HSBC 2013 Annual Report Download - page 76

Download and view the complete annual report

Please find page 76 of the 2013 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

|

|

HSBC BANK CANADA

74

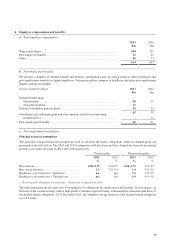

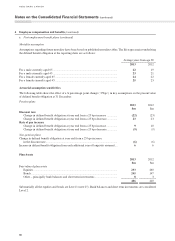

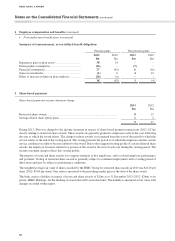

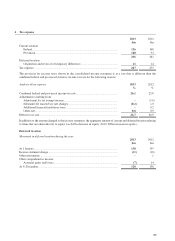

2 Summary of significant accounting policies (continued)

k Derivatives and hedge accounting (continued)

Derivatives that do not qualify for hedge accounting

All gains and losses from changes in the fair values of derivatives that do not qualify for hedge accounting are

recognized immediately in the income statement. These gains and losses are reported in ‘Net trading income’,

except where derivatives are managed in conjunction with financial instruments designated at fair value (other than

derivatives managed in conjunction with debt securities issued by the bank), in which case gains and losses are

reported in ‘Net income from financial instruments designated at fair value’. The interest on derivatives managed

in conjunction with debt securities issued by the bank which are designated at fair value is recognized in ‘Interest

expense’. All other gains and losses on these derivatives are reported in ‘Net income from financial instruments

designated at fair value’.

Derivatives that do not qualify for hedge accounting include non-qualifying hedges entered into as part of documented

interest rate management strategies for which hedge accounting was not, or could not, be applied.

The size and direction of changes in fair value of non-qualifying hedges can be volatile from year to year, but do not

alter the cash flows expected as part of the documented management strategies for both the non-qualifying hedge

instruments and the assets and liabilities to which the documented interest rate strategies relate. Non-qualifying

hedges therefore operate as economic hedges of the related assets and liabilities.

l Derecognition of financial assets and liabilities

Financial assets are derecognized when the contractual right to receive cash flows from the assets has expired; or

when the bank has transferred its contractual right to receive the cash flows of the financial assets, and either:

– substantially all the risks and rewards of ownership have been transferred; or

– the bank has neither retained nor transferred substantially all the risks and rewards, but has not retained control.

Financial liabilities are derecognized when they are extinguished, that is when the obligation is discharged, cancelled

or expires.

m Offsetting financial assets and financial liabilities

Financial assets and financial liabilities are offset and the net amount is reported in the statement of financial position

when there is a legally enforceable right to offset the recognized amounts and there is an intention to settle on a net

basis, or realize the asset and settle the liability simultaneously. New disclosures are provided in note 32.

n Subsidiaries and associates

The bank classifies investments in entities which it controls as subsidiaries.

The bank classifies investments in entities over which it has significant influence, but does not control, as associates.

Investments in associates are recognized using the equity method. Under this method, such investments are initially

stated at cost, including attributable goodwill, and are adjusted thereafter for the post-acquisition change in the

bank’s share of net assets.

Profits on transactions between the bank and its associates are eliminated to the extent of the bank’s interest in

the respective associates. Losses are also eliminated to the extent of the bank’s interest in the associates unless the

transaction provides evidence of an impairment of the asset transferred.

A structured entity is an entity that has been designed so that voting or similar rights are not the dominant factor in

deciding who controls the entity, for example when any voting rights relate to administrative tasks only, and key

activities are directed by contractual agreement. Structured entities often have restricted activities and a narrow and well

defined objective. Examples of structured entities include investment funds, securitization vehicles and asset backed

financings. The bank would be considered to sponsor another entity if it has a key role in establishing that entity or

in bringing together the relevant counterparties so that the transaction, which is the purpose of the entity, can occur.

This may include instances where the bank initially sets up an entity for a structured transaction. The bank would not

be considered a sponsor once our initial involvement in setting up the structured entity had ceased even if we were

subsequently involved with an entity to the extent of providing arm’s length services in the normal course of business.

Notes on the Consolidated Financial Statements (continued)

HSBC BANK CANADA