ADT 1999 Annual Report Download - page 35

Download and view the complete annual report

Please find page 35 of the 1999 ADT annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

|

|

33

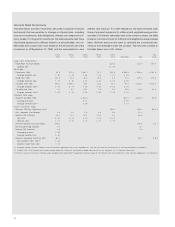

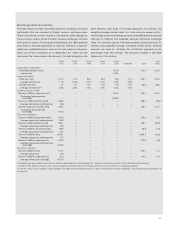

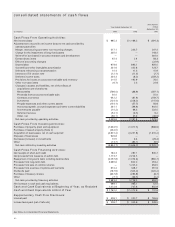

Exchange Rate Sensitivity

The table below provides information about the Company’s financial

instruments that are sensitive to foreign currency exchange rates.

These instruments include long-term investments, debt obligations,

cross-currency swaps, forward foreign currency exchange contracts

and currency options. For long-term investments, the table presents

cash flows of principal payments (in millions) related to a subordi-

nated, non-collateralized zero coupon loan note, based on the amor-

tized cost of the investment as of September 30, 1999, and the

associated fair value interest rate discount. For debt obligations, the

table presents cash flows of principal repayment (in millions) and

weighted average interest rates. For cross-currency swaps and for-

ward foreign currency exchange contracts, the table presents notional

amounts (in millions) and weighted average contractual exchange

rates. For currency options, the table presents notional amounts (in

millions) and weighted average contractual strike prices. Notional

amounts are used to calculate the contractual payments to be

exchanged under the contract. The amounts included in the table

below are in U.S. dollars.

Fiscal Fiscal Fiscal Fiscal Fiscal Fair

2000 2001 2002 2003 2004 Thereafter Total Value

Long-term investment:

Fixed Rate (British Pound)

————

120.5

—

120.5 120.5

Interest rate 11.5%

Long-term debt:

Fixed rate (Yen) 127.3 17.3 34.3 18.3 6.9 71.0 275.1 275.4

Average interest rate 1.7% 2.3% 2.2% 2.4% 2.0% 4.5%

Variable rate (Yen) 4.7 5.7 14.1 5.6 3.3 13.2 46.6 46.6

Average interest rate(1) 2.3% 2.3% 2.3% 2.3% 2.3% 2.3%

Cross-currency swap:

Receive US$/Pay Japanese Yen(2)

————

150.0

—

150.0 0.4(3)

Contractual exchange rate

(Yen/US$)

————

105.95

—

Receive US$/Pay British Pound 208.2

—————

208.2 (8.8)(3)

Average contractual exchange rate 1.58

—————

Receive Japanese Yen/Pay US$ 89.7

—————

89.7 4.4(3)

Contractual exchange rate

(Yen/US$) 111.50

Forward contracts:

Receive US$/Pay Australian Dollar 224.3

—————

224.3 (0.7)

Average contractual exchange rate 0.65

—————

Receive US$/Pay British Pound 766.7

—————

766.7 (26.3)

Average contractual exchange rate 1.59

—————

Receive US$/Pay Canadian Dollar 49.6

—————

49.6 (1.2)

Average contractual exchange rate 0.67

—————

Receive US$/Pay Euro 1,534.1

—————

1,534.1 (23.0)

Average contractual exchange rate 1.07

—————

Receive US$/Pay Japanese Yen 142.6

—————

142.6 (1.5)

Average contractual exchange rate

(Yen/US$) 103.62

—————

Currency options:

Receive US$/Pay Euro 100.0

—————

100.0 0.4

Average strike price 1.00

—————

Receive US$/Pay Japanese Yen 60.0

—————

60.0 0.3

Average strike price (Yen/US$) 119.75

—————

(1) Weighted average variable interest rates are based on applicable rates as of September 30, 1999 per the terms of the contracts of the related financial instruments.

(2) In March 1994, AMP entered into a cross-currency swap with a financial institution to hedge a portion of its net investment in its Japanese subsidiary.

(3) The fair values of cross-currency swaps included in the table reflect the portion of the fair values of the contracts that are attributable to the foreign currency component of

the contracts.