HSBC 2013 Annual Report Download

Download and view the complete annual report

Please find the complete 2013 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

|

|

HSBC Bank Canada

Annual Report and Accounts 2013

Table of contents

-

Page 1

HSBC Bank Canada Annual Report and Accounts 2013 -

Page 2

-

Page 3

... 11 Movement in financial position 12 Global lines of business 18 Fourth quarter 2013 financial performance 22 Summary quarterly performance 23 Economic outlook for 2014 24 Critical accounting policies 26 Changes in accounting policy during 2013 27 Future accounting developments Off-balance sheet... -

Page 4

...and plan to give customers more reasons to bank with us in 2014. In Commercial Banking, we have refocused on those companies that we are best placed to help achieve their business goals - those with an international focus. We introduced specially trained International Relationship Managers, launched... -

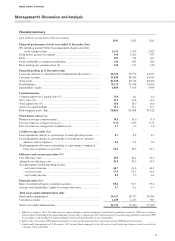

Page 5

...Financial position at 31 December ($m) Loans and advances to customers (net of impairment allowances) ...Customer accounts ...Total assets ...Total liabilities ...Shareholders' equity...Capital measures1 Common equity tier 1 capital ratio (%) ...Tier 1 ratio (%) ...Total capital ratio (%) ...Assets... -

Page 6

... loans and advances to customers by customer accounts using year-end balances. Average total shareholders' equity to average total assets is calculated by dividing average total shareholders' equity for the year (determined using month-end balances) with average total assets (determined using daily... -

Page 7

... traded in New York in the form of American Depositary Receipts. Through an international network linked by advanced technology, the HSBC Group provides a comprehensive range of financial services through four business lines: Retail Banking and Wealth Management, Commercial Banking, Global Banking... -

Page 8

... corporate governance framework is directly linked to the long-term success of the bank and the HSBC Group globally. Streamline processes and procedures This initiative is critical to the long-term sustainability of our business. Society's expectations of the financial services industry are evolving... -

Page 9

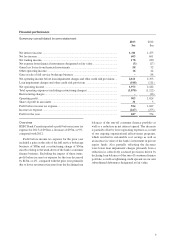

... Bank Canada reported a profit before income tax expense for 2013 of $934m, a decrease of $95m, or 9%, compared with 2012. Profit before income tax expense for the prior year included a gain on the sale of the full service brokerage business of $88m and a restructuring charge of $36m mostly relating... -

Page 10

...as a reduction in net interest spread. 2013 $m Credit facilities ...Funds under management ...Account services ...Credit cards ...Immigrant Investor Program ...Corporate finance ...Remittances ...Brokerage commissions ...Insurance ...Trade finance import/export...Trustee fees ...Other ...Fee income... -

Page 11

...the full service retail brokerage business. The sale of the full service retail brokerage business resulted in a gain of $88m, net of assets written off and directly related costs, and was reported in the results of 2012. Loan impairment charges and other credit risk provisions 2013 $m Individually... -

Page 12

... cost savings from 2011 to the end of 2013 are in excess of $130m. Right sizing operations of the bank's consumer finance business further contributed to the decrease in total operating expenses. Restructuring charges of $36m were recognized in the first quarter of 2012 primarily relating to... -

Page 13

... and advances to banks ...Loans and advances to customers ...Financial investments...Customer's liability under acceptances...Other assets ...Total assets ...LIABILITIES AND EQUITY Liabilities Deposits by banks ...Customer accounts ...Trading liabilities ...Derivatives ...Debt securities in issue... -

Page 14

...in trading liabilities is primarily as a result of increased activity in the rates business. Repurchase agreements decreased primarily as a result of reduced customer facilitating activity and balance sheet management activities. Debt securities in issue Global lines of business We manage and report... -

Page 15

... Banking franchise represents a key client base for Global Banking and Markets products and services, including foreign exchange and interest rate products, together with capital raising on debt and equity markets. Review of financial performance Strategic direction Commercial Banking aims to be... -

Page 16

... global basis. Global Banking and Markets is managed as three principal business lines: Markets, Capital Financing and Banking. This structure allows us to focus on relationships and sectors that best fit the HSBC Group's geographic reach and facilitate seamless delivery of our products and services... -

Page 17

... day-to-day finances and save for the future. We selectively offer credit facilities to assist customers in their short or longer-term borrowing requirements, and we provide financial advisory and investment services to help them to manage their financial future. We develop products designed to meet... -

Page 18

.... We focus on three strategic initiatives: - building a consistent, high standard, customer needs-driven wealth management service for retail customers drawing on our financial advisory and asset management businesses; - leveraging global expertise to improve customer service and productivity, to... -

Page 19

... fair value of own debt, income related to information technology services provided to HSBC Group companies on an arm's length basis with associated recoveries and other transactions which do not directly relate to our global lines of business. Review of financial performance 2013 $m Net interest... -

Page 20

......Net trading income...Net expense from financial instruments designated at fair value ...Gains less losses from financial investments ...Other operating income/(expense) ...Gain on sale of full service retail brokerage business...Net operating income before loan impairment charges and other credit... -

Page 21

Net fee income Quarter ended 31 December 2013 $m Credit facilities ...Funds under management ...Account services ...Credit cards ...Corporate finance ...Remittances ...Immigrant Investor Program ...Brokerage commissions ...Insurance ...Trade finance import/export...Trustee fees ...Other ...Fee ... -

Page 22

... of 2012 and nil in the third quarter of 2013. The bank's financial instruments designated at fair value are fixed-rate long-term subordinated debt issued, the rate profile of which has been changed to floating through interest rate swaps as part of a documented interest rate management strategy... -

Page 23

... effectiveness programs, which resulted in sustainable cost savings of $9m in the current quarter. Right sizing operations of the bank's consumer finance business further contributed to the decrease in total operating expenses. 146 112 9 3 270 31 December 2012 $m 152 109 8 8 277 30 September 2013... -

Page 24

... Summary consolidated income statement 2013 Quarter ended Dec 31 $m Net interest income ...Net fee income ...Net trading income...Other operating income/(expense) ...Gain on the sale of the full service retail brokerage business ...Net operating income before loan impairment charges and other credit... -

Page 25

... 2013 in line with market volatility. Operating expenses continue to decrease from the first quarter of 2012 primarily due to cost reductions relating to the wind-down of the bank's consumer finance business and as a result of continued cost reduction initiatives. Economic outlook for 2014 At best... -

Page 26

... concentrations, loan product features, economic conditions such as national and local trends in housing markets, the level of interest rates, portfolio seasoning, account management policies and practices, changes in laws and regulations, and other influences on customer payment patterns... -

Page 27

... viability of the customer's business model and the capacity to trade successfully out of financial difficulties and generate sufficient cash flow to service debt obligations. Under certain specified conditions, we provide loan forbearance to borrowers experiencing financial difficulties by agreeing... -

Page 28

... or decrease the pension expense by the difference between the current expected return on plan assets and the return calculated by applying the relevant discount rate. In addition, unvested amounts related to past service events are no longer amortized and recognized in the income statement over... -

Page 29

... hedge accounting requirements are applied prospectively and the bank is currently in the process of assessing the impact on its consolidated financial statements. Macro hedging is not included in the IFRS 9 project and will be addressed separately. In November 2013, the IASB issued amendments to... -

Page 30

...loans and advances to our customers. In accordance with accounting standards for financial instruments, we record the fair value of guarantees made on behalf of customers. For credit risk management purposes, we consider guarantees and letters of credit to be part of our customers' credit facilities... -

Page 31

... with the policies or procedures may deteriorate. Management has evaluated, under the supervision of and with the participation of the CEO and the CFO, the design and effectiveness of the internal control over financial reporting as required by the Canadian securities regulatory authorities... -

Page 32

...and strengthen the risk culture within HSBC. This training, which is updated regularly, ensures a clear and consistent message is communicated to staff. It covers technical aspects of the various risks assumed in the course of business and how these risks should be managed effectively, and serves to... -

Page 33

...remain satisfactorily capitalized after taking account of assumed management actions. Credit risk Credit risk is the risk of financial loss if a customer or counterparty fails to an obligation under contract. It arises principally from direct lending, trade finance and the leasing business, but also... -

Page 34

... also controlled globally by this unit through the imposition of country limits. A review of all credit matters undertaken by our branch and head office credit managers is completed regularly to ensure all our policies, guidelines, practices, conditions and terms are followed. We manage real estate... -

Page 35

...eligible bills...Debt securities ...Equity securities ...Customer trading assets ...Bankers acceptances ...Less: securities not exposed to credit risk...Derivatives ...Loans and advances held at amortized cost ...Loans and advances to banks ...Loans and advances to customers ...Financial investments... -

Page 36

... ...Finance and insurance ...Wholesale trade ...Services ...Transport and storage ...Business services ...Mining, logging and forestry ...Construction services ...Automotive ...Retail trade ...Hotels and accommodation ...Agriculture ...Sole proprietors ...Government services ... Total wholesale loan... -

Page 37

... mortgages ...Home equity lines of credit ...Personal unsecured revolving loan facilities...Other personal loan facilities ...Other small to medium enterprises loan facilities...Run-off consumer loan portfolio...Total retail loan portfolio ...Total loan portfolio exposure ...Large customer... -

Page 38

... CANADA Management's Discussion and Analysis (continued) - in the financial sector, charges over financial instruments such as debt and equity securities in support of trading facilities. Our credit risk management policies include appropriate guidelines on the acceptability of specific classes... -

Page 39

...; loans fully secured by cash collateral; residential mortgages in arrears more than 90 days, but where the value of collateral is sufficient to repay both the principal debt and all potential interest for at least one year; and short-term trade facilities past due more than 90 days for technical... -

Page 40

...accommodation ...Mining, logging and forestry ...Business services ...Sole proprietors ...Transportation and storage ...Services ...Finance and insurance ...Retail trade ...Total impaired wholesale portfolio ...Impaired retail portfolio Residential mortgages ...Other retail loans ...Run off consumer... -

Page 41

... allowances and provision for credit losses (Audited) 2013 Customers individually assessed $m Opening balance at the beginning of the year ...Movement Loans and advances written off net of recoveries of previously written off amounts1 ...Charge/(release) to income statement ...Reclassified as held... -

Page 42

... to support our customers' requirements and to assist us in the management of assets and liabilities, particularly relating to interest and foreign exchange rate risks as noted above. 2013 $m Interest rate contracts ...Foreign exchange contracts...Commodity contracts ...Net credit equivalent amount... -

Page 43

... to changing business models, markets and regulations. Our liquidity and funding risk management framework requires: - liquidity to be managed on a stand-alone basis with no implicit reliance on the HSBC Group or central banks; - compliance with the limit for the advances to core funding ratio; and... -

Page 44

... by placing limits to restrict the bank's ability to increase loans and advances to customers without corresponding growth in current accounts and savings accounts or long-term debt funding with a residual maturity beyond one year. This measure is referred to as the 'advances to core funding' ratio... -

Page 45

... used for the purpose of calculating one and three month stressed coverage ratio. Any unencumbered asset held as a consequence of Estimated liquidity value (Unaudited) 2013 $m Level 11...Level 22 ...17,955 3,960 21,915 118 118 110 113 137 137 120 130 2012 % 136 142 125 136 2012 % 116 122 106 114... -

Page 46

... monitored under the contingent liquidity risk structure (Unaudited) 2013 $m Commitments to conduits Total lines ...Largest individual lines ...Commitments to customers Five largest ...Largest market sector ...Sources of funding Current accounts and savings deposits, payable on demand or on short... -

Page 47

...2013 Deposits by banks ...Customer accounts ...Trading liabilities ...Financial liabilities designated at fair value ...Derivatives ...Debt securities in issue...Subordinated liabilities1 ...Other financial liabilities...Loan commitments...Financial guarantee contracts ...1 Excludes interest payable... -

Page 48

... RMC and approved by the Board as well as centrally by HSBC Group Risk Management. We set risk limits for each of our trading operations dependent upon the size, financial and capital resources of the operations, market liquidity of the instruments traded, business plan, experience and track record... -

Page 49

... all relevant stakeholders, including media, regulators, customers and employees. It is managed by every member of staff and is covered by a number of policies and guidelines. Each of the lines of business is required to have a procedure to assess and address reputational risks potentially arising... -

Page 50

... control assessments and developing and executing key control monitoring to confirm the continued operation of key controls to management. They are responsible for reporting issues identified through risk and control monitoring and testing, reviewing adequacy of action plans and progress monitoring... -

Page 51

...'s rights. Our legal function assists management in controlling legal risk. Security and fraud risk Security and fraud risk includes: Fraud Risk, Information Security Risk, and Business Continuity. The Fraud Risk function is responsible for ensuring that effective protection measures are in place... -

Page 52

... the designated businesses via a policy framework and monitoring of key indicators. The bank's principal fiduciary businesses (designated businesses) are: - HSBC Trust Company (Canada), where it is exposed to fiduciary risk via trustee's responsibilities, and - HSBC Global Asset Management (Canada... -

Page 53

... of risk management. Regulations are in place to protect our customers and the public interest. Considerable changes in laws and regulations that relate to the financial services industry have been proposed and enacted, including changes related to capital and liquidity requirements. Changes in laws... -

Page 54

... where indicated, forms an integral part of the audited consolidated financial statements) Our objective in the management of capital is to maintain appropriate levels of capital to support our business strategy and meet our regulatory requirements. Capital management The bank manages its capital in... -

Page 55

...with its capital plan. Purchase and cancelled, as well as redeemed regulatory capital instruments (Unaudited) Instrument description Preferred shares Class 2 - Series B ...Preferred shares of HSBC Mortgage Corporation (Canada)...Subordinated debentures ...Regulatory capital and risk weighted assets... -

Page 56

...Common shares ($m) ...Preferred shares ($ per share) Class 1, Series C ...Class 1, Series D ...Class 1, Series E ...Class 2, Series B1 ...HSBC HaTSâ„¢ - Series 2015 ($ per unit) ...1 Preferred shares - Class 2, Series B were redeemed on 27 December 2013. 2012 330 1.275 1.250 1.650 0.310 51.50 2011... -

Page 57

..., the bank's Chief Auditor and OSFI have full and free access to the Board of Directors and its committees to discuss audit, financial reporting and related matters. Paulo Maia President and Chief Executive Officer Jacques Fleurant Chief Financial Officer Vancouver, Canada 21 February 2014 55 -

Page 58

... audited the accompanying consolidated financial statements of HSBC Bank Canada, which comprise the consolidated statements of financial position as at 31 December 2013 and 31 December 2012, the consolidated income statement and statements of comprehensive income, changes in equity and cash flows... -

Page 59

...Consolidated statement of cash flows ...Consolidated statement of changes in equity ...Notes on the Consolidated Financial Statements 1 Basis of preparation ...2 Summary of significant accounting policies 3 Net operating income ...4 Employee compensation and benefits...5 Share-based payments...6 Tax... -

Page 60

... ...Net trading income...Net income/(expense) from financial instruments designated at fair value .. Gains less losses from financial investments ...Other operating income...Gain on sale of full service brokerage business ...Net operating income before loan impairment charges and other credit risk... -

Page 61

HSBC BANK CANADA Consolidated statement of comprehensive income For the year ended 31 December (in millions of dollars) 2013 $m 687 2012 $m 754 Note Profit for the year ...Other comprehensive income Available-for-sale investments1 ...- fair value gains/(loss) ...- fair value gains transferred to ... -

Page 62

... sections of 'Risk Management' and 'Capital' within Management's Discussion and Analysis form an integral part of these consolidated financial statements. Approved on behalf of the Board of Directors: Samuel Minzberg Chairman, HSBC Bank Canada Paulo Maia President and Chief Executive Officer 60 -

Page 63

HSBC BANK CANADA Consolidated statement of cash flows For the year ended 31 December (in millions of dollars) 2013 $m 934 28 28 28 265 (584) 1,847 (215) 2,247 2012 $m 1,029 203 (3,311) 1,150 (350) (1,279) Note Cash flows from operating activities Profit before tax...Adjustments for: - non-cash ... -

Page 64

... 2012 ... 1 Share capital is comprised of common shares $1,225m and preference shares $600m (2012: $946m). The accompanying notes and the audited sections of 'Risk Management' and 'Capital' within Management's Discussion and Analysis form an integral part of these consolidated financial statements... -

Page 65

... consolidated financial statements, HSBC Group means the Parent and its subsidiary companies. From 1 January 2011, the bank has prepared its consolidated financial statements in accordance with International Financial Reporting Standards ('IFRS') and accounting guidelines as issued by the Office... -

Page 66

... bank's critical accounting policies where judgement is necessarily applied are those which relate to impairment of loans and advances and the valuation of financial instruments as described within the Management's Discussion and Analysis. d Consolidation The consolidated financial statements of the... -

Page 67

... or decrease the pension expense by the difference between the current expected return on plan assets and the return calculated by applying the relevant discount rate. In addition, unvested amounts related to past service events are no longer amortized and recognized in the income statement over... -

Page 68

... hedge accounting requirements are applied prospectively and the bank is currently in the process of assessing the impact on its consolidated financial statements. Macro hedging is not included in the IFRS 9 project and will be addressed separately. In November 2013, the IASB issued amendments to... -

Page 69

...following global lines of business: Commercial Banking, Global Banking and Markets, as well as Retail Banking and Wealth Management. Measurement of segmental assets, liabilities, income and expenses is in accordance with the bank's accounting policies. Segmental income and expenses include transfers... -

Page 70

HSBC BANK CANADA Notes on the Consolidated Financial Statements (continued) 2 Summary of significant accounting policies (continued) d Valuation of financial instruments All financial instruments are recognized initially at fair value. In the normal course of business, the fair value of a ... -

Page 71

... following factors: - the bank's aggregate exposure to the customer; - the viability of the customer's business model and their capacity to trade successfully out of financial difficulties and generate sufficient cash flow to service debt obligations; - the amount and timing of expected receipts and... -

Page 72

... decrease can be related objectively to an event occurring after the impairment was recognized, the excess is written back by reducing the loan impairment allowance account accordingly. The write-back is recognized in the income statement. Assets acquired in exchange for loans Non-financial assets... -

Page 73

... rate risk management strategy. An accounting mismatch would arise if the debt securities issued were accounted for at amortized cost, because the related derivatives are measured at fair value with changes in the fair value recognized in the income statement. By designating the long-term debt... -

Page 74

HSBC BANK CANADA Notes on the Consolidated Financial Statements (continued) 2 Summary of significant accounting policies (continued) i Financial investments (continued) Interest income is recognized on available-for-sale debt securities using the effective interest rate, calculated over the asset... -

Page 75

... value. Fair values of exchange traded derivatives are obtained from quoted market prices. Fair values of over-the-counter derivatives are obtained using valuation techniques, including discounted cash flow models and option pricing models. Derivatives are classified as assets when their fair value... -

Page 76

... immediately in the income statement. These gains and losses are reported in 'Net trading income', except where derivatives are managed in conjunction with financial instruments designated at fair value (other than derivatives managed in conjunction with debt securities issued by the bank), in... -

Page 77

... and depreciation calculated to write off the assets over their estimated useful lives as follows: - land is not depreciated; - buildings are depreciated over their estimated useful lives (between 20 and 40 years); and - leasehold improvements are depreciated over the shorter of their lease term or... -

Page 78

HSBC BANK CANADA Notes on the Consolidated Financial Statements (continued) 2 Summary of significant accounting policies (continued) r Income tax Income tax comprises current tax and deferred tax. Income tax is recognized in the income statement except to the extent that it relates to items ... -

Page 79

...that settlement will require the outflow of economic benefits, or because the amount of the obligations cannot be reliably measured. Contingent liabilities are not recognized in the financial statements but are disclosed unless the probability of settlement is remote. w Financial guarantee contracts... -

Page 80

HSBC BANK CANADA Notes on the Consolidated Financial Statements (continued) 2 Summary of significant accounting policies (continued) x Debt securities in issue and deposits by customers and banks Financial liabilities are recognized when the bank enters into the contractual provisions of the ... -

Page 81

... and settlement gains and other amounts related to restructuring included above ...Post-employment benefits ...c Post-employment benefit plans 2013 $m 20 12 30 62 - 62 2012 $m 19 - 31 50 11 61 Principal actuarial assumptions The principal actuarial financial assumptions used to calculate the... -

Page 82

...from a 25 bps decrease...Non-pension plans Change in defined benefit obligation at year end from a 25 bps increase in the discount rate ...Increase in defined benefit obligation from each additional year of longevity assumed ...Plan Assets 2013 $m Fair value of plan assets Equities ...Bonds ...Other... -

Page 83

... costs and a higher defined benefit liability. The bank takes steps to manage these risks through an asset liability management program, which includes reducing interest rate and market risk over time by increasing its asset allocation to bonds that more closely match the plan's obligations. 81 -

Page 84

HSBC BANK CANADA Notes on the Consolidated Financial Statements (continued) 4 Employee compensation and benefits (continued) c Post-employment benefit plans (continued) Summary of remeasurement, net on defined benefit obligations Pension plans 2013 2012 $m $m 38 14 (26) - 27 (61) (1) 6 (20) (1) ... -

Page 85

... enacted tax rate changes ...Additional financial institution taxes ...Other, net ...Effective tax rate ...2013 % 26.1 - (0.2) - 0.8 26.7 2012 % 25.8 (1.0) 1.0 0.2 0.9 26.9 In addition to the amount charged to the income statement, the aggregate amount of current and deferred taxation relating to... -

Page 86

...of deferred taxation accounted for in the statement of financial position comprised the following deferred tax assets and liabilities: 2013 2012 $m $m Deferred tax assets Retirement benefits ...72 86 Loan impairment allowances ...33 54 Unused tax credits ...- 7 Assets leased to customers ...(71) (66... -

Page 87

... financial needs, and Business Banking, to serve small and medium-sized enterprises ('SME's), enabling differentiated coverage of our target customers. Client offering includes Credit and Lending; International trade and receivables finance; Payments and Cash Management; and Global Banking... -

Page 88

HSBC BANK CANADA Notes on the Consolidated Financial Statements (continued) 8 Segment analysis (continued) 2013 $m Commercial Banking Net interest income ...Net fee income ...Net trading income...Other operating loss ...Net operating income before loan impairment charges and other credit risk ... -

Page 89

... - 2,182 2,182 - Commercial Banking $m At 31 December 2013 Loans and advances to customers (net) ...Customers' liability under acceptances...Total assets ...Customer accounts Acceptances ...Total liabilities...At 31 December 2012 Loans and advances to customers (net) ...Customers' liability under... -

Page 90

... and by statement of financial position heading: Financial liabilities Deposits by banks ...Customer accounts ...Items in the course of transmission to other banks .. Trading liabilities ...Financial liabilities designated at fair value...Derivatives ...Debt securities in issue...Other liabilities... -

Page 91

... 650 151 4,737 80,229 Financial liabilities Deposits by banks ...Customer accounts ...Items in the course of transmission to other banks .. Trading liabilities ...Financial liabilities designated at fair value...Derivatives ...Debt securities in issue...Other liabilities...Acceptances ...Accruals... -

Page 92

...Equity securities ... 1 Including government guaranteed bonds Term to maturity of debt securities Less than 1 year ...1-5 years ...5-10 years ...Over 10 years ... 216 1,422 651 239 2,528 301 1,255 291 245 2,092 11 Derivatives Fair values of derivatives by product contract type held 2013 Trading... -

Page 93

...rate contracts Futures...Swaps ...Caps...Other interest rate contracts ...- 20,864 303 - 21,167 - 2,904 7,386 10,290 130 31,587 2012 Trading 1 to 5 years $m More than 5 years $m Total trading...124 64,257 Foreign exchange contracts Spot contracts ...Forward contracts...Currency swaps and options ... ... -

Page 94

... are reported in 'Net income from financial instruments designated at fair value', together with the gains and losses on the hedged items. Where the derivatives are managed with debt securities in issue, the contractual interest is shown in 'interest expense' together with the interest payable on... -

Page 95

... portfolio and related credit exposure 2013 Credit equivalent amount 2 $m - 1,070 6 - 1,076 2012 Credit equivalent amount 2 $m - 1,094 7 - 1,101 Notional amount 1 $m Interest rate contracts Future ...Swaps ...Caps...Other interest rate contracts ...Foreign exchange contracts Spot contracts... -

Page 96

HSBC BANK CANADA Notes on the Consolidated Financial Statements (continued) 11 Derivatives (continued) Fair value of derivatives designated as fair value hedges 2013 Assets Liabilities $m $m Interest rate...60 69 2012 Assets Liabilities $m $m 8 94 Gains or losses arising from the change in fair ... -

Page 97

...462 3 months or less $m Assets ...Liabilities ...Net cash inflow/(outflow) exposure...17,239 (7,622) 9,617 5 years or more $m 119 (387) (268) The gains and losses on ineffective portions of such derivatives are recognized immediately in 'Net trading income'. During 2013, a gain of $5m (2012: gain... -

Page 98

... bonds1...Other debt securities issued by banks and other financial institutions ...Other debt securities ... 16,534 799 3,248 1,224 9 21,814 13,429 2,308 2,999 1,666 9 20,411 1 Includes government guaranteed bonds. The term to maturity of financial investments are as follows: 2013 $m Term to... -

Page 99

.... Deposits by banks ...Customer accounts ...Items in the course of transmission to other banks ...Trading liabilities ...Financial liabilities designated at fair value ...Derivatives ...Debt securities in issue...Acceptances ...Subordinated liabilities ...Other liabilities...Shareholders' equity... -

Page 100

... 1.6 Deposits by banks ...Customer accounts ...Items in the course of transmission to other banks ...Trading liabilities ...Financial liabilities designated at fair value ...Derivatives ...Debt securities in issue...Acceptances ...Subordinated liabilities ...Other liabilities...Shareholders' equity... -

Page 101

... cash flows from the financial assets, or retains the right but assumes an obligation to pass on the cash flows from the asset, and transfers substantially all the risks and rewards of ownership. The risks typically include credit, interest rate, prepayment and other price risks. The following table... -

Page 102

HSBC BANK CANADA Notes on the Consolidated Financial Statements (continued) 15 Property, plant and equipment (continued) Freehold land and Leasehold buildings improvements $m $m Cost At 1 January 2012 ...Additions at cost ...Disposals and write-offs...At 31 December 2012 ...Accumulated ... -

Page 103

... 2012. 19 Trading liabilities 2013 $m Other liabilities - net short positions ...Customer trading liabilities ...Trading liabilities due to other banks ...Other debt securities in issue ...3,617 442 300 37 4,396 2012 $m 1,644 916 55 57 2,672 20 Debt securities in issue 2013 $m Bonds and medium term... -

Page 104

...which are unsecured and subordinated in right of payment to the claims of depositors and certain other creditors, comprise: Foreign Carrying amount Currency 2013 2012 Year of Amount Interest rate (%) $m $m maturity $m Issued to HSBC Group Companies 4.8221...Issued to third parties 4.942...4.803...30... -

Page 105

...between financial instruments; - the degree of consistency between different sources; - the process followed by the pricing provider to derive the data; - the elapsed time between the date to which the market data relates and the reporting date; and - the manner in which the data was sourced. Models... -

Page 106

...For all issued debt securities, discounted cash flow modelling is used to separate the change in fair value that may be attributed to the bank's credit spread movements from movements in other market factors such as benchmark interest rates or foreign exchange rates. Specifically, the change in fair... -

Page 107

... as foreign exchange rates, interest rates and equity prices. As a result of changing market practices in response to regulatory and accounting changes, as well as general market developments, the bank revised its methodology for estimating the credit valuation adjustment ('CVA') and debit valuation... -

Page 108

... ...Issues ...Settlements ...Transfer out ...At 31 December 2013 ...Total gains or losses recognized in profit or loss relating to those assets and liabilities held at the end of the reporting period ...9 1 - (10) - - 5 34 - - (5) 34 Held for trading $m 49 1 15 (1) (55) 9 Liabilities Designated at... -

Page 109

...'. Fair value changes on long-term debt designated at fair value and related derivatives are presented in the income statement under 'Changes in fair value of long-term debt issued and related derivatives'. The income statement line item 'Net income from financial instruments designated at fair... -

Page 110

...: 2013 Level 3 Level 1 Level 2 with Quoted using significant market observable unobservprice inputs able inputs $m $m $m 2012 Carrying amount $m Assets Loans and advances to banks ...Loans and advances to customers ...Liabilities Deposits by banks ...Customer accounts .. Debt securities in issue... -

Page 111

... the ordinary course of business, we pledge assets recorded on our consolidated statement of financial position in relation to securitization activity, mortgages sold with recourse, securities lending and securities sold under repurchase agreements. These transactions are conducted under terms that... -

Page 112

HSBC BANK CANADA Notes on the Consolidated Financial Statements (continued) 26 Share Capital Authorized: Preferred - Unlimited number of Class 1 preferred shares in one or more series and unlimited number of Class 2 preferred shares in one or more series. We may, from time to time, divide any ... -

Page 113

... of securities issued by the Trust ('HSBC HaTSâ„¢'). The Trust assets are primarily undivided co-ownership interests in pools of Canada Mortgage and Housing Corporation and Genworth Financial Mortgage Insurance Company Canada insured first mortgages originated by the bank, and Trust deposits with... -

Page 114

... credit risk provisions ...Charge for defined benefit pension plans ...Gain on sale of full service retail brokerage business... Change in operating assets Change in prepayment and accrued income ...Change in net trading securities and net derivatives ...Change in loans and advances to customers... -

Page 115

... Agreement with the New York County District Attorney ('DANY'), and HSBC Holdings consented to a cease and desist order with the Federal Reserve Board ('FRB'). HSBC Holdings also entered into an Undertaking with the UK Financial Services Authority (now a Financial Conduct Authority ('FCA') Direction... -

Page 116

... US DPA, FCA direction, and other settlement agreements. The settlement with U.S. and U.K. authorities does not preclude private litigation relating to, among other things, the HSBC Group's compliance with applicable AML/BSA and sanctions laws or other regulatory or law enforcement actions for AML... -

Page 117

... be varied to reflect changes in, for example, tax or interest rates. Rentals are calculated to recover the cost of assets less their residual value, and earn finance income. 2013 Unearned finance income $m 2012 Unearned finance income $m Total future minimum payment $m Lease receivables: No later... -

Page 118

HSBC BANK CANADA Notes on the Consolidated Financial Statements (continued) 31 Related party transactions The ultimate parent company of the bank is HSBC Holdings, which is incorporated in England. The bank's related parties include the parent, fellow subsidiaries, and Key Management Personnel. a ... -

Page 119

... the ordinary course of business and on substantially the same terms, including interest rates and security, as for comparable transactions with third party counterparties. 2013 Highest balance during Balance at the year 31 December $m $m Assets Trading assets ...Derivatives ...Loans and advances to... -

Page 120

... statement of financial position Gross amounts of recognized financial assets $m At 31 December 2013 Derivatives2 (note 11) ...Reverse repurchase, securities borrowing and similar agreements: - Loan and advances to banks at amortized cost...- Loan and advances to customers at amortized cost...Loans... -

Page 121

... statement of financial position Gross amounts of recognized financial assets $m At 31 December 2012 Derivatives2 (note 11) ...Reverse repurchase, securities borrowing and similar agreement classified as: - Loan and advances to banks at amortized cost...- Loan and advances to customers at amortized... -

Page 122

...Except as noted above, there have been no other material events after the reporting period which would require disclosure or adjustment to the 31 December 2013 consolidated financial statements. These accounts were approved by the Board of Directors on 21 February 2014 and authorized for issue. 120 -

Page 123

...HSBC Group International Network* Services are provided by over 6,300 offices in 75 countries and territories: Europe Offices Asia-Pacific Offices Americas Offices Middle East and Africa Offices Armenia Austria Belgium Channel Islands Czech Republic France Germany Greece Ireland Isle of Man Italy... -

Page 124

... Management Vancouver Linda Seymour Executive Vice President and Head of Commercial Banking Toronto Sandra Stuart Chief Operating Officer Vancouver Board of Directors* Samuel Minzberg Chairman, HSBC Bank Canada and Senior Partner, Davies Ward Phillips & Vineberg LLP John Flint Group Managing... -

Page 125

... to contact their brokers. For general information please write to the bank's transfer agent, Computershare Investor Services Inc., at their mailing address or by e-mail to [email protected]. Other shareholder inquiries may be directed to Shareholder Relations by writing to: HSBC Bank Canada... -

Page 126

... Copyright HSBC Bank Canada 2014 All rights reserved No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of HSBC Bank Canada. Form... -

Page 127

HSBC Bank Canada 885 West Georgia Street Vancouver, British Columbia Canada V6C 3E8 Telephone: 1 604 685 1000 www.hsbc.ca