Google 2007 Annual Report Download - page 91

Download and view the complete annual report

Please find page 91 of the 2007 Google annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

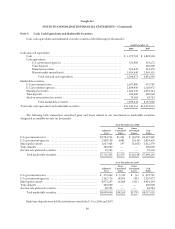

Google Inc.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

new fair value measurements, but provides guidance on how to measure fair value by providing a fair value hierarchy used

to classify the source of the information. SFAS 157 is effective for fiscal years beginning after November 15, 2007.

However, on December 14, 2007, the FASB issued proposed FSP FAS 157-b which would delay the effective date of

SFAS 157 for all nonfinancial assets and nonfinancial liabilities, except those that are recognized or disclosed at fair value

in the financial statements on a recurring basis (at least annually). This proposed FSP partially defers the effective date of

Statement 157 to fiscal years beginning after November 15, 2008, and interim periods within those fiscal years for items

within the scope of this FSP. Effective for 2008, we will adopt SFAS 157 except as it applies to those nonfinancial assets

and nonfinancial liabilities as noted in proposed FSP FAS 157-b. The partial adoption of SFAS 157 will not have a material

impact on our consolidated financial position, results of operations or cash flows.

In February 2007, the FASB issued SFAS No. 159, The Fair Value Option for Financial Assets and Financial Liabilities-

including an Amendment of FASB Statement No. 115 (“SFAS 159”), which allows an entity to choose to measure certain

financial instruments and liabilities at fair value. Subsequent measurements for the financial instruments and liabilities an

entity elects to fair value will be recognized in earnings. SFAS 159 also establishes additional disclosure requirements.

SFAS 159 is effective for us beginning January 1, 2008. We are currently evaluating the potential impact of the adoption of

SFAS 159 on our consolidated financial position, results of operations or cash flows.

In December 2007, the FASB issued SFAS No. 141 (revised 2007), Business Combinations (“SFAS 141R”).

SFAS 141R establishes principles and requirements for how an acquirer recognizes and measures in its financial

statements the identifiable assets acquired, the liabilities assumed, any noncontrolling interest in the acquiree and the

goodwill acquired. SFAS 141R also establishes disclosure requirements to enable the evaluation of the nature and financial

effects of the business combination. This statement is effective for us beginning January 1, 2009. We are currently

evaluating the potential impact of the adoption of SFAS 141R on our consolidated financial position, results of operations

or cash flows.

In December 2007, the FASB issued SFAS No. 160, Noncontrolling Interests in Consolidated Financial Statements—an

amendment of Accounting Research Bulletin No. 51 (“SFAS 160”). SFAS 160 establishes accounting and reporting standards

for ownership interests in subsidiaries held by parties other than the parent, the amount of consolidated net income

attributable to the parent and to the noncontrolling interest, changes in a parent’s ownership interest, and the valuation of

retained noncontrolling equity investments when a subsidiary is deconsolidated. SFAS 160 also establishes disclosure

requirements that clearly identify and distinguish between the interests of the parent and the interests of the

noncontrolling owners. This statement is effective for us beginning January 1, 2009. We are currently evaluating the

potential impact of the adoption of SFAS 160 on our consolidated financial position, results of operations or cash flows.

77