Abercrombie & Fitch 2009 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2009 Abercrombie & Fitch annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

|

|

following policies and estimates are most critical to the portrayal of the Company’s financial condition and

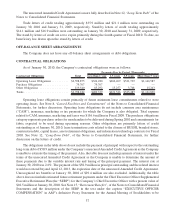

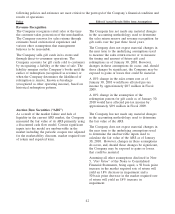

results of operations.

Policy Effect if Actual Results Differ from Assumptions

Revenue Recognition

The Company recognizes retail sales at the time

the customer takes possession of the merchandise.

The Company reserves for sales returns through

estimates based on historical experience and

various other assumptions that management

believes to be reasonable.

The Company sells gift cards in its stores and

through direct-to-consumer operations. The

Company accounts for gift cards sold to customers

by recognizing a liability at the time of sale. The

liability remains on the Company’s books until the

earlier of redemption (recognized as revenue) or

when the Company determines the likelihood of

redemption is remote, known as breakage

(recognized as other operating income), based on

historical redemption patterns.

The Company has not made any material changes

in the accounting methodology used to determine

the sales return reserve and revenue recognition for

gift cards over the past three fiscal years.

The Company does not expect material changes in

the near term to the underlying assumptions used

to measure the sales return reserve or to measure

the timing and amount of future gift card

redemptions as of January 30, 2010. However,

changes in these assumptions do occur, and, should

those changes be significant, the Company may be

exposed to gains or losses that could be material.

A 10% change in the sales return rate as of

January 30, 2010 would have affected pre-tax

income by approximately $0.7 million in Fiscal

2009.

A 10% change in the assumption of the

redemption pattern for gift cards as of January 30,

2010 would have affected pre-tax income by

approximately $0.9 million in Fiscal 2009.

Auction Rate Securities (“ARS”)

As a result of the market failure and lack of

liquidity in the current ARS market, the Company

measured the fair value of its ARS primarily using

a discounted cash flow model. Certain significant

inputs into the model are unobservable in the

market including the periodic coupon rate adjusted

for the marketability discount, market required rate

of return and expected term.

The Company has not made any material changes

in the accounting methodology used to determine

the fair value of the ARS.

The Company does not expect material changes in

the near term to the underlying assumptions used

to determine the unobservable inputs used to

calculate the fair value of the ARS as of January

30, 2010. However, changes in these assumptions

do occur, and, should those changes be significant,

the Company may be exposed to gains or losses

that could be material.

Assuming all other assumptions disclosed in Note

5, “Fair Value” of the Notes to Consolidated

Financial Statements, being equal, a 50 basis point

increase in the market required rate of return will

yield an 18% decrease in impairment and a

50 basis point decrease in the market required rate

of return will yield an 18% increase in

impairment.

42