Capital One 1996 Annual Report Download - page 31

Download and view the complete annual report

Please find page 31 of the 1996 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

|

|

Capital One 29

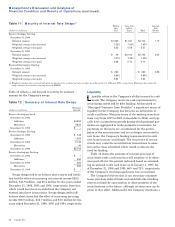

Table 7 Summary of Allow ance for Loan Losses

Year Ended December 31

(dollars in thousands) 1996 1995 1994 1993 1992

Balance at beginning of year $ 72,000 $ 68,516 $ 63,516 $ 55,993 $ 31,541

Provision for loan losses 167,246 65,895 30,727 34,030 55,012

Transfer to loans held for securitization (27,887) (11,504) (4,869) (2,902)

Increase from consumer loan purchase 9,000

Charge-offs (115,159) (64,260) (31,948) (39,625) (44,666)

Recoveries 13,300 13,353 11,090 16,020 14,106

Net charge-offs(1) (101,859) (50,907) (20,858) (23,605) (30,560)

Balance at end of year $ 118,500 $ 72,000 $ 68,516 $ 63,516 $ 55,993

Allowance for loan losses to loans

at year-end(1) 2.73% 2.85% 3.07% 3.41% 4.29%

(1) Excludes consumer loans held for securitization.

For the year ended December 31, 1996, the provision for

loan losses increased to $167.2 million, or 154%, from the

1995 provision for loan losses of $65.9 million. The increase

in the provision for loan losses resulted from increases in

average reported consumer loans of 24%, continued loan

seasoning, a shift in the composition of reported consumer

loans and general economic trends in consumer credit per-

formance. Net charge-offs as a percentage of average

reported consumer loans increased to 3.63% for the year

ended December 31, 1996 from 2.03% in the prior year.

Additionally, growth in second generation products which

have modestly higher charge-off rates than first generation

products, increased the amount of provision necessary to

absorb credit losses. In consideration of these factors, the

Company increased the allowance for loan losses by $46.5

million during 1996.

For the year ended December 31, 1995, the increase in

the provision for loan losses resulted from increases in

average reported consumer loans of 37%, continued loan

seasoning, a shift in the composition of reported consumer

loans and a softening in U.S. consumer credit quality. Net

charge-offs as a percentage of average reported consumer

loans increased to 2.03% for the year ended December 31,

1995 from 1.13% in the prior year. The increase in the pro-

vision and charge-off rate reflects an 87% increase in the

seller’s interest in securitization trusts to $1.4 billion, or

48%, of the reported average balance for 1995 from

$700 million, or 33%, of the reported average balance for

1994. This seller’s interest represents an undivided inter-

est in the trust receivables in excess of investor certificates

outstanding in the trust. These receivables are generally

more seasoned than the other newer on-balance sheet

loans. In consideration of growth in second generation

products, the Company increased the allowance for loan

losses by $3.5 million during 1995.

Provision and Allow ance for Loan Losses

The provision for loan losses is the periodic expense of

maintaining an adequate allowance at the amount

estimated to be sufficient to absorb possible future losses,

net of recoveries (including recovery of collateral), inherent

in the existing on-balance sheet loan portfolio. In evaluat-

ing the adequacy of the allowance for loan losses, the

Company takes into consideration several factors including

economic trends and conditions, overall asset quality, loan

seasoning and trends in delinquencies and expected charge-

offs. The Company’s primary guideline is a calculation

which uses current delinquency levels and other measures

of asset quality to estimate net charge-offs. Once a loan is

charged off, it is the Company’s policy to continue to pursue

the recovery of principal and interest.

Management believes that the allowance for loan losses

is adequate to cover anticipated losses in the on-balance

sheet consumer loan portfolio under current conditions.

There can be no assurance as to future credit losses that

may be incurred in connection with the Company’s con-

sumer loan portfolio, nor can there be any assurance that

the loan loss allowance that has been established by the

Company will be sufficient to absorb such future credit

losses. The allowance is a general allowance applicable to

the on-balance sheet consumer loan portfolio. Table 7 sets

forth the activity in the allowance for loan losses for the

periods indicated. See “Asset Quality,” “Delinquencies” and

“Net Charge-Offs” for a more complete analysis of asset

quality.