Capital One 1996 Annual Report Download - page 50

Download and view the complete annual report

Please find page 50 of the 1996 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59

|

|

On November 17, 1995, the Company entered into a

three-year, $1,715,000 unsecured revolving credit arrange-

ment (the “1995 Credit Facility”), which was replaced in

1996 by the Credit Facility discussed above. The 1995

Credit Facility, which replaced the 1994 syndicated bank

facility, consisted of three tranches. Tranches A and B, for

$1,300,000 and $200,000, respectively, were available to

the Bank. In addition, Tranche B allowed the Bank to

borrow in major foreign currencies. Tranche C was for

$215,000 and was available to the Corporation and the Bank.

The Company entered into swaps to effectively convert

certain of the interest rates on bank notes from fixed to

variable. The swaps, which had a notional amount totaling

$974,000 as of December 31, 1996, will mature in 1997

through 2000 to coincide with maturities of fixed bank

notes. These swaps paid three-month London Interbank

Offered Rate (“LIBOR”) at a weighted average contractual

rate of 5.59% as of December 31, 1996 and received a

weighted average fixed rate of 7.71%.

As of December 31, 1995, swaps with a notional amount

totaling $1,014,000, with maturity dates from 1996

through 2000, paid three-month LIBOR at a weighted

average contractual rate of 5.69% and received a weighted

average fixed rate of 7.68%. In 1995, the Company entered

into basis swaps (notional amounts totaling $260,000) to

effectively convert bank notes, with a variable rate based

on six-month LIBOR to a variable rate based on three-

month LIBOR. These swaps and bank notes matured

in 1996.

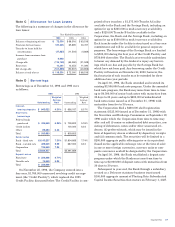

Senior and deposit notes as of December 31, 1996,

mature as follows (all other borrowings mature in 1997):

Senior Notes Deposit Notes Total

1997 $ 891,436 $ 891,436

1998 800,166 $299,996 $1,100,162

1999 625,000 625,000

2000 599,614 599,614

2001 438,115 438,115

Thereafter 339,906 339,906

Total $3,694,237 $299,996 $3,994,233

Note E Associate Benefit Plans

The Company sponsors a contributory Associate Savings

Plan in which substantially all full-time and certain part-

time associates are eligible to participate. The Company

matches a portion of associate contributions and makes

discretionary contributions based upon the Company’s

earnings per common share. Effective January 1, 1996, the

Company is required to make additional contributions for

pay-based credits for eligible associates which were previ-

ously provided under the Cash Balance Pension Plan. The

Company’s contributions to this plan were $9,048, $2,701

and $3,890 for the years ended December 31, 1996, 1995

and 1994, respectively.

Through December 31, 1995, the Company provided its

associate pension benefits through the Cash Balance

Pension Plan and postretirement medical coverage and life

insurance benefits through the Associate Welfare Benefits

Plan. Effective December 31, 1995, the Company amended

the Cash Balance Pension Plan so that no future pay-based

credits will accrue. Future pay-based credits will accrue to

the Associate Savings Plan discussed above. Neither the

remaining obligations under the Cash Balance Pension

Plan nor the obligations under the unfunded Associate

Welfare Benefits Plan were material to the Company’s

financial statements.

Note F Stock Plans

The Company has three stock-based compensation plans

which are described below. The Company applies

Accounting Principles Board Opinion No. 25, “Accounting

for Stock Issued to Employees” (“APB 25”) and related

Interpretations in accounting for its stock-based compensa-

tion plans. In accordance with APB 25, no compensation

cost has been recognized for the Company’s fixed stock

options, since the exercise price equals the market price of

the underlying stock on the date of grant, nor for the stock

purchase plan, which is considered to be noncompensatory.

For the performance-based option plan discussed below,

compensation cost for these options is measured as the

difference between the exercise price and the market price

required for vesting and is recognized over the estimated

vesting period.

During 1995, the FASB issued SFAS No. 123,

“Accounting for Stock-Based Compensation” (“SFAS 123”)

which requires, for companies electing to continue to follow

the recognition provisions of APB 25, pro forma informa-

tion regarding net income and earnings per share, as if the

recognition provisions of SFAS 123 were adopted for stock

options granted subsequent to December 31, 1994. For

purposes of pro forma disclosure, the estimated fair value

of the options is amortized to expense over the options’

vesting period. For the year ended December 31, 1996 and

1995, the Company’s pro forma net income and earnings

per share information would have been $151,853, or $2.25

per share, and $125,296, or $1.88 per share, respectively.

48 Capital One

Notes to Consolidated Financial Statements (continued)

(dollars in thousands, except per share data)