Kraft 2005 Annual Report Download - page 49

Download and view the complete annual report

Please find page 49 of the 2005 Kraft annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

MERRILL CORPORATION MBLOUNT// 9-MAR-06 12:42 DISK126:[06CHI5.06CHI1135]DM1135A.;12

mrll.fmt Free: 52DM/0D Foot: 0D/ 0D VJ Seq: 7 Clr: 0

DISK024:[PAGER.PSTYLES]UNIVERSAL.BST;51

KRAFT FOODS-FSC CERTIFIED-10K/AR Proj: P1102CHI06 Job: 06CHI1135 File: DM1135A.;12

Merrill Corporation/Chicago (312) 786-6300 Page Dim: 8.250 X 10.750Copy Dim: 38. X 54.3

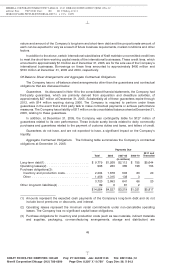

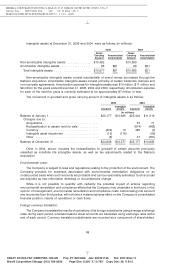

Value at Risk. The Company uses a value at risk (‘‘VAR’’) computation to estimate the potential

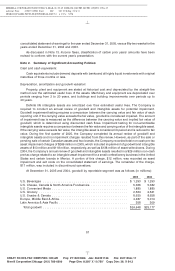

one-day loss in the fair value of its interest rate-sensitive financial instruments and to estimate the

potential one-day loss in pre-tax earnings of its foreign currency and commodity price-sensitive

derivative financial instruments. The VAR computation includes the Company’s debt; short-term

investments; foreign currency forwards, swaps and options; and commodity futures, forwards and

options. Anticipated transactions, foreign currency trade payables and receivables, and net investments

in foreign subsidiaries, which the foregoing instruments are intended to hedge, were excluded from the

computation.

The VAR estimates were made assuming normal market conditions, using a 95% confidence

interval. The Company used a ‘‘variance/co-variance’’ model to determine the observed

interrelationships between movements in interest rates and various currencies. These interrelationships

were determined by observing interest rate and forward currency rate movements over the preceding

quarter for the calculation of VAR amounts at December 31, 2005 and 2004, and over each of the four

preceding quarters for the calculation of average VAR amounts during each year. The values of foreign

currency and commodity options do not change on a one-to-one basis with the underlying currency or

commodity, and were valued accordingly in the VAR computation.

The estimated potential one-day loss in fair value of the Company’s interest rate-sensitive

instruments, primarily debt, under normal market conditions and the estimated potential one-day loss in

pre-tax earnings from foreign currency and commodity instruments under normal market conditions, as

calculated in the VAR model, were as follows (in millions):

Pre-Tax Earnings Impact Fair Value Impact

At 12/31/05 Average High Low At 12/31/05 Average High Low

Instruments sensitive to:

Interest rates .............. $29 $39 $45 $29

Foreign currency rates ....... $23 $25 $28 $23

Commodity prices .......... 7 6 12 3

Pre-Tax Earnings Impact Fair Value Impact

At 12/31/04 Average High Low At 12/31/04 Average High Low

Instruments sensitive to:

Interest rates .............. $56 $66 $74 $56

Foreign currency rates ....... $20 $16 $25 $ 4

Commodity prices .......... 4 6 8 4

This VAR computation is a risk analysis tool designed to statistically estimate the maximum

probable daily loss from adverse movements in interest rates, foreign currency rates and commodity

prices under normal market conditions. The computation does not purport to represent actual losses in

fair value or earnings to be incurred by the Company, nor does it consider the effect of favorable changes

in market rates. The Company cannot predict actual future movements in such market rates and does

not present these VAR results to be indicative of future movements in such market rates or to be

representative of any actual impact that future changes in market rates may have on its future results of

operations or financial position.

New Accounting Standards

See Note 2 to the consolidated financial statements for a discussion of new accounting standards.

Contingencies

See Note 18 to the consolidated financial statements for a discussion of contingencies.

Item 7A. Quantitative and Qualitative Disclosures about Market Risk.

See paragraphs captioned ‘‘Market Risk’’ and ‘‘Value at Risk’’ in Item 7 above.

48

6 C Cs: 62638