Kraft 2005 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2005 Kraft annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

MERRILL CORPORATION MBLOUNT// 9-MAR-06 12:42 DISK126:[06CHI5.06CHI1135]DM1135A.;12

mrll.fmt Free: 115D*/120D Foot: 0D/ 0D VJ RSeq: 3 Clr: 0

DISK024:[PAGER.PSTYLES]UNIVERSAL.BST;51

KRAFT FOODS-FSC CERTIFIED-10K/AR Proj: P1102CHI06 Job: 06CHI1135 File: DM1135A.;12

Merrill Corporation/Chicago (312) 786-6300 Page Dim: 8.250 X 10.750Copy Dim: 38. X 54.3

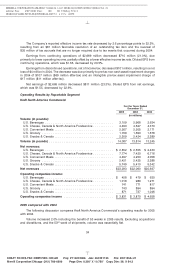

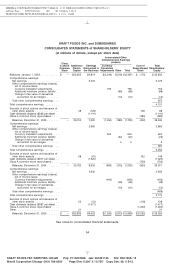

$750 million in third-party long-term debt, the net proceeds of which were used to refinance maturing

debt.

Debt and Liquidity

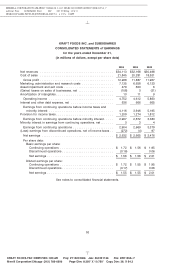

Debt. The Company’s total debt, including amounts due to Altria Group, Inc. and affiliates, was

$11.2 billion at December 31, 2005 and $12.5 billion at December 31, 2004. The Company’s

debt-to-equity ratio was 0.38 at December 31, 2005 and 0.42 at December 31, 2004. The Company’s

debt-to-capitalization ratio was 0.27 at December 31, 2005 and 0.30 at December 31, 2004.

In November 2004, the Company issued $750 million of 5-year notes bearing interest at 4.125%.

The net proceeds of the offering were used to refinance maturing debt. The Company has a Form S-3

shelf registration statement on file with the Securities and Exchange Commission (‘‘SEC’’) under which

the Company may sell debt securities and/or warrants to purchase debt securities in one or more

offerings up to a total amount of $4.0 billion. At December 31, 2005, the Company had $3.5 billion of

capacity remaining under its shelf registration.

At December 31, 2005 and 2004, the Company had short-term amounts payable to Altria

Group, Inc. and affiliates of $652 million and $227 million, respectively. The amounts payable to Altria

Group, Inc. generally include accrued dividends, taxes and service fees. Interest on intercompany

borrowings is based on the applicable London Interbank Offered Rate. The Company had no long-term

amounts payable to Altria Group, Inc. and affiliates.

Credit Ratings. Following a $10.1 billion judgment on March 21, 2003, against Altria Group, Inc.’s

domestic tobacco subsidiary, Philip Morris USA Inc., the three major credit rating agencies took a series

of ratings actions resulting in the lowering of the Company’s short-term and long-term debt ratings,

despite the fact the Company is neither a party to, nor has exposure to, this litigation. The Company’s

credit ratings by Moody’s at December 31, 2005, were ‘‘P-2’’ for short-term debt and ‘‘A3’’ for long-term

debt, with stable outlook. The Company’s credit ratings by Standard & Poor’s at December 31, 2005

were ‘‘A-2’’ for short-term debt and ‘‘BBB+’’ for long-term debt, with stable outlook. The Company’s

credit ratings by Fitch Rating Services at December 31, 2005 were ‘‘F-2’’ for short-term debt and

‘‘BBB+’’ for long-term debt, with stable outlook. As a result of the rating agencies’ actions, borrowing

costs have increased. None of the Company’s debt agreements requires accelerated repayment in the

event of a decrease in credit ratings. The credit rating downgrades by Moody’s, Standard & Poor’s and

Fitch Rating Services had no impact on any of the Company’s other existing third-party contracts.

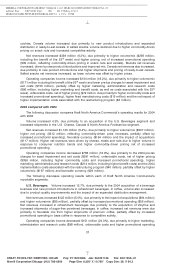

Credit Lines. The Company maintains revolving credit facilities that have historically been used to

support the issuance of commercial paper. In April 2005, the Company terminated its $2.0 billion,

multi-year revolving credit facility expiring in July 2006 and its $2.5 billion, 364-day revolving credit facility

expiring in July 2005 and replaced them with a new $4.5 billion, multi-year revolving credit facility that

expires in April 2010. At December 31, 2005, the credit line for the Company and the related activity were

as follows (in billions of dollars):

December 31, 2005

Commercial Paper

Type Credit Lines Amount Drawn Outstanding

Multi-year ................................ $4.5 $— $0.4

The Company’s revolving credit facility, which is for its sole use, requires the maintenance of a

minimum net worth of $20.0 billion. At December 31, 2005, the Company’s net worth was $29.6 billion.

The Company expects to continue to meet this covenant. The revolving credit facility does not include

any other financial tests, any credit rating triggers or any provisions that could require the posting of

collateral. The Company expects to refinance long-term and short-term debt from time to time. The

44

6 C Cs: 29224