ADT 1999 Annual Report Download - page 44

Download and view the complete annual report

Please find page 44 of the 1999 ADT annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

|

|

42

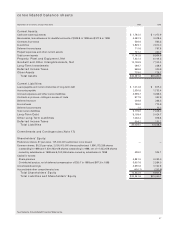

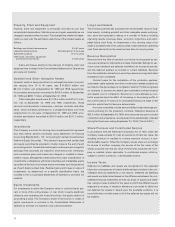

Property, Plant and Equipment

Property, plant and equipment is principally recorded at cost less

accumulated depreciation. Maintenance and repair expenditures are

charged to expense when incurred. The straight-line method of depre-

ciation is used over the estimated useful lives of the related assets as

follows:

Buildings and related improvements 5 to 50 years

Leasehold improvements Remaining term of the lease

Subscriber systems 10 to 14 years

Other plant, machinery, equipment

and furniture and fixtures 2 to 25 years

Gains and losses arising on the disposal of property, plant and

equipment are included in the Consolidated Statements of Operations

and were not material.

Goodwill and Other Intangible Assets

Goodwill, which is being amortized on a straight-line basis over peri-

ods ranging from 10 to 40 years, was $10,639.3 million and

$6,104.1 million, net, at September 30, 1999 and 1998, respectively.

Accumulated amortization amounted to $615.6 million at September

30, 1999 and $499.7 million at September 30, 1998.

Other intangible assets were $1,519.6 million and $1,001.4 mil-

lion, net, at September 30, 1999 and 1998, respectively. These

amounts include patents, trademarks, customer contracts and other

items, which are being amortized on a straight-line basis over lives

ranging from 2 to 40 years. At September 30, 1999 and 1998, accu-

mulated amortization amounted to $319.5 million and $207.1 million,

respectively.

Investments

The Company accounts for its long-term investments that represent

less than twenty percent ownership using Statement of Financial

Accounting Standards No. 115, “Accounting for Certain Investments in

Debt and Equity Securities.” This standard requires that certain debt

and equity securities be adjusted to market value at the end of each

accounting period. Unrealized market gains and losses are charged to

earnings if the securities are traded for short-term profit. Otherwise,

such unrealized gains and losses are charged or credited to share-

holders’ equity. Management determines the proper classification of

investments in obligations with fixed maturities and marketable equity

securities at the time of purchase and re-evaluates such designations

as of each balance sheet date. Realized gains and losses on sales of

investments, as determined on a specific identification basis, are

included in the Consolidated Statements of Operations and were not

material.

Equity Investments

For investments in which the Company owns or controls twenty per-

cent or more of the voting shares, or over which it exerts significant

influence over operating and financial policies, the equity method of

accounting is used. The Company’s share of net income or losses of

equity investments is included in the Consolidated Statements of

Operations and was not material in any period presented.

Long-Lived Assets

The Company periodically evaluates the net realizable value of long-

lived assets, including goodwill and other intangible assets and prop-

erty, plant and equipment, relying on a number of factors including

operating results, business plans, economic projections and antici-

pated future cash flows. An impairment in the carrying value of an

asset is assessed when the undiscounted, expected future operating

cash flows derived from the asset are less than its carrying value.

Revenue Recognition

Revenue from the sale of services or products is recognized as ser-

vices are rendered or shipments are made. Subscriber billings for ser-

vices not yet rendered are deferred and taken into income as earned,

and the deferred element is included in current liabilities. Revenue

from the installation of electronic security systems is recognized when

installations are completed.

Contract sales for the installation of fire protection systems,

underwater cable systems and other construction related projects are

recorded on the percentage-of-completion method. Profits recognized

on contracts in process are based upon estimated contract revenue

and related cost to completion. Revisions in cost estimates as con-

tracts progress have the effect of increasing or decreasing profits in

the current period. Provisions for anticipated losses are made in the

period in which they first become determinable.

Accounts receivable include amounts billed under retainage pro-

visions primarily for fire protection contracts. Retention balances of

$33.3 million at September 30, 1999, which become due upon contract

completion and acceptance, are expected to be substantially collected

during the fiscal year ending September 30, 2000 (“Fiscal 2000”).

Share Premium and Contributed Surplus

In accordance with the Bermuda Companies Act of 1981, when the

Company issues shares for cash at a premium to their par value, the

resulting premium is credited to a share premium account, a non-

distributable reserve. When the Company issues shares in exchange

for shares of another company, the excess of the fair value of the

shares acquired over the par value of the shares issued by the Com-

pany is credited, where applicable, to contributed surplus, which is,

subject to certain conditions, a distributable reserve.

Income Taxes

Deferred tax liabilities and assets are recognized for the expected

future tax consequences of events that have been included in the con-

solidated financial statements or tax returns. Deferred tax liabilities

and assets are determined based on the differences between the con-

solidated financial statements and the tax basis of assets and liabili-

ties, using tax rates in effect for the years in which the differences are

expected to reverse. A valuation allowance is provided to offset any

net deferred tax assets if, based upon the available evidence, it is

more likely than not that some or all of the deferred tax assets will not

be realized.