Berkshire Hathaway 2002 Annual Report Download - page 55

Download and view the complete annual report

Please find page 55 of the 2002 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

|

|

54

Management's Discussion (Continued)

Insurance — Underwriting (Continued)

General Re (Continued)

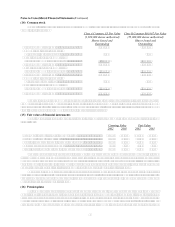

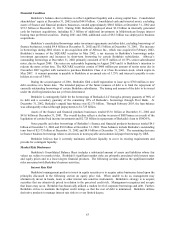

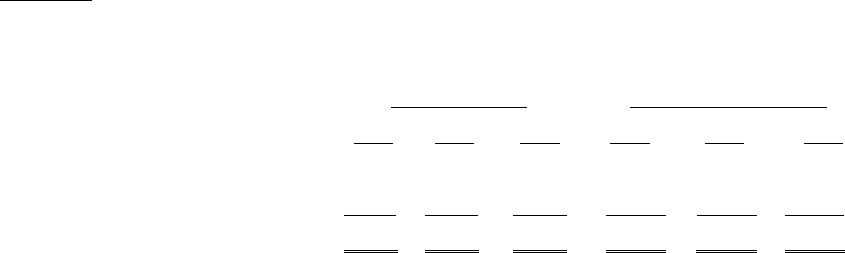

General Re’ s pre-tax underwriting results for the past three years are summarized below.

— (dollars in millions) —

Premiums earned Pre-tax underwriting loss

2002 2001 2000 2002 2001 2000

North American property/casualty....................... $3,967 $3,968 $3,389 $(1,019) $(2,843) $ (656)

International property/casualty ............................ 2,647 2,397 3,046 (319) (746) (518)

Global life/health................................................... 1,886 1,988 2,261 (55) (82) (80)

$8,500 $8,353 $8,696 $(1,393) $(3,671) $(1,254)

General Re’ s underwriting results were negatively impacted in both 2002 and 2001 by increases in loss

reserve estimates established for claims occurring in prior years with respect to the North American

property/casualty business. Additionally, underwriting results for 2001 were severely impacted by losses from the

September 11th terrorist attack.

General Re took significant underwriting actions to better align premium rates with coverage terms during

the past two years. Improved current accident year results for 2002 in the North American, London market and

global life/health operations, in part, reflect these efforts. However, management continues to believe that

additional premium rate increases and more favorable coverage terms are needed in certain lines and territories to

achieve targeted long-term underwriting profitability. Information with respect to each of General Re’ s

underwriting units is presented below.

North American property/casualty

General Re’ s North American property/casualty operations underwrite predominantly excess reinsurance

across multiple lines of business. Excess reinsurance provides indemnification of losses above a stated retention on

either an individual claim basis or in the aggregate across all claims in a portfolio. Reinsurance contracts are written

on both a treaty (group of risks) and facultative (individual risk) basis.

Premiums earned in 2002 were unchanged from premiums earned in 2001. Premiums earned in 2001

increased over 2000 levels by $579 million (17.1%). Premiums earned in 2002 were primarily impacted by rate

increases (estimated at approximately $800 million) across most lines of business, partially offset by reductions

from cancellations in excess of new business written. Premiums earned in 2001 included $400 million from one

retroactive reinsurance contract and a large quota share agreement. An aggregate excess reinsurance contract

produced earned premiums of $404 million in 2000. There were no such contracts written in 2002.

The North American property/casualty business had underwriting losses of $1,019 million in 2002, $2,843

million in 2001, and $656 million in 2000. The underwriting loss in 2002 included charges of $990 million (24.9%

of premiums earned in 2002) from increases to prior years’ loss reserves. Underwriting losses for 2001 and 2000

included charges of $800 million and $92 million respectively for prior years’ loss reserve increases. Underwriting

results in 2002 also included a net gain of $66 million with respect to the 2002 accident year. The favorable effects

of re-pricing efforts and improved contract terms and conditions implemented over the past two years contributed to

the net gain. In addition, underwriting results for 2002 were favorably impacted by the absence of major

catastrophes and other large individual property losses ($20 million or greater), a condition that is unusual and

should not be expected to occur regularly in the future. As a result, 2002 accident year results for property lines

were better than normally expected. Underwriting results for 2001 included approximately $1.54 billion of net

losses from the September 11th terrorist attack, as well as $87 million of losses from other catastrophes (principally

Tropical Storm Allison) and other large individual property losses. Results for 2000 included $53 million of

catastrophe and other large property losses and a loss of $239 million from a large excess reinsurance contract.

The adjustment of $990 million to prior year loss estimates in 2002 was from casualty lines of business and

related principally to the 1997 through 2000 accident years. Increases in prior years’ general liability claims totaled

about $400 million. The remainder of the increase in prior years’ reserves in 2002 was split fairly evenly among