Cisco 2007 Annual Report Download - page 49

Download and view the complete annual report

Please find page 49 of the 2007 Cisco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

|

|

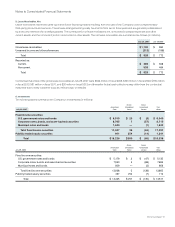

52 Cisco Systems, Inc.

Notes to Consolidated Financial Statements

Use of Estimates The preparation of financial statements and related disclosures in conformity with accounting principles generally

accepted in the United States requires management to make estimates and judgments that affect the amounts reported in the

Consolidated Financial Statements and accompanying notes. Estimates are used for revenue recognition, allowance for doubtful accounts

and sales returns, inventory valuation and liability for purchase commitments with contract manufacturers and suppliers, warranty costs,

share-based compensation expense, investment impairments, goodwill impairments, income taxes, and loss contingencies, among others.

The actual results experienced by the Company may differ materially from management’s estimates.

Share-Based Compensation Expense On July 31, 2005, the Company adopted SFAS 123(R) which requires the measurement and

recognition of compensation expense for all share-based payment awards made to employees and directors including employee

stock options and employee stock purchases related to the Employee Stock Purchase Plan (“employee stock purchase rights”) based

on estimated fair values. SFAS 123(R) supersedes the Company’s previous accounting under Accounting Principles Board Opinion

No. 25, “Accounting for Stock Issued to Employees” (“APB 25”) beginning in fiscal 2006. In March 2005, the U.S. Securities and Exchange

Commission (SEC) issued Staff Accounting Bulletin No. 107 (“SAB 107”) relating to SFAS 123(R). The Company has applied the provisions

of SAB 107 in its adoption of SFAS 123(R).

The Company adopted SFAS 123(R) using the modified prospective transition method, which required the application of the

accounting standard as of July 31, 2005, the first day of the Company’s fiscal 2006. The Company’s Consolidated Financial Statements for

fiscal 2007 and 2006 reflect the impact of SFAS 123(R). In accordance with the modified prospective transition method, the Company’s

Consolidated Financial Statements for fiscal years prior to fiscal 2006 have not been restated to reflect, and do not include, the impact

of SFAS 123(R). For additional information, see Note 10 to the Consolidated Financial Statements.

SFAS 123(R) requires companies to estimate the fair value of share-based payment awards on the date of grant using an option-pricing

model. The value of awards that are ultimately expected to vest is recognized as expense over the requisite service periods in the Company’s

Consolidated Statements of Operations. Prior to the adoption of SFAS 123(R), the Company accounted for share-based awards to

employees and directors using the intrinsic value method in accordance with APB 25 as allowed under Statement of Financial Accounting

Standards No. 123, “Accounting for Stock-Based Compensation” (“SFAS 123”). Under the intrinsic value method, no share-based

compensation expense had been recognized in the Company’s Consolidated Statements of Operations, other than as related to

acquisitions and investments, because the exercise price of the Company’s stock options granted to employees and directors equaled

the fair market value of the underlying stock at the date of grant.

Share-based compensation expense recognized in the Company’s Consolidated Statements of Operations for fiscal 2007 and 2006

included compensation expense for share-based payment awards granted prior to, but not yet vested as of July 30, 2005 based on the

grant date fair value estimated in accordance with the pro forma provisions of SFAS 123 and compensation expense for the share-based

payment awards granted subsequent to July 30, 2005 based on the grant date fair value estimated in accordance with the provisions of

SFAS 123(R). In conjunction with the adoption of SFAS 123(R), the Company changed its method of attributing the value of share-based

compensation to expense from the accelerated multiple-option approach to the straight-line single-option method. Compensation

expense for all share-based payment awards granted on or prior to July 30, 2005 will continue to be recognized using the accelerated

multiple-option approach while compensation expense for all share-based payment awards granted subsequent to July 30, 2005 is

recognized using the straight-line single-option method. Because share-based compensation expense recognized in the Consolidated

Statements of Operations for fiscal 2007 and 2006 is based on awards ultimately expected to vest, it has been reduced for forfeitures.

Upon adoption of SFAS 123(R), the Company also changed its method of valuation for share-based awards granted beginning in fiscal

2006 to a lattice-binomial option-pricing model (“lattice-binomial model”) from the Black-Scholes option-pricing model (“Black-Scholes

model”) which was previously used for the Company’s pro forma information required under SFAS 123. For additional information, see

Note 10 to the Consolidated Financial Statements. The Company’s determination of fair value of share-based payment awards on the date

of grant using an option-pricing model is affected by the Company’s stock price as well as assumptions regarding a number of highly

complex and subjective variables. These variables include, but are not limited to, the Company’s expected stock price volatility over the

term of the awards, and actual and projected employee stock option exercise behaviors. Option-pricing models were developed for use

in estimating the value of traded options that have no vesting or hedging restrictions and are fully transferable. Because the Company’s

employee stock options have certain characteristics that are significantly different from traded options, and because changes in the

subjective assumptions can materially affect the estimated value, in management’s opinion, the existing valuation models may not provide

an accurate measure of the fair value of the Company’s employee stock options. Although the fair value of employee stock options is

determined in accordance with SFAS 123(R) and SAB 107 using an option-pricing model, that value may not be indicative of the fair value

observed in a willing buyer/willing seller market transaction.