Seagate 2006 Annual Report Download - page 87

Download and view the complete annual report

Please find page 87 of the 2006 Seagate annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

Table of Contents

SEAGATE TECHNOLOGY

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

The $322 million reduction in the Maxtor goodwill was required in accordance with SFAS No. 109, Accounting

for Income Taxes

(“SFAS No. 109”) as a result of the reversal of valuation allowance that had been previously

recorded as of the date of acquisition against Maxtor related deferred tax assets primarily for tax net operating loss

carryovers. The valuation allowance was reduced primarily to reflect the realization of acquired Maxtor net operating

loss carry forwards due to increased forecasts of future U.S. taxable income and a $296 million gain for U.S. tax

purposes from the intercompany sale of certain intellectual property rights to a foreign subsidiary. Approximately

$120 million of tax expense associated with the gain on the intercompany sale of intangibles has been capitalized in

accordance with Accounting Research Bulletin No. 51, Consolidated Financial Statements (“ARB No. 51”) and is

being amortized to income tax expense over a sixty-

month period, which approximates the expected useful life of the

intangibles sold in the intercompany transaction.

As of June 29, 2007, the valuation allowance recorded was $399 million. Approximately $22 million relates to

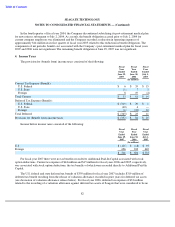

deferred tax assets acquired in the Maxtor transaction for which the related benefit will be credited directly to

goodwill when and if realized. The net decrease in the valuation allowance in fiscal 2007 was $580 million. In fiscal

years 2006 and 2005, the valuation allowance increased by $327 million and $111 million respectively.

At June 29, 2007, the Company had recorded $768 million of net deferred tax assets. The realization of

$663 million of these deferred tax assets is primarily dependent on the Company generating sufficient U.S. and

certain foreign taxable income in future periods. Although realization is not assured, the Company’s management

believes that it is more likely than not these deferred tax assets will be realized. The amount of deferred tax assets

considered realizable, however, may increase or decrease, when the Company reevaluates the underlying basis for its

estimates of future U.S. and certain foreign taxable income.

At June 29, 2007, the Company had U.S. federal, state and foreign tax net operating loss carryforwards of

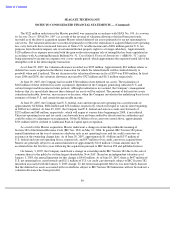

approximately $2 billion, $886 million and $534 million, respectively, which will expire at various dates beginning

in 2008 if not utilized. At June 29, 2007, the Company had U.S. federal and state tax credit carryforwards of

$232 million and $68 million, respectively, which will expire at various dates beginning in 2008, if not utilized.

These net operating losses and tax credit carryforwards have not been audited by the relevant tax authorities and

could be subject to adjustment on examination. Of the $2 billion of loss carryovers noted above, approximately

$591 million will be credited to Additional Paid-in Capital upon recognition.

As a result of the Maxtor acquisition, Maxtor underwent a change in ownership within the meaning of

Section 382 of the Internal Revenue Code (IRC Sec. 382) on May 19, 2006. In general, IRC Section 382 places

annual limitations on the use of certain tax attributes such as net operating losses and tax credit carryovers in

existence at the ownership change date. As of June 29, 2007, approximately $1.4 billion and $337 million of

U.S. federal and state net operating losses, respectively, and $47 million of tax credit carryovers acquired from

Maxtor are generally subject to an annual limitation of approximately $110 million. Certain amounts may be

accelerated into the first five years following the acquisition pursuant to IRC Section 382 and published notices.

On January 3, 2005, the Company underwent a change in ownership under IRC Section 382 due to the sale of

common shares to the public by its then largest shareholder, New SAC. Based on an independent valuation as of

January 3, 2005, the annual limitation for this change is $44.8 million. As of June 29, 2007, there is $447 million of

U.S. net operating loss carryforwards and $111 million of U.S. tax credit carryforwards subject to IRC Section 382

limitation associated with the January 3, 2005 change. To the extent management believes it is more likely than not

that the deferred tax assets associated with tax attributes subject to IRC Section 382 limitations will not be realized, a

valuation allowance has been provided.

84