MasterCard 2015 Annual Report Download - page 51

Download and view the complete annual report

Please find page 51 of the 2015 MasterCard annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

|

|

45

We do not record U.S. income tax expense for foreign earnings which we intend to reinvest indefinitely to expand our international

operations. We consider business plans, planning opportunities, and expected future outcomes in assessing the needs for future

expansion and support of our international operations. If our business plans change or our future outcomes differ from our

expectations, U.S. income tax expense and our effective tax rate could increase or decrease in that period.

Valuation of Assets

The valuation of assets acquired in a business combination and asset impairment reviews require the use of significant estimates

and assumptions. The acquisition method of accounting for business combinations requires the Company to estimate the fair

value of assets acquired, liabilities assumed, and any non-controlling interest in the acquiree to properly allocate purchase price

consideration between assets that are depreciated and amortized from goodwill. Impairment testing for assets, other than

goodwill and indefinite-lived intangible assets, requires the allocation of cash flows to those assets or group of assets and if

required, an estimate of fair value for the assets or group of assets. The Company’s estimates are based upon assumptions

believed to be reasonable, but which are inherently uncertain and unpredictable. These valuations require the use of

management’s assumptions, which would not reflect unanticipated events and circumstances that may occur.

We evaluate goodwill and indefinite-lived intangible assets for impairment on an annual basis or sooner if indicators of impairment

exist. Goodwill is tested for impairment at the reporting unit level. The impairment evaluation utilizes a quantitative assessment

using a two-step impairment test. The first step is to compare the reporting unit’s carrying value, including goodwill, to the fair

value. The Company uses a market approach for estimating the fair value of its reporting unit. If the fair value exceeds the carrying

value, then no potential impairment is considered to exist. If the carrying value exceeds the fair value, the second step is performed

to determine if the implied fair value of the reporting unit’s goodwill exceeds the carrying value of the reporting unit. An

impairment charge would be recorded if the carrying value exceeds the implied fair value. The impairment test for indefinite-

lived intangible assets consists of a qualitative assessment to evaluate all relevant events and circumstances that could affect

the significant inputs used to determine the fair value of indefinite-lived intangible assets. In performing the qualitative

assessment, we consider relevant events and conditions, including but not limited to, macroeconomic trends, industry and market

conditions, overall financial performance, cost factors, company-specific events, and legal and regulatory factors. If the qualitative

assessment indicates that it is more likely than not that the fair value of the indefinite-lived intangible asset is less than their

carrying amounts, the Company must perform a quantitative impairment test.

ITEM 7A. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET

RISK

Market risk is the potential for economic losses to be incurred on market risk sensitive instruments arising from adverse changes

in market factors such as interest rates, foreign currency exchange rates and equity price risk. Our exposure to market risk from

changes in interest rates, foreign exchange rates and equity price risk is limited. Management establishes and oversees the

implementation of policies governing our funding, investments and use of derivative financial instruments. We monitor risk

exposures on an ongoing basis. The effect of a hypothetical 10% adverse change in foreign currency rates could result in a fair

value loss of approximately $128 million on our foreign currency derivative contracts outstanding at December 31, 2015 related

to the hedging program. A 100 basis point adverse change in interest rates would not have a material impact on the Company’s

investments at December 31, 2015 and 2014. In addition, there was no material equity price risk at December 31, 2015 or 2014.

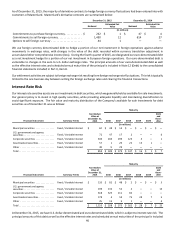

Foreign Exchange Risk

We enter into derivative contracts to manage risk associated with anticipated receipts and disbursements which are either

transacted in a non-functional currency or valued based on a currency other than our functional currency. We may also enter

into foreign currency derivative contracts to offset possible changes in value due to foreign exchange fluctuations of earnings,

assets and liabilities denominated in currencies other than the functional currency of the entity. The objective of these activities

is to reduce our exposure to transaction gains and losses resulting from fluctuations of foreign currencies against our functional

and reporting currencies, principally the U.S. dollar and euro. Foreign currency exposures are managed together through our

foreign exchange risk management activities, which are discussed further in Note 20 (Foreign Exchange Risk Management) to

the consolidated financial statements included in Part II, Item 8. The terms of the forward contracts are generally less than 18

months.