HSBC 2013 Annual Report Download - page 22

Download and view the complete annual report

Please find page 22 of the 2013 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

|

|

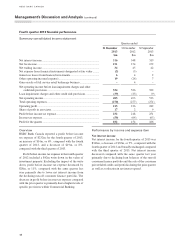

Other items of income Quarter ended

31 December

2013

$m

31 December

2012

$m

30 September

2013

$m

Net expense from financial instruments designated at fair value ........ (2) (3) –

Gains less losses from financial investments ....................................... 64 2

Other operating income/(expense) ....................................................... 19 (26) 7

Gain on the sale of the full service retail brokerage business ................ –4 –

Other items of income/(expense) ......................................................... 23 (21) 9

Net expense from financial instruments designated

at fair value for the fourth quarter of 2013 was a loss

of $2m, compared with a loss of $3m in the fourth

quarter of 2012 and nil in the third quarter of 2013. The

bank’s financial instruments designated at fair value are

fixed-rate long-term subordinated debt issued, the rate

profile of which has been changed to floating through

interest rate swaps as part of a documented interest

rate management strategy. The movement in fair value

of these long-term debt issues and the related hedges

includes the effect of our credit spread changes and any

ineffectiveness in the economic relationship between the

related swaps and own debt. As credit spreads widen

or narrow, accounting profits or losses, respectively,

are booked. We reported net expense from financial

instruments in the current quarter and the same quarter

last year primarily as a result of adverse fair value

movements driven by the tightening of credit spreads.

Gains less losses from financial investments for the

fourth quarter of 2013 were $6m, an increase of $2m

and $4m respectively, compared with the fourth quarter

of 2012 and the third quarter of 2013. Gains less losses

from financial investments increased as Balance Sheet

Management recognized higher gains on sales of available-

for-sale debt securities as a result of the continued

re-balancing of the portfolio for risk management purposes

based on the low interest rate environment.

Other operating income for the fourth quarter of

2013 was $19m, an increase of $45m compared with

the fourth quarter of 2012, and an increase of $12m

compared with the third quarter of 2013. The increase

is primarily due to a reduction in fair value of an

investment property in comparative periods.

Gain on the sale of the full service retail brokerage

business. In the fourth quarter of 2012, the bank satisfied

certain conditions relating to the sale which allowed a

further gain of $4m to be recognized. These gains were

not repeated in 2013.

Loan impairment charges and other credit risk provisions

Quarter ended

31 December

2013

$m

31 December

2012

$m

30 September

2013

$m

Individually assessed allowances/(allowance releases) ....................... 31 23 (3)

Collectively assessed allowances ........................................................... 16 6 14

Loan impairment charges ..................................................................... 47 29 11

Other credit risk provisions/(reversal of provisions) .............................. (8) 4 (2)

Loan impairment charges and other credit risk provisions .................. 39 33 9

Loan impairment charges and other credit risk

provisions for the fourth quarter of 2013 were $39m, an

increase of $6m and $30m respectively, compared with

the fourth quarter of 2012 and the third quarter of 2013.

The increase in loan impairment charges and other credit

risk provisions compared with both the same quarter

last year and the prior quarter is primarily due to higher

specific allowances for commercial customers.

HSBC BANK CANADA

Management’s Discussion and Analysis (continued)

20