Abercrombie & Fitch 2011 Annual Report Download - page 86

Download and view the complete annual report

Please find page 86 of the 2011 Abercrombie & Fitch annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

|

|

ABERCROMBIE & FITCH CO.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

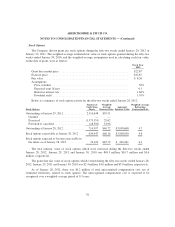

In the second quarter of Fiscal 2010, as a result of a strategic review of under-performing stores, the

Company determined that a number of stores were likely to be closed prior to lease expiration, which

caused a triggering event requiring the Company to evaluate the related long-lived assets for impairment.

Associated with these expected closures, the Company incurred a non-cash, pre-tax asset impairment

charge of $2.2 million, included in Stores and Distribution Expense on the Consolidated Statement of

Operations and Comprehensive Income for the fifty-two weeks ended January 29, 2011. The charge was

associated with one Abercrombie & Fitch, one abercrombie kids and three Hollister stores.

In the fourth quarter of Fiscal 2010, as a result of the fiscal year-end review of long-lived store-related

assets, the Company incurred store-related asset impairment charges of $48.4 million, included in Stores

and Distribution Expense on the Consolidated Statement of Operations and Comprehensive Income for the

fifty-two weeks ended January 29, 2011. The asset impairment charge was primarily related to 13 Gilly

Hicks stores constructed using the original large format store of approximately 10,000 gross square feet

which has been revised to a smaller format of 5,000 gross square feet for new stores. The charge also

included one Abercrombie & Fitch, one abercrombie kids and six Hollister stores.

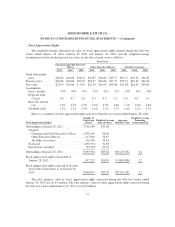

Store-related assets are considered level 3 assets in the fair value hierarchy and the fair values were

determined at the store level, primarily using a discounted cash flow model. The estimation of future cash

flows from operating activities requires significant estimates of factors that include future sales, gross

margin performance and operating expenses. In instances where the discounted cash flow analysis

indicated a negative value at the store level, the market exit price based on historical experience was used

to determine the fair value by asset type. Included in property and equipment, net, are store-related assets

previously impaired and measured at a fair value of $13.1 million and $14.6 million, net of accumulated

depreciation, as of January 28, 2012 and January 29, 2011, respectively.

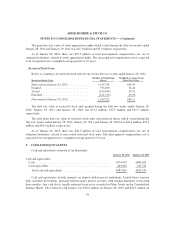

In certain lease arrangements, the Company is involved with the construction of the building. If the

Company determines that it has substantially all of the risks of ownership during construction of the leased

property and therefore is deemed to be the owner of the construction project, the Company records an

amount for the total project costs and an amount related to the pre-existing, leased building, which is

included in Property and Equipment, Net and Long-Term Debt, respectively, on the Consolidated Balance

Sheets. Once construction is complete, the Company determines if the asset qualifies for sale-leaseback

accounting treatment. If the arrangement does not qualify for sale-lease back treatment, the Company

continues to depreciate the asset over its useful life. The Company had $47.5 million and $16.5 million of

construction project assets in Property and Equipment, Net at January 28, 2012 and January 29, 2011,

respectively.

83