Berkshire Hathaway 2002 Annual Report Download - page 56

Download and view the complete annual report

Please find page 56 of the 2002 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

|

|

55

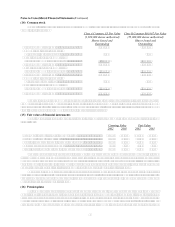

Insurance — Underwriting (Continued)

General Re (Continued)

workers’ compensation, medical malpractice, auto liability and professional liability coverages. The 2002 prior year

loss reserve adjustment was net of a $115 million reduction in reserves established in connection with the

September 11th terrorist attack. The reduction in reserves related to the September 11th terrorist attack was due

primarily to decreased loss estimates for certain claims. As of December 31, 2002, approximately $241 million of

claims arising as a result of the September 11th terrorist attack have been paid.

About $386 million of the reserve increases for prior years’ claims resulted from actual reported claims

exceeding expectations. This under-estimation of expected claims indicated that the level of premium rate erosion

that occurred in recent years was greater than had been previously contemplated in General Re's earlier loss reserve

estimates. As a result of the higher than anticipated reported losses, General Re increased reserves for incurred but

not reported (“IBNR”) claims by an additional $604 million.

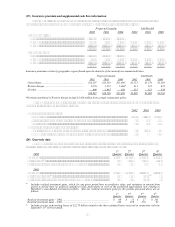

The process of establishing reserves by General Re, like most other reinsurers, requires numerous estimates

and judgments by management. Loss reserve estimates are based primarily on claims reported by ceding companies

(such amounts generally exclude IBNR claims), analysis of historical claim reporting patterns of ceding companies,

and estimates of expected overall loss amounts for all accident periods. Expected overall losses are partly based

upon assumptions with respect to both General Re’ s and ceding companies’ premium rate adequacy. Premium rate

adequacy assumptions are an indicator of the profitability of the subject business reinsured and are important in

establishing reserves for claims that will be reported and settled over long periods into the future. Claim frequency

or count analyses are generally not practicable because such data is either not provided by ceding companies or

otherwise not timely or reliable. Loss reserves, which are established based on estimates by line of business and

type of coverage, are regularly re-evaluated and appropriate adjustments are made to bring reserves in line with the

revised estimates.

IBNR reserves are largely comprised of liability and workers’ compensation exposures because these

claims tend to be reported by and settled with ceding companies over long time periods. Therefore, such claims are

subject to a higher degree of estimation error as a result of changes in the legal environment, jury awards, medical

cost trends and general cost inflation. Based upon statistical analysis of past reporting trends, General Re estimates

how much IBNR is required to cover claims that will be reported by ceding companies in future years.

Subsequently, as claims are reported, amounts are measured against previous expectations, with variances (positive

or negative) recognized in earnings as a component of losses and loss adjustment expenses. Significant variances

are analyzed and revised judgments are made with respect to remaining IBNR reserve levels, and are also

recognized in earnings.

There is considerable judgment employed in developing the estimates because of inherent delays in claim

emergence and reporting by ceding companies, particularly with respect to liability claims. Normally only about

15% of ultimate excess casualty reinsurance claims are reported in the year of loss occurrence. General Re has not

quantified a range of possible reserve estimates.

Among other factors, management believes the revised estimates in 2002 for prior years were due to: (a) an

increase in claim severity, which has a leveraged effect on excess of loss coverages provided by General Re by

producing a disproportionate increase in claims exceeding General Re’ s attachment point; (b) escalating medical

inflation and utilization that adversely affect workers’ compensation and other casualty lines; (c) an increased

frequency in corporate bankruptcies, scandals and accounting restatements which increased losses under directors

and officers coverages; (d) broadened coverage terms under General Re’ s reinsurance contracts during 1997

through 2000; (e) increased ceding companies’ reserve inadequacies, likely arising from broadened terms and

conditions, as well as previously unrecognized premium inadequacies; and (f) increased primary company

insolvencies, which changed historical claim reporting patterns.

General Re continuously estimates its liabilities and related reinsurance recoverables for environmental and

asbestos claims and claim expenses. Most liabilities for such claims arise from exposures in North America.

Environmental and asbestos exposures do not lend themselves to traditional methods of loss development

determination and therefore reserves related to these exposures may be considered less reliable than reserves for

standard lines of business (e.g., automobile). The estimate for environmental and asbestos losses is composed of

four parts: known claims, development on known claims, IBNR and direct excess coverage litigation expenses. At

December 31, 2002, environmental and asbestos loss reserves for North America were $1,161 million ($1,008