Abercrombie & Fitch 2011 Annual Report Download - page 91

Download and view the complete annual report

Please find page 91 of the 2011 Abercrombie & Fitch annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

|

|

ABERCROMBIE & FITCH CO.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

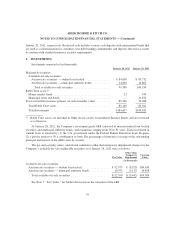

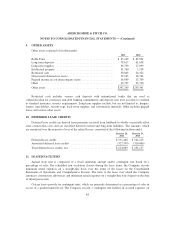

not that these net operating loss carryovers will reduce future years’ tax liabilities in certain foreign

jurisdictions less the associated valuation allowance. As of January 28, 2012 and January 29, 2011, the

foreign subsidiaries’ net operating valuation allowances totaled $2.5 million and $0.0, respectively.

No other valuation allowances have been provided for deferred tax assets because management

believes that it is more likely than not that the full amount of the net deferred tax assets will be realized in

the future.

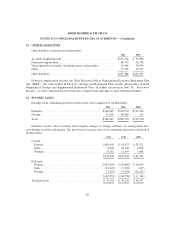

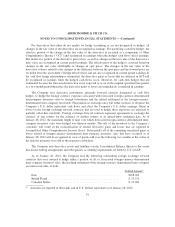

2011 2010 2009

(In thousands)

Unrecognized tax benefits, beginning of the year ......... $14,827 $ 29,437 $ 43,684

Gross addition for tax positions of the current year ........ 1,183 562 222

Gross addition for tax positions of prior years ........... 1,602 1,734 2,167

Reductions of tax positions of prior years for:

Lapses of applicable statutes of limitations ............ (2,448) (2,328) (448)

Settlements during the period ...................... (1,631) (14,166) (5,444)

Changes in judgment ............................. (129) (412) (10,744)

Unrecognized tax benefits, end of year ................. $13,404 $ 14,827 $ 29,437

The amount of the above unrecognized tax benefits at January 28, 2012, January 29, 2011 and

January 30, 2010 which would impact the Company’s effective tax rate, if recognized, was $13.4 million,

$14.8 million and $29.4 million, respectively.

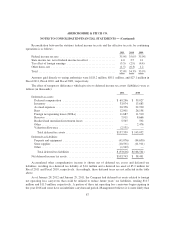

The Company recognizes accrued interest and penalties related to unrecognized tax benefits as a

component of income tax expense. Tax expense for Fiscal 2011 includes a $0.7 million increase of net

accrued interest, compared to a $3.4 million reduction of net accrued interest as of the end of Fiscal 2010.

Interest and penalties of $6.1 million had been accrued, at the end of Fiscal 2011, compared to $6.2 million

accrued at the end of Fiscal 2010.

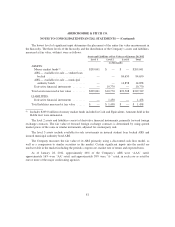

The Internal Revenue Service (“IRS”) is currently conducting an examination of the Company’s U.S.

federal income tax return for Fiscal 2011 as part of the IRS’s Compliance Assurance Process program. IRS

examinations for Fiscal 2010 and prior years have been completed and settled. State and foreign returns are

generally subject to examination for a period of three-five years after the filing of the respective return. The

Company has various state income tax returns in the process of examination or administrative appeals.

The Company does not expect material adjustments to the total amount of unrecognized tax benefits

within the next 12 months, but the outcome of tax matters is uncertain and unforeseen results can occur.

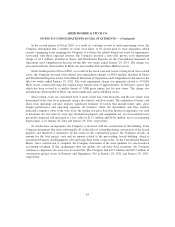

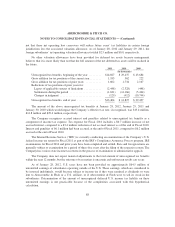

As of January 28, 2012, U.S. taxes have not been provided on approximately $64.5 million of

unremitted earnings of subsidiaries operating outside of the U.S. These earnings, which are considered to

be invested indefinitely, would become subject to income tax if they were remitted as dividends or were

lent to Abercrombie & Fitch or a U.S. affiliate, or if Abercrombie & Fitch were to sell its stock in the

subsidiaries. Determination of the amount of unrecognized deferred U.S. income tax liability on these

unremitted earnings is not practicable because of the complexities associated with this hypothetical

calculation.

88