Capital One 1996 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 1996 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

|

|

Capital One

Management’s Discussion and Analysis of

Financial Condition and Results of Operations (continued)

36

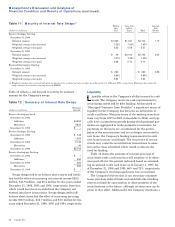

The Company expects to increase its solicitation (mar-

keting) expenses in 1997, as compared to 1996, and to

invest in existing and new first and second generation

products as marketing opportunities develop. These oppor-

tunities are subject to a variety of external and internal

factors that may affect the actual amount of solicitation

expense, such as competition in the credit card industry,

general economic conditions affecting consumer credit per-

formance and the asset quality of the Company’s portfolio.

Moreover, the first generation and second generation prod-

ucts have different account growth, loan growth and asset

quality characteristics. As a result, although the Company

expects that its growth in consumer accounts and managed

consumer loan growth will continue in 1997, actual growth

may vary significantly depending on the actual mix of prod-

ucts that the Company may offer in 1997.

The Company currently expects continued increases in

the delinquency and net charge-off rates of its portfolio.

Actual amount of increases will be affected by continued

seasoning of the portfolio, general economic trends in

consumer credit and the product mix. To the extent the

Company markets first generation products and experi-

ences greater consumer loan growth, the increases in delin-

quency and net charge-off rates will be less, as delinquencies

and net charge-off characteristics of new portfolios generally

are lower than more seasoned portfolios. However, because

second generation products generally have higher delin-

quencies and net charge-offs than first generation products,

to the extent the Company increases the proportion of

second generation products in its portfolio, the increases in

delinquency and net charge-off rates will be greater. These

factors notwithstanding, the Company believes that the

credit quality of its portfolio is enhanced as a result of the

application of IBS.

The Company also has been applying, and expects to

continue applying, its IBS to other financial products and

non-financial products (“third generation products”). The

Company has established the Savings Bank and several

non-bank operating subsidiaries to identify and explore

new product opportunities. The Company is in various

stages of developing and test marketing a number of new

products or services including, but not limited to, selected

non-card consumer lending products and the reselling of

telecommunication services. During 1996, the Company

allocated an increased percentage of its marketing expens-

es to non-card products or services. To date, only a relative-

ly small dollar percentage of assets and a relatively small

percentage of accounts have been generated as a result of

such expenditures. As the Company continues to apply its

IBS to non-card opportunities and builds the infrastructure

necessary to support new businesses, the Company expects

that it may increase the percentage of its 1997 marketing

and operating expenses attributable to such businesses.

The Company expects to maintain a flexible approach to

its marketing investment. The Company intends to continue

applying its IBS to all products, even established products

and businesses, and the results of ongoing testing will

influence the amount and allocation of future marketing

investment. Management believes that, through the contin-

ued application of IBS, the Company can develop product

and service offerings to sustain growth and that it has the

personnel, financial resources and business strategy neces-

sary for continued success. However, as the Company

attempts to apply IBS to diversify and expand its product

offerings beyond credit cards, there can be no assurance

that the historical financial information of the Company

will necessarily reflect the results of operations and finan-

cial condition of the Company in the future. The Company’s

actual results will be influenced by, among other things,

the factors discussed in this section.

The Company’s strategies and objectives outlined above

and the other forward looking statements contained in this

section involve a number of risks and uncertainties. The

Company cautions readers that any forward looking infor-

mation is not a guarantee of future performance and that

actual results could differ materially. In addition to the fac-

tors discussed above, among the other factors that could

cause actual results to differ materially are the following:

continued intense competition from numerous providers of

products and services which compete with the Company’s

businesses; with respect to financial products, changes in

the Company’s aggregate accounts or consumer loan bal-

ances and the growth rate thereof, including changes

resulting from factors such as shifting product mix, amount

of actual marketing expenses made by the Company and

attrition of accounts and loan balances; an increase in cred-

it losses (including increases due to a worsening of general

economic conditions); difficulties or delays in the develop-

ment, production, testing and marketing of new products

or services; losses associated with new products or services;

financial, legal, regulatory or other difficulties that may

affect investment in, or the overall performance of a prod-

uct or business; the amount of, and rate of growth in, the

Company’s expenses (including associate and marketing

expenses) as the Company’s business develops or changes

or as it expands into new market areas; the availability of

capital necessary to fund the Company’s new businesses;

the ability of the Company to build the operational and

organizational infrastructure necessary to engage in new

businesses; the ability of the Company to recruit experi-

enced personnel to assist in the management and opera-

tions of new products and services; and other factors listed

from time to time in the Company’s SEC reports, including

but not limited to the Annual Report on Form 10-K for the

year ended December 31, 1996 (Part I, Item 1, Cautionary

Statements).