Frontier Communications 2005 Annual Report Download - page 11

Download and view the complete annual report

Please find page 11 of the 2005 Frontier Communications annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

9

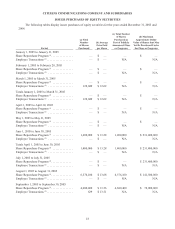

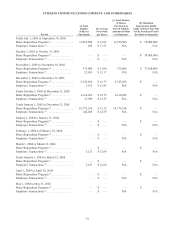

CITIZENS COMMUNICATIONS COMPANY AND SUBSIDIARIES

The telecommunications industry is undergoing significant changes. The market is extremely competitive,

resulting in lower prices, and consumers are changing behavior, such as using wireless in place of wireline services and

using e-mail instead of making calls. These trends are likely to continue and result in a challenging revenue

environment. These factors could also result in more bankruptcies in the sector and therefore affect our ability to

collect money owed to us by bankrupt carriers.

ELI Competition

ELI faces significant competition from incumbents in each of its markets. Principal incumbent competitors include

Qwest, at&t and Verizon. ELI also competes with all of the major IXCs, internet access providers and other CLECs.

CLEC service providers have generally encountered intense competitive pressures, the result of which is the failure of

a number of CLECs and substantial financial pressures on others.

Competitors in ELI’s markets include, in addition to the incumbent providers: at&t, Sprint, Time Warner Telecom,

Verizon, Integra Telecom and XO Communications. In each of the markets in which ELI operates, at least one other

CLEC, and in some cases several other CLECs, offer many of the same services that ELI provides, generally at similar

prices.

Competition is based on price, quality, network reliability, customer service, service features and responsiveness

to the customer’s needs. Many of our competitors have greater market presence and greater financial, technical,

marketing and human resources, more extensive infrastructure and stronger customer and strategic relationships

than are available to us. Competition in the CLEC industry is intense and pricing continues to decline. ELI’s

revenues have declined since 2000, however 2005 revenues were higher than 2004.

DIVESTITURE OF PUBLIC UTILITIES SERVICES

In the past we provided public utilities services including natural gas transmission and distribution, electric

transmission and distribution, water distribution and wastewater treatment services to primarily rural and suburban

customers throughout the United States. In 1999, we announced a plan of divestiture for our public utilities services

properties. Since then, we have divested all of our public utility operations for an aggregate of $1.9 billion.

We have retained a potential payment obligation associated with our previous electric utility activities in the

state of Vermont. The Vermont Joint Owners (VJO), a consortium of 14 Vermont utilities, including us, entered into

a purchase power agreement with Hydro-Quebec in 1987. The agreement contains “step-up” provisions which state

that if any VJO member defaults on its purchase obligation under the contract to purchase power from Hydro-

Quebec, then the other VJO participants will assume responsibility for the defaulting party’s share on a pro-rata

basis. Our pro-rata share of the purchase power obligation is 10%. If any member of the VJO defaults on its

obligations under the Hydro-Quebec agreement, the remaining members of the VJO, including us, may be required

to pay for a substantially larger share of the VJO’s total power purchase obligation for the remainder of the agreement

(which runs through 2015). Paragraph 13 of FIN 45 requires that we disclose “the maximum potential amount of

future payments (undiscounted) the guarantor could be required to make under the guarantee.” Paragraph 13 also

states that we must make such disclosure “… even if the likelihood of the guarantor’s having to make any payments

under the guarantee is remote…” As noted above, our obligation only arises as a result of default by another VJO

member, such as upon bankruptcy. Therefore, to satisfy the “maximum potential amount” disclosure requirement

we must assume that all members of the VJO simultaneously default, a highly unlikely scenario given that the two

members of the VJO that have the largest potential payment obligations are publicly traded with credit ratings that

are equal to or superior to ours, and that all VJO members are regulated utility providers with regulated cost recovery.

Regardless, despite the remote chance that such an event could occur, or that the State of Vermont could or would

allow such an event, assuming that all the members of the VJO defaulted on January 1, 2007 and remained in default

for the duration of the contract (another 9 years), we estimate that our undiscounted purchase obligation for 2007

through 2015 would be approximately $1.26 billion. In such a scenario we would then own the power and could seek

to recover our costs. We would do this by seeking to recover our costs from the defaulting members and/or reselling

the power to other utility providers or the northeast power grid. There is an active market for the sale of power. We

could potentially lose money if we were unable to sell the power at cost. We caution that we cannot predict with any

degree of certainty any potential outcome.