgment and may change depending on progress in settlement negotiations or

depending upon decisions in any opt-out merchant cases. In addition, in the event that the merchant class litigation settlement

approval is overturned, a negative outcome in the litigation could have a material adverse effect on MasterCard’s results of

operations, financial position and cash flows.

Canada. In December 2010, a proposed class action complaint was commenced against MasterCard in Quebec on behalf of

Canadian merchants. That suit essentially repeated the allegations and arguments of a previously filed application by the Canadian

Competition Bureau to the Canadian Competition Tribunal (dismissed in MasterCard’s favor) related to certain MasterCard rules

related to point-of-sale acceptance, including the “honor all cards” and “no surcharge” rules. The suit sought compensatory and

punitive damages in unspecified amounts, as well as injunctive relief. In the first half of 2011, additional purported class action

lawsuits containing similar allegations to the Quebec class action were commenced in British Columbia and Ontario against

MasterCard, Visa and a number of large Canadian financial institutions. The British Columbia suit seeks compensatory damages

in unspecified amounts, and the Ontario suit seeks compensatory damages of $5 billion. The British Columbia and Ontario suits

also seek punitive damages in unspecified amounts, as well as injunctive relief, interest and legal costs. The Quebec suit was

later amended to include the same defendants and similar claims as in the British Columbia and Ontario suits. With respect to

the status of the proceedings: (1) the Quebec suit has been stayed, (2) the Ontario suit is being temporarily suspended while the

British Columbia suit proceeds, and (3) the British Columbia appellate court issued an order in August 2015 allowing several of

the merchants’ claims to proceed on a class basis. Additional proposed class action complaints have been filed in Saskatchewan

and Alberta with claims that largely mirror those in the British Columbia and Ontario suits. If the class action lawsuits are ultimately

successful, negative decisions could have a significant adverse impact on the revenue of MasterCard’s Canadian customers and

on MasterCard’s overall business in Canada and could result in substantial damage awards.

Europe. In July 2015, the European Commission issued a Statement of Objections related to MasterCard’s interregional

interchange fees and central acquiring rules within the European Economic Area. The Statement of Objections, which follows

an investigation opened in 2013, includes preliminary conclusions concerning the anticompetitive effects of these practices. The

European Commission has indicated it intends to seek fines if these conclusions are subsequently confirmed. Although the

Statement of Objections does not quantify the level of fines, it is possible that they could be substantial. MasterCard would not

expect fines to be imposed if it agrees with the Commission to business practice changes that address the Commission’s concerns.

In the United Kingdom, beginning in May 2012, a number of retailers filed claims against MasterCard seeking damages for alleged

anti-competitive conduct with respect to MasterCard’s cross-border interchange fees and its U.K. and Ireland domestic

interchange fees. More than 30 different retailers have filed claims or threatened litigation. Approximately 30 additional

merchants have filed or threatened litigation with respect to interchange rates in Europe (“Pan-European claimants”). Although

the U.K. and Pan-European claimants have not quantified the full extent of their compensatory and punitive damages, their

purported damages exceed $2 billion. In June 2015, MasterCard entered into a settlement with one of these merchants for $61

million, recorded as a provision for litigation settlement. MasterCard has submitted statements of defense to the remaining

retailers’ claims disputing liability and damages. A trial for liability and damages for one of the U.K. merchant cases commenced

in January 2016. The merchant in that action has claimed compensatory damages of approximately $300 million, and is also

seeking costs and punitive damages. MasterCard has argued that there is no liability or damage to the merchant. The trial is

expected to conclude in March 2016, with a decision expected later in the year.

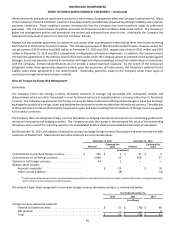

ATM Non-Discrimination Rule Surcharge Complaints

In October 2011, a trade association of independent Automated Teller Machine (“ATM”) operators and 13 independent ATM

operators filed a complaint styled as a class action lawsuit in the U.S. District Court for the District of Columbia against both