Google 2007 Annual Report Download - page 75

Download and view the complete annual report

Please find page 75 of the 2007 Google annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

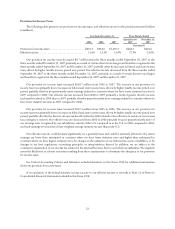

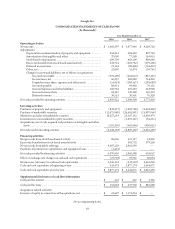

Interest Rate Risk

We invest in a variety of securities, consisting primarily of investments in interest-bearing demand deposit accounts

with financial institutions, tax-exempt money market funds and highly liquid debt securities of corporations and

municipalities. By policy, we limit the amount of credit exposure to any one issuer.

Investments in both fixed rate and floating rate interest earning products carry a degree of interest rate risk. Fixed

rate securities may have their fair market value adversely impacted due to a rise in interest rates, while floating rate

securities may produce less income than predicted if interest rates fall. Due in part to these factors, our income from

investments may decrease in the future.

We considered the historical volatility of short term interest rates and determined that it was reasonably possible that

an adverse change of 100 basis points could be experienced in the near term. A hypothetical 1.00% (100 basis-point)

increase in interest rates would have resulted in a decrease in the fair values of our marketable securities of approximately

$98.8 million and $86.7 million at December 31, 2006 and December 31, 2007.

61