Kraft 2005 Annual Report Download - page 81

Download and view the complete annual report

Please find page 81 of the 2005 Kraft annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

MERRILL CORPORATION FLANGST// 9-MAR-06 02:25 DISK126:[06CHI5.06CHI1135]EA1135A.;8

mrll.fmt Free: 95D*/1020D Foot: 0D/ 0D VJ RSeq: 6 Clr: 0

DISK024:[PAGER.PSTYLES]UNIVERSAL.BST;51

KRAFT FOODS-FSC CERTIFIED-10K/AR Proj: P1102CHI06 Job: 06CHI1135 File: EA1135A.;8

Merrill Corporation/Chicago (312) 786-6300 Page Dim: 8.250 X 10.750Copy Dim: 38. X 54.3

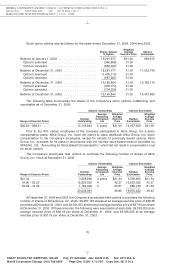

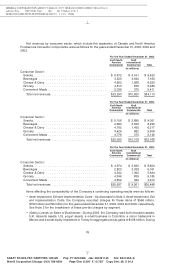

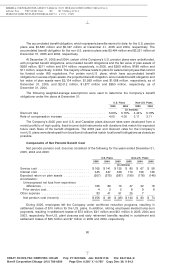

The accumulated benefit obligation, which represents benefits earned to date, for the U.S. pension

plans was $5,580 million and $5,327 million at December 31, 2005 and 2004, respectively. The

accumulated benefit obligation for the non-U.S. pension plans was $3,494 million and $3,251 million at

December 31, 2005 and 2004, respectively.

At December 31, 2005 and 2004, certain of the Company’s U.S. pension plans were underfunded,

with projected benefit obligations, accumulated benefit obligations and the fair value of plan assets of

$268 million, $211 million and $14 million, respectively, in 2005, and $260 million, $188 million and

$11 million, respectively, in 2004. The majority of these relate to plans for salaried employees that cannot

be funded under IRS regulations. For certain non-U.S. plans, which have accumulated benefit

obligations in excess of plan assets, the projected benefit obligation, accumulated benefit obligation and

fair value of plan assets were $2,134 million, $1,993 million and $1,088 million, respectively, as of

December 31, 2005, and $2,012 million, $1,877 million and $950 million, respectively, as of

December 31, 2004.

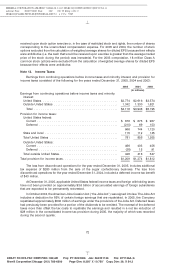

The following weighted-average assumptions were used to determine the Company’s benefit

obligations under the plans at December 31:

U.S. Plans Non-U.S. Plans

2005 2004 2005 2004

(in millions)

Discount rate .................................... 5.60% 5.75% 4.44% 5.18%

Rate of compensation increase ....................... 4.00 4.00 3.11 3.11

The Company’s 2005 year end U.S. and Canadian plans discount rates were developed from a

model portfolio of high quality, fixed-income debt instruments with durations that match the expected

future cash flows of the benefit obligations. The 2005 year end discount rates for the Company’s

non-U.S. plans were developed from local bond indices that match local benefit obligations as closely as

possible.

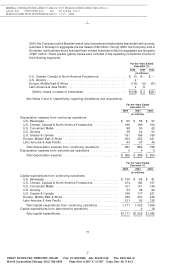

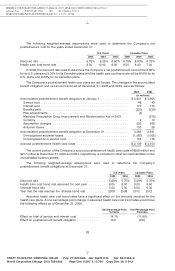

Components of Net Periodic Benefit Cost

Net periodic pension cost (income) consisted of the following for the years ended December 31,

2005, 2004 and 2003:

U.S. Plans Non-U.S. Plans

2005 2004 2003 2005 2004 2003

(in millions)

Service cost ............................ $165 $141 $135 $ 80 $ 67 $ 58

Interest cost ............................ 345 347 338 170 156 136

Expected return on plan assets .............. (507) (575) (587) (190) (178) (146)

Amortization:

Unrecognized net loss from experience

differences .......................... 166 89 15 47 32 18

Prior service cost ....................... 432898

Other expense .......................... 83 41 51 25 7

Net pension cost (income) ................ $256 $ 46 $ (46) $140 $ 93 $ 74

During 2005, employees left the Company under workforce reduction programs, resulting in

settlement losses of $10 million for the U.S. plans. In addition, retiring employees elected lump-sum

payments, resulting in settlement losses of $73 million, $41 million and $51 million in 2005, 2004 and

2003, respectively. Non-U.S. plant closures and early retirement benefits resulted in curtailment and

settlement losses of $25 million and $7 million in 2005 and 2004, respectively.

80

6 C Cs: 19871