Abercrombie & Fitch 2011 Annual Report Download - page 83

Download and view the complete annual report

Please find page 83 of the 2011 Abercrombie & Fitch annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

|

|

ABERCROMBIE & FITCH CO.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

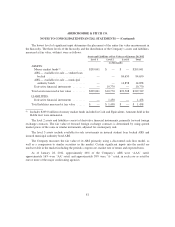

An impairment is considered to be other-than-temporary if an entity (i) intends to sell the security,

(ii) more likely than not will be required to sell the security before recovering its amortized cost basis, or

(iii) does not expect to recover the security’s entire amortized cost basis, even if there is no intent to sell the

security. During the fifty-two weeks ended January 28, 2012, the Company changed its intent regarding the

sale of its ARS, resulting in recognition of an other-than-temporary impairment of $13.4 million recorded

in other expense.

The irrevocable rabbi trust (the “Rabbi Trust”) is intended to be used as a source of funds to match

respective funding obligations to participants in the Abercrombie & Fitch Co. Nonqualified Savings and

Supplemental Retirement Plan I, the Abercrombie & Fitch Co. Nonqualified Savings and Supplemental

Retirement Plan II and the Chief Executive Officer Supplemental Executive Retirement Plan. The Rabbi

Trust assets are consolidated and recorded at fair value, with the exception of the trust-owned life insurance

policies which are recorded at cash surrender value. The Rabbi Trust assets are included in Other Assets on

the Consolidated Balance Sheets and are restricted as to their use as noted above. During the fifty-two

weeks ended January 28, 2012, the Company sold $11.6 million of municipal notes and bonds at an

immaterial realized loss. The proceeds from the sale of the municipal notes and bonds, along with money

market funds on hand, were used to purchase an additional $12.3 million in insurance policies. The change

in cash surrender value of the trust-owned life insurance policies held in the Rabbi Trust resulted in

realized gains of $2.5 million and $2.3 million for the fifty-two weeks ended January 28, 2012 and

January 29, 2011, respectively, recorded as part of Interest Expense, Net on the Consolidated Statements of

Operations and Comprehensive Income.

7. FAIR VALUE

Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly

transaction between market participants at the measurement date. The inputs used to measure fair value are

prioritized based on a three-level hierarchy. The three levels of inputs to measure fair value are as follows:

• Level 1 — inputs are unadjusted quoted prices for identical assets or liabilities that are available in

active markets.

• Level 2 — inputs are other than quoted market prices included within Level 1 that are observable

for assets or liabilities, directly or indirectly.

• Level 3 — inputs to the valuation methodology are unobservable.

80