Abercrombie & Fitch 2011 Annual Report Download - page 57

Download and view the complete annual report

Please find page 57 of the 2011 Abercrombie & Fitch annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

|

|

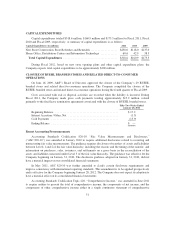

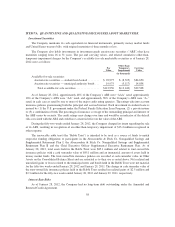

Policy Effect if Actual Results Differ from Assumptions

Inventory Valuation

Inventories are principally valued at the lower of

average cost or market utilizing the retail method.

The Company reduces inventory value by recording a

valuation reserve that represents estimated future

permanent markdowns necessary to sell-through the

inventory. The valuation reserve can fluctuate

depending on the timing of markdowns previously

recognized.

Additionally, as part of inventory valuation, an

inventory shrink estimate is made each period that

reduces the value of inventory for lost or stolen

items.

The Company has not made any material changes

in the accounting methodology used to determine

the shrink reserve or the valuation reserve over the

past three fiscal years.

The Company does not expect material changes in

the near term to the underlying assumptions used

to determine the shrink reserve or valuation

reserve as of January 28, 2012. However, changes

in these assumptions do occur, and, should those

changes be significant, they could significantly

impact the ending inventory valuation at cost, as

well as the resulting gross margin(s).

An increase or decrease in the valuation reserve of

10% would have affected pre-tax income by

approximately $7.2 million for Fiscal 2011.

An increase or decrease in the inventory shrink

accrual of 10% would have been immaterial to

pre-tax income for Fiscal 2011.

54