Avon 2004 Annual Report Download - page 21

Download and view the complete annual report

Please find page 21 of the 2004 Avon annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

|

|

Net cash provided by operating activities

reached a record level of $882.6 in 2004,

$137.3 favorable to 2003.

Liquidity and Capital Resources

Avon’s principal sources of funds historically have been

cash flows from operations, commercial paper and bor-

rowings under lines of credit. Management believes that

cash from operations and available sources of financing

are adequate to meet anticipated requirements for

working capital, dividends, capital expenditures, the

stock repurchase program and other cash needs.

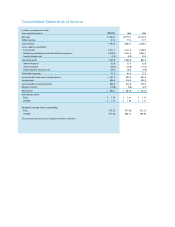

Balance Sheet Data 2004 2003

Cash and cash equivalents $ 769.6 $ 694.0

Total debt 918.0 1,121.8

Working capital 980.9 619.1

Cash Flows2004 2003 2002

Net cash provided by

operating activities $ 882.6 $ 745.3 $ 565.4

Net cash used by

investing activities (279.4) (178.4) (123.0)

Net cash used by financing

activities (567.0) (495.5) (331.8)

Effect of exchange rate

changes on cash

and equivalents 39.4 15.8 (12.3)

Net Cash Provided by Operating Activities

Net cash provided by operating activities in 2004 was $137.3

favorable to 2003 principally reflecting the following:

• Higher net income (adjusted for non-cash items), and

• Favorable working capital levels in accounts payable

and accrued expenses, including lower cash outlays in

2004 for bonus and restructuring payments, as well as a

higher number of accounts payable days outstanding.

These sources of cash were partially offset by the following:

• Unfavorable working capital levels in accounts

receivable and inventories, primarily reflecting

higher sales in 2004, as well as an increase in inven-

tory days outstanding (increase of 1 day in 2004 ver-

sus 2003 as compared to a decrease of 7 days in 2003

versus 2002),

• Higher contributions to the U.S. qualified pension

plan ($90.0 in 2004 versus $60.0 in 2003), and

• Higher tax audit settlement payments ($71.2 in 2004

versus $45.1 in 2003).

Avon maintains qualified defined benefit pension plans

and unfunded supplemental pension benefit plans (see

Note 10, Employee Benefit Plans). Avon’s funding policy for

these plans is based on legal requirements and cash flows.

The amounts necessary to fund future obligations under

these plans could vary depending on estimated assump-

tions (as detailed in “Critical Accounting Estimates”). The

future funding for these plans will depend on economic

conditions, employee demographics, mortality rates, the

number of associates electing to take lump-sum distribu-

tions, investment performance and funding decisions.

Based on current assumptions, Avon expects to contribute

approximately $85.0 and $37.0, respectively, to its U.S. and

international pension plans in 2005.

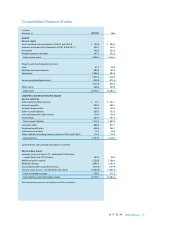

Inventories of $740.5 at December 31, 2004 were higher

than $653.4 at December 31, 2003. It is Avon’s objective to

continue to focus on inventory management. However,

the addition or expansion of product lines, which are sub-

ject to changing fashion trends and consumer tastes, as

well as planned expansion in high growth markets, may

cause inventory levels to grow periodically.

Net Cash Used by Investing Activities

Net cash used by investing activities in 2004 was $101.0

higher than in 2003 resulting from the following:

• Higher capital expenditures and

• The purchase in 2004 of additional shares in its two

subsidiaries in China for $45.6 as compared to the

purchase in 2003 of the outstanding shares in Avon’s

Turkish business for $18.4 (see Note 17, Acquisitions).

Capital expenditures during 2004 were $250.1 compared

with $162.6 in 2003. The increase in capital spending was

primarily driven by continued investments for capacity

expansion (primarily a new manufacturing facility in

Russia), facility modernization (primarily the construction

of a new research and development facility in the U.S.),

and improvements to existing facilities, information sys-

tems and equipment replacement projects. Numerous

construction and information systems projects were in

progress at December 31, 2004, with an estimated cost to

complete of approximately $135.0. Capital expenditures

in 2005 are currently expected to be approximately

$280.0 and will be funded by cash from operations. These

expenditures will include continued investments for

capacity expansion, facility modernization (primarily the

continuation of construction of the new research and

development facility in the U.S.), information systems

(including the development of the ERP project previously

discussed) and equipment replacement projects.