ADT 1999 Annual Report Download - page 32

Download and view the complete annual report

Please find page 32 of the 1999 ADT annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

|

|

30

earnings at the time the reserves are established. Amounts expended

for merger, restructuring and other non-recurring costs are charged

against the reserves as they are paid out. If the amount of the reserves

proves to be greater than the costs actually incurred, any excess is

credited against merger, restructuring and other non-recurring

charges in the Consolidated Statement of Operations in the period in

which that determination is made.

In Fiscal 1999, the Company established merger, restructuring

and other non-recurring reserves of $434.9 million in connection with

its merger with USSC and $841.8 million in connection with its merger

with AMP. At the beginning of the fiscal year, there existed merger,

restructuring and other non-recurring reserves of $303.7 million

related to pooling of interests transactions consummated in prior

years and other restructuring charges taken by the merged companies

prior to their combination with the Company. During Fiscal 1999, the

Company paid out $633.6 million in cash and incurred $478.5 million

in non-cash charges that were charged against these reserves. Also

in Fiscal 1999, the Company determined that $15.0 million of merger,

restructuring and other non-recurring reserves established in prior

years was not needed and deducted that amount from the merger,

restructuring and other non-recurring charges for Fiscal 1999. At Sep-

tember 30, 1999, there remained $453.3 million of merger, restructur-

ing and other non-recurring reserves on the Company’s Consolidated

Balance Sheet, of which $366.3 million is included in current liabilities

and $87.0 million is included in long-term liabilities. The Company

expects to pay out approximately $350.0 million in cash in Fiscal 2000

for merger, restructuring and other non-recurring expenses that will be

charged against these reserves.

All other business combination transactions completed in Fiscal

1999 were required to be accounted for under the purchase account-

ing method. At the time each purchase acquisition is made, the Com-

pany establishes a reserve for transaction costs and the costs of

integrating each purchased company within the relevant Tyco busi-

ness segment. The amounts of such reserves established in Fiscal

1999 are detailed in Note 3 to the Consolidated Financial Statements.

These amounts are not charged against current earnings but are

treated as additional purchase price consideration and have the effect

of increasing the amount of goodwill recorded in connection with the

respective acquisition. Indeed, management views these costs as the

equivalent of additional purchase price consideration when it consid-

ers making an acquisition. If the amount of the reserves proves to be

in excess of costs actually incurred, any excess goes to reduce the

goodwill account that was established at the time the acquisition was

made.

In Fiscal 1999, the Company made acquisitions that were

accounted for under the purchase accounting method at an aggregate

cost of $6,923.3 million. Of this amount, $4,546.8 million was paid in

cash (net of cash acquired), $1,449.6 million was paid in the form of

Tyco common shares, and the Company assumed $926.9 million in

debt. In connection with these acquisitions, the Company established

purchase accounting reserves of $525.4 million for transaction and

integration costs. At the beginning of Fiscal 1999, purchase account-

ing reserves were $505.6 million as a result of purchase accounting

transactions made in prior years. During Fiscal 1999, the Company

paid out $354.4 million in cash and incurred $16.3 million in non-cash

charges against the reserves established during and prior to Fiscal

1999. Also in Fiscal 1999, the Company determined that $90.0 million

of purchase accounting reserves related to acquisitions prior to Fiscal

1999 were not needed and reversed that amount against goodwill. At

September 30, 1999, there remained $570.3 million in purchase

accounting reserves on the Company’s Consolidated Balance Sheet,

of which $408.0 million is included in current liabilities and $162.3 mil-

lion is included in long-term liabilities. The Company expects to pay

out approximately $350.0 million in cash in Fiscal 2000 that will be

charged against these purchase accounting reserves.

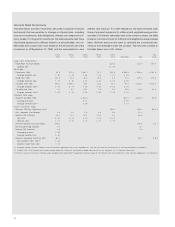

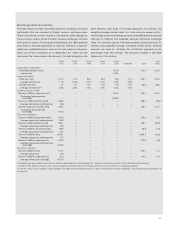

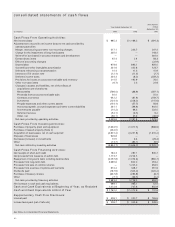

The following details the Fiscal 1999 capital expenditures and

depreciation by segment:

Capital

(in millions) Expenditures Depreciation

Telecommunications and Electronics $ 488.5 $446.2

Healthcare and Specialty Products 235.9(1) 179.3

Fire and Security Services 746.3 262.2

Flow Control Products 135.1 87.0

Corporate 26.7 4.9

Total $1,632.5 $979.6

(1) Excludes $234.0 million related to the purchase of leased property in connection with

the merger with USSC.

The Company continues to fund capital expenditures to improve

the cost structure of its businesses, to invest in new processes and

technology, and to maintain high quality production standards. The

level of capital expenditures for the Fire and Security Services seg-

ment significantly exceeded, and is expected to continue to signifi-

cantly exceed, depreciation due to the large volume growth of new

residential subscriber systems capitalized. The level of capital expen-

ditures in the other segments is expected to increase moderately in

Fiscal 2000. The source of funds for capital expenditures is expected

to be cash from operating activities.

The provision for income taxes in the Consolidated Statement of

Operations for Fiscal 1999 was $620.2 million, but the amount of

income taxes paid (net of refunds) during the year was only $209.7 mil-

lion. After adjustment for deferred income taxes of acquired compa-

nies and other items, the net increase in deferred income taxes was

$334.3 million. The increase in deferred income taxes is attributable

primarily to current utilization of deductions on restructuring, other

non-recurring charges and purchase accounting spending, other tim-

ing differences between book and tax recognition of income and

expense, utilization of net operating loss and credit carryforwards, and

the tax benefits of stock option exercises.

The net change in working capital, net of the effects of acquisi-

tions and divestitures, was an increase of $85.5 million. These

changes are set forth in detail in the Consolidated Statement of Cash

Flows. The increase in working capital accounts is attributable to the

higher level of business activity in Fiscal 1999 as reflected in the

increased sales over the prior year. Management focuses on maxi-

mizing the cash flow from its operating businesses and attempts to

keep the working capital employed in the businesses to the minimum

level required for efficient operations.

In addition, the Company used $234.0 million of cash to purchase

the USSC North Haven facilities and $637.8 million to purchase its

own common shares. The Company repurchases its own shares from