Frontier Communications 2005 Annual Report Download - page 84

Download and view the complete annual report

Please find page 84 of the 2005 Frontier Communications annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

-

96

|

|

F-35

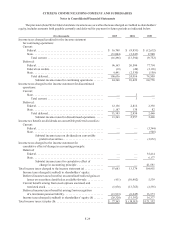

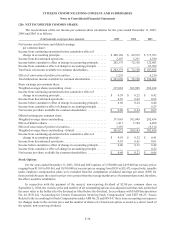

CITIZENS COMMUNICATIONS COMPANY AND SUBSIDIARIES

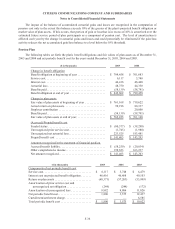

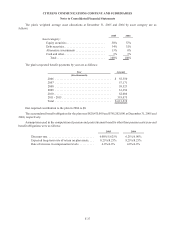

Notes to Consolidated Financial Statements

(24) RETIREMENT PLANS:

We sponsor a noncontributory defined benefit pension plan covering a significant number of our employees

and other postretirement benefit plans that provide medical, dental, life insurance benefits and other benefits for

covered retired employees and their beneficiaries and covered dependents. The benefits are based on years of service

and final average pay or career average pay. Contributions are made in amounts sufficient to meet ERISA funding

requirements while considering tax deductibility. Plan assets are invested in a diversified portfolio of equity and

fixed-income securities and alternative investments.

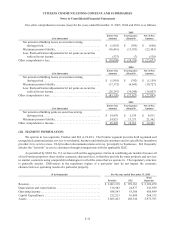

The accounting results for pension and postretirement benefit costs and obligations are dependent upon various

actuarial assumptions applied in the determination of such amounts. These actuarial assumptions include the

following: discount rates, expected long-term rate of return on plan assets, future compensation increases, employee

turnover, healthcare cost trend rates, expected retirement age, optional form of benefit and mortality. We review

these assumptions for changes annually with its outside actuaries. We consider our discount rate and expected long-

term rate of return on plan assets to be our most critical assumptions.

The discount rate is used to value, on a present value basis, our pension and postretirement benefit obligation

as of the balance sheet date. The same rate is also used in the interest cost component of the pension and postretirement

benefit cost determination for the following year. The measurement date used in the selection of our discount rate is

the balance sheet date. Our discount rate assumption is determined annually with assistance from our actuaries

based on the duration of our pension and postretirement benefit liabilities, the pattern of expected future benefit

payments and the prevailing rates available on long-term, high quality corporate bonds that approximate the benefit

obligation. In making this determination we consider, among other things, the yields on the Citigroup Pension

Discount Curve and Bloomberg Finance. This rate can change from year-to-year based on market conditions that

impact corporate bond yields.

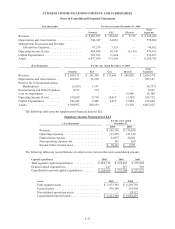

The expected long-term rate of return on plan assets is applied in the determination of periodic pension and

postretirement benefit cost as a reduction in the computation of the expense. In developing the expected long-term

rate of return assumption, we considered published surveys of expected market returns, 10 and 20 year actual returns

of various major indices, and our own historical 5-year and 10-year investment returns.

The expected long-term rate of return on plan assets is based on an asset allocation assumption of 30% to 45%

in fixed income securities, 45% to 55% in equity securities and 5% to 15% in alternative investments. We review our

asset allocation at least annually and make changes when considered appropriate. In 2005, we did not change our

expected long-term rate of return from the 8.25% used in 2004. Our pension plan assets are valued at actual market

value as of the measurement date. The measurement date used to determine pension and other postretirement benefit

measures for the pension plan and the postretirement benefit plan is December 31.

Accounting standards require that we record an additional minimum pension liability when the plan’s

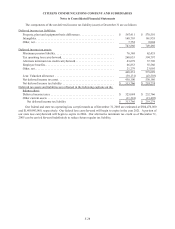

“accumulated benefit obligation” exceeds the fair market value of plan assets at the pension plan measurement

(balance sheet) date. In the fourth quarter of 2005, mainly due to a decrease in the year-end discount rate, we

recorded an additional minimum pension liability in the amount of $36,416,000 with a corresponding charge to

shareholders’ equity of $22,483,000, net of taxes of $13,933,000. In the fourth quarter of 2004, mainly due to a

decrease in the year-end discount rate, we recorded an additional minimum pension liability in the amount of

$17,372,000 with a corresponding charge to shareholders’ equity of $10,727,000, net of taxes of $6,645,000. These

adjustments did not impact our net income or cash flows for either year. If discount rates and the equity markets

performance decline, we would be required to increase our minimum pension liabilities and record additional charges

to shareholder’s equity in the future.

Actual results that differ from our assumptions are added or subtracted to our balance of unrecognized actuarial

gains and losses. For example, if the year-end discount rate used to value the plan’s projected benefit obligation

decreases from the prior year-end, then the plan’s actuarial loss will increase. If the discount rate increases from the

prior year-end then the plan’s actuarial loss will decrease. Similarly, the difference generated from the plan’s actual

asset performance as compared to expected performance would be included in the balance of unrecognized gains and

losses.