BP 2009 Annual Report Download - page 122

Download and view the complete annual report

Please find page 122 of the 2009 BP annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

|

|

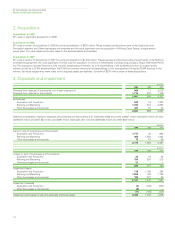

1. Significant accounting policies continued

Financial liabilities

Financial liabilities are classified as financial liabilities at fair value

through profit or loss; derivatives designated as hedging instruments

in an effective hedge; or as financial liabilities measured at amortized

cost, as appropriate. Financial liabilities include trade and other payables,

accruals, finance debt and derivative financial instruments. The group

determines the classification of its financial liabilities at initial recognition.

The measurement of financial liabilities depends on their classification,

as follows:

Financial liabilities at fair value through profit or loss

Derivatives, other than those designated as effective hedging

instruments, are classified as held for trading and are included in this

category. These liabilities are carried on the balance sheet at fair value

with gains or losses recognized in the income statement.

Derivatives designated as hedging instruments in an effective hedge

Such derivatives are carried on the balance sheet at fair value, the

treatment of gains and losses arising from revaluation are described

below in the accounting policy for derivative financial instruments and

hedging activities.

Financial liabilities measured at amortized cost

All other financial liabilities are initially recognized at fair value. For

interest-bearing loans and borrowings this is the fair value of the

proceeds received net of issue costs associated with the borrowing.

After initial recognition, other financial liabilities are subsequently

measured at amortized cost using the effective interest method.

Amortized cost is calculated by taking into account any issue costs, and

any discount or premium on settlement. Gains and losses arising on the

repurchase, settlement or cancellation of liabilities are recognized

respectively in interest and other revenues and finance costs.

This category of financial liabilities includes trade and other

payables and finance debt.

Leases

Finance leases, which transfer to the group substantially all the risks and

benefits incidental to ownership of the leased item, are capitalized at the

commencement of the lease term at the fair value of the leased property

or, if lower, at the present value of the minimum lease payments. Financ

charges are allocated to each period so as to achieve a constant rate of

interest on the remaining balance of the liability and are charged directly

against income.

Capitalized leased assets are depreciated over the shorter of the

estimated useful life of the asset or the lease term.

Operating lease payments are recognized as an expense in the

income statement on a straight-line basis over the lease term.

For both finance and operating leases, contingent rents are

recognized in the income statement in the period in which they

are incurred.

Derivative financial instruments and hedging activities

The group uses derivative financial instruments to manage certain

exposures to fluctuations in foreign currency exchange rates, interest

rates and commodity prices as well as for trading purposes. Such

derivative financial instruments are initially recognized at fair value on the

date on which a derivative contract is entered into and are subsequently

remeasured at fair value. Derivatives are carried as assets when the fair

value is positive and as liabilities when the fair value is negative.

Contracts to buy or sell a non-financial item that can be settled net in

cash or another financial instrument, or by exchanging financial

instruments as if the contracts were financial instruments, with the

exception of contracts that were entered into and continue to be held

for the purpose of the receipt or delivery of a non-financial item in

accordance with the group’s expected purchase, sale or usage

requirements, are accounted for as financial instruments.

Gains or losses arising from changes in the fair value of

derivatives that are not designated as effective hedging instruments are

recognized in the income statement.

For the purpose of hedge accounting, hedges are classified as:

• Fair value hedges when hedging exposure to changes in the fair value

of a recognized asset or liability.

• Cash flow hedges when hedging exposure to variability in cash flows

that is either attributable to a particular risk associated with a

recognized asset or liability or a highly probable forecast transaction.

• Hedges of a net investment in a foreign operation.

At the inception of a hedge relationship the group formally designates

and documents the hedge relationship for which the group wishes to

claim hedge accounting, together with the risk management objective

and strategy for undertaking the hedge. The documentation includes

identification of the hedging instrument, the hedged item or transaction,

the nature of the risk being hedged, and how the entity will assess the

hedging instrument effectiveness in offsetting the exposure to changes

in the hedged item’s fair value or cash flows attributable to the hedged

item. Such hedges are expected at inception to be highly effective in

achieving offsetting changes in fair value or cash flows. Hedges meeting

the criteria for hedge accounting are accounted for as follows:

Fair value hedges

The change in fair value of a hedging derivative is recognized in profit or

loss. The change in the fair value of the hedged item attributable to the

risk being hedged is recorded as part of the carrying value of the hedged

item and is also recognized in profit or loss.

The group applies fair value hedge accounting for hedging fixed

interest rate risk on borrowings. The gain or loss relating to the effective

portion of the interest rate swap is recognized in the income statement

within finance costs, offsetting the amortization of the interest on the

underlying borrowings.

If the criteria for hedge accounting are no longer met, or if the

group revokes the designation, the adjustment to the carrying amount of

ea hedged item for which the effective interest rate method is used is

amortized to profit or loss over the period to maturity.

Cash flow hedges

For cash flow hedges, the effective portion of the gain or loss on the

hedging instrument is recognized within other comprehensive income,

while the ineffective portion is recognized in profit or loss. Amounts

taken to equity are transferred to the income statement when the

hedged transaction affects profit or loss. The gain or loss relating to the

effective portion of interest rate swaps hedging variable rate borrowings

is recognized in the income statement within finance costs.

Where the hedged item is the cost of a non-financial asset or

liability, such as a forecast transaction for the purchase of property, plant

and equipment, the amounts recognized within other comprehensive

income are transferred to the initial carrying amount of the non-financial

asset or liability.

If the hedging instrument expires or is sold, terminated or

exercised without replacement or rollover, or if its designation as a hedge

is revoked, amounts previously recognized within other comprehensive

income remain in equity until the forecast transaction occurs and are

transferred to the income statement or to the initial carrying amount of a

non-financial asset or liability as above. If a forecast transaction is no

longer expected to occur, amounts previously recognized in equity are

reclassified to the income statement.

120

BP Annual Report and Accounts 2009

Notes on financial statements