Capital One 1996 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 1996 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

-

59

|

|

Capital One 45

Solicitation: The Company expenses the costs related to

the solicitation of new accounts as incurred.

Credit Card Fraud Losses: The Company experiences fraud

losses from the unauthorized use of credit cards.

Transactions suspected of being fraudulent are charged to

non-interest expense after a 60-day investigation period.

Income Taxes: Deferred tax assets and liabilities are deter-

mined based on differences between the financial reporting

and tax bases of assets and liabilities and are measured

using the enacted tax rates and laws that will be in effect

when the differences are expected to reverse.

Earnings Per Share: Earnings per share are based on the

weighted average number of common and common equiva-

lent shares, including dilutive stock options and restricted

stock outstanding during the year, after giving retroactive

effect to the initial capitalization of the Company as if the

issuance of all shares had occurred on January 1, 1994.

Income that would have been generated from the proceeds

of the Company’s common stock on November 22, 1994 was

not considered in the calculation of earnings per share.

Interest Rate Sw ap Agreements: The Company enters into

interest rate swap agreements (“swaps”) for purposes of

managing its interest rate sensitivity. The Company desig-

nates swaps to on-balance sheet instruments to alter the

interest rate characteristics of such instruments and to

modify interest rate sensitivity. The Company also desig-

nates swaps to off-balance sheet items to reduce the inter-

est rate sensitivity associated with off-balance sheet cash

flows (i.e., securitizations).

Swaps involve the periodic exchange of payments over

the life of the agreements. Amounts received or paid on

swaps that are used to manage interest rate sensitivity and

alter the interest rate characteristics of on-balance sheet

instruments or reduce interest rate sensitivity associated

with off-balance sheet items are recorded on an accrual

basis as an adjustment to the related income or expense of

the item to which the agreements are designated. The

related amount receivable from counterparties of $41,548

and $26,652 as of December 31, 1996 and 1995, respectively,

was included in other assets. Changes in the fair value of

swaps are not reflected in the accompanying financial

statements.

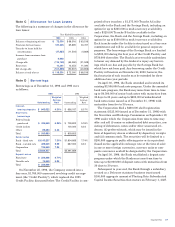

Securitizations: The Company securitizes credit card loans

and records such securitizations as sales in accordance

with Statement of Financial Accounting Standards (“SFAS”)

No. 77, “Reporting by Transferors for Transfers of

Receivables with Recourse.” Due to the relatively short

average life of credit card loans securitized (approximately

8 to 12 months), no gains are recorded at the time of sale.

Rather, excess servicing fees related to the securitizations

are recorded over the life of each sale transaction. The

excess servicing fee is based upon the difference between

finance charges received from the cardholders less the yield

paid to investors, credit losses and a normal servicing fee,

which is also retained by the Company. In accordance with

the sale agreements, a fixed amount of excess servicing fees

is set aside to absorb potential credit losses. Accounts

receivable from securitization principally represents excess

servicing fees earned and due to the Company. Transaction

expenses are deferred and amortized over the reinvestment

period of the transaction as a reduction of loan servicing

fees. The monthly pattern of recording loan servicing fees is

similar to the revenue recognition that the Company would

have experienced if the loans had not been securitized.

In June 1996, the Financial Accounting Standards

Board (“FASB”) issued SFAS No. 125 (“SFAS 125”),

“Accounting for Transfers and Servicing of Financial Assets

and Extinguishments of Liabilities,” which establishes the

accounting for certain financial asset transfers including

securitization transactions. SFAS 125 requires an entity,

after a transfer of financial assets that meets the criteria

for sale accounting, to recognize the financial and servicing

assets it controls and the liabilities it has incurred and to

derecognize financial assets for which control has been

surrendered. The provisions of SFAS 125 are effective

January 1, 1997. Based on the anticipated performance of

securitization transactions the Company has undertaken,

the Company does not believe the adoption of the new

standard will have a material impact on the Company’s

financial statements.

Premises and Equipment: Premises and equipment are

stated at cost less accumulated depreciation and amortiza-

tion ($99,104 and $61,452 as of December 31, 1996 and

1995, respectively). Depreciation and amortization expense

are computed generally by the straight-line method over

the estimated useful lives of the assets.