Kraft 2005 Annual Report Download - page 25

Download and view the complete annual report

Please find page 25 of the 2005 Kraft annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

MERRILL CORPORATION ABLIJDE// 7-MAR-06 14:42 DISK126:[06CHI5.06CHI1135]DI1135A.;10

mrll.fmt Free: 190D*/240D Foot: 0D/ 0D VJ RSeq: 5 Clr: 0

DISK024:[PAGER.PSTYLES]UNIVERSAL.BST;51

KRAFT FOODS-FSC CERTIFIED-10K/AR Proj: P1102CHI06 Job: 06CHI1135 File: DI1135A.;10

Merrill Corporation/Chicago (312) 786-6300 Page Dim: 8.250 X 10.750Copy Dim: 38. X 54.3

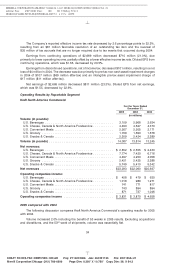

a reduction of the service cost component of net postretirement health care costs for amounts

attributable to current service, if the benefit provided is at least actuarially equivalent to Medicare Part D.

The Company adopted FSP 106-2 in the third quarter of 2004. The impact for 2005 and 2004 was a

reduction of pre-tax net postretirement health care costs and an increase in net earnings of $55 million

and $24 million, respectively. In addition, as of July 1, 2004, the Company reduced its accumulated

postretirement benefit obligation for the subsidy related to benefits attributed to past service by

$315 million and decreased its unrecognized actuarial losses by the same amount.

At December 31, 2005, for the U.S. pension and postretirement plans, the Company reduced its

discount rate assumption from 5.75% to 5.60%. The Company presently anticipates that assumption

changes, coupled with the amortization of deferred gains and losses will result in an increase in 2006

pre-tax benefit expense of approximately $80 million, or approximately $0.03 per share. The expected

increase in benefit expense is prior to the consideration of any impact of the expanded restructuring

program. While the Company does not presently anticipate a change in its 2006 assumptions, as a

sensitivity measure, a fifty-basis point decline (increase) in the Company’s discount rate would increase

(decrease) the Company’s U.S. pension and postretirement expense by approximately $72 million.

Similarly, a fifty-basis point decrease (increase) in the expected return on plan assets would increase

(decrease) the Company’s pension expense for the U.S. pension plans by approximately $31 million.

See Note 15 to the consolidated financial statements for a sensitivity discussion of the assumed health

care cost trend rates.

Revenue Recognition. As required by U.S. GAAP, the Company recognizes revenues, net of sales

incentives, and including shipping and handling charges billed to customers, upon shipment or delivery

of goods when title and risk of loss pass to customers. Shipping and handling costs are classified as part

of cost of sales. Provisions and allowances for estimated sales returns and bad debts are also recorded

in the Company’s consolidated financial statements. The amounts recorded for these provisions and

related allowances are not significant to the Company’s consolidated financial position or results of

operations.

Depreciation, Amortization and Goodwill Valuation. The Company depreciates property, plant and

equipment and amortizes definite life intangibles using the straight-line method over the estimated

useful lives of the assets.

The Company is required to conduct an annual review of goodwill and intangible assets for potential

impairment. Goodwill impairment testing requires a comparison between the carrying value and fair

value of each reporting unit. If the carrying value exceeds the fair value, goodwill is considered impaired.

The amount of impairment loss is measured as the difference between the carrying value and implied fair

value of goodwill, which is determined using discounted cash flows. Impairment testing for

non-amortizable intangible assets requires a comparison between the fair value and carrying value of

the intangible asset. If the carrying value exceeds fair value, the intangible asset is considered impaired

and is reduced to fair value. These calculations may be affected by the market conditions noted below in

the Business Environment section, as well as interest rates, general economic conditions and projected

growth rates. During the first quarter of 2005, the Company completed its annual review of goodwill and

intangible assets and no impairment charges resulted from this review. However, as part of the sale or

pending sale of certain Canadian assets and two brands, the Company recorded non-cash pre-tax asset

impairment charges of $269 million in 2005, which included impairment of goodwill and intangible

assets of $13 million and $118 million, respectively, as well as $138 million of asset write-downs. During

2004, the Company’s annual review of goodwill and intangible assets resulted in a $29 million non-cash

pre-tax charge related to an intangible asset impairment for a small confectionery business in the United

States and certain brands in Mexico. A portion of this charge, $17 million, was reclassified to earnings

from discontinued operations on the consolidated statement of earnings in the fourth quarter of 2004.

24

6 C Cs: 13586