ADT 1999 Annual Report Download - page 57

Download and view the complete annual report

Please find page 57 of the 1999 ADT annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

-

69

-

70

-

71

-

72

|

|

55

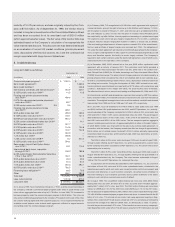

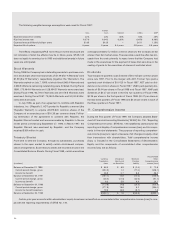

12. Charge for the Impairment of

Long-Lived Assets

Charges for the impairment of long-lived assets are as follows:

Nine Months

Ended

Year Ended September 30,

September 30,

(in millions) 1999 1998 1997

Telecommunications and

Electronics $259.0 $

—

$

—

Healthcare and Specialty

Products 76.0

——

Fire and Security Services

——

118.8

Flow Control Products

——

29.6

$335.0 $

—

$148.4

Effective January 1, 1996, the Company adopted Statement of

Financial Accounting Standards No. 121, “Accounting for the Impair-

ment of Long-Lived Assets and Long-Lived Assets to Be Disposed Of”

(“SFAS 121”). SFAS 121 requires the recoverability of the carrying

value of long-lived assets, primarily property, plant and equipment and

related goodwill and other intangible assets, to be reviewed for impair-

ment whenever events or changes in circumstances indicate that the

carrying amount of an asset may not be fully recoverable. Under

SFAS 121 impairment losses are recognized when expected future

cash flows are less than the assets’ carrying value. When indicators of

impairment are present, the carrying values of the assets are evalu-

ated in relation to the operating performance and future undiscounted

cash flows of the underlying business. The net book value of the

underlying assets is adjusted to fair value if the sum of expected future

undiscounted cash flows is less than book value. Fair values are

based on quoted market prices and assumptions concerning the

amount and timing of estimated future cash flows and assumed dis-

count rates, reflecting varying degrees of perceived risk.

1999 Charges

The Telecommunications and Electronics segment recorded a charge

of $259.0 million in Fiscal 1999, which includes $198.2 million related

to the write-down of property, plant and equipment, primarily manu-

facturing and administrative facilities, associated with AMP’s world-

wide operations and the combination of facilities as a result of its

merger with the Company. It also includes an impairment in the value

of goodwill and other intangibles of $60.8 million resulting from the

combination of AMP’s electronics business with that of the Company

and AMP’s existing profit improvement plan.

The Healthcare and Specialty Products segment recorded a

charge of $76.0 million in Fiscal 1999 primarily relating to the write-

down of property, plant and equipment, principally administrative facil-

ities, associated with the consolidation of facilities in USSC’s

operations in the United States and Europe as a result of its merger

with the Company.

1997 Charges

The Fire and Security Services segment recorded a charge of

$118.8 million in Fiscal 1997, which includes $98.8 million related to

subscriber security systems installed at customers’ premises in the

United States and Canada, determined following a review of the car-

rying value of the assets. It also includes an impairment in the carry-

ing value of goodwill of $20.0 million resulting from the combination of

ADT’s electronic security business with that of Former Tyco.

The Flow Control Products segment recorded a charge of

$29.6 million in Fiscal 1997 reflecting an impairment in the carrying

value of goodwill resulting from the combination of Keystone’s valve

manufacturing and distribution business with that of Former Tyco.

13. Extraordinary Items

The extraordinary item in Fiscal 1999 of $45.7 million, net of tax ben-

efit of $18.0 million, primarily relates to the write-off of net unamortized

deferred financing costs related to the Company’s debt tender offers

(Note 4). The extraordinary item in Fiscal 1998 of $2.4 million, net of

tax benefit of $1.2 million, was the write-off of unamortized deferred

financing costs related to the LYONs (Note 4). During Fiscal 1997 the

Company reacquired in the market certain of its long-term debt which

was financed from cash on hand and borrowings under the Company’s

credit agreements. The extraordinary items in Fiscal 1997 of

$58.3 million, net of tax benefit of $33.0 million, included the loss

resulting from the reacquisition of these notes, and the write-off of

unamortized deferred refinancing costs and other related fees.

14. Cumulative Effect of Accounting Changes

The cumulative effect of accounting changes during Fiscal 1997 of

$15.5 million, net of tax of $7.4 million, related to AMP changing the

accounting practices used to develop inventory costs, including stan-

dardizing globally the definition of capacity used in determining over-

head rates and changing its inventory costing methodology to include

manufacturing engineering costs in inventory costs.