HSBC 2012 Annual Report Download - page 56

Download and view the complete annual report

Please find page 56 of the 2012 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

|

|

HSBC HOLDINGS PLC

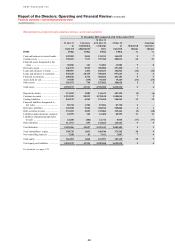

Report of the Directors: Operating and Financial Review (continued)

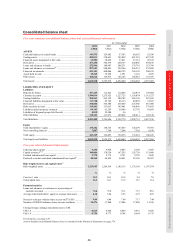

Financial summary > Critical accounting policies

54

Critical accounting policies

(Audited)

Introduction

The results of HSBC are sensitive to the accounting

policies, assumptions and estimates that underlie the

preparation of our consolidated financial statements.

The significant accounting policies are described in

Note 2 on the Financial Statements.

The accounting policies that are deemed critical

to our results and financial position, in terms of the

materiality of the items to which the policies are

applied and the high degree of judgement involved,

including the use of assumptions and estimation, are

discussed below.

Impairment of loans and advances

Our accounting policy for losses arising from the

impairment of customer loans and advances is

described in Note 2g on the Financial Statements.

Loan impairment allowances represent

management’s best estimate of losses incurred

in the loan portfolios at the balance sheet date.

Management is required to exercise judgement

in making assumptions and estimates when

calculating loan impairment allowances on both

individually and collectively assessed loans and

advances.

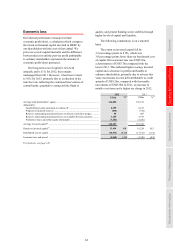

The majority of the collectively assessed loan

impairment allowances are in North America, where

they were US$5.2bn, representing 54% (2011:

US$6.8bn; 62%) of the Group’s total collectively

assessed loan impairment allowances and 32% of the

Group’s total impairment allowances. Of the North

American collective impairment allowances

approximately 86% (2011: 75%) related to the

US CML portfolio.

The methods used to calculate collective

impairment allowances on homogeneous groups

of loans and advances that are not considered

individually significant are disclosed in Note 2g

on the Financial Statements. They are subject to

estimation uncertainty, in part because it is not

practicable to identify losses on an individual loan

basis because of the large number of individually

insignificant loans in the portfolio.

The estimation methods include the use of

statistical analyses of historical information,

supplemented with significant management

judgement, to assess whether current economic and

credit conditions are such that the actual level of

inherent losses is likely to be greater or less than

that suggested by historical experience. Where

changes in economic, regulatory or behavioural

conditions result in the most recent trends in

portfolio risk factors being not fully reflected in the

statistical models, risk factors are taken into account

by adjusting the impairment allowances derived

solely from historical loss experience.

Risk factors include loan portfolio growth,

product mix, unemployment rates, bankruptcy trends,

geographical concentrations, loan product features,

economic conditions such as national and local

trends in housing markets, the level of interest rates,

portfolio seasoning, account management policies

and practices, changes in laws and regulations, and

other influences on customer payment patterns.

Different factors are applied in different regions

and countries to reflect local economic conditions,

laws and regulations. The methodology and the

assumptions used in calculating impairment losses

are reviewed regularly in the light of differences

between loss estimates and actual loss experience.

For example, roll rates, loss rates and the expected

timing of future recoveries are regularly

benchmarked against actual outcomes to ensure

they remain appropriate.

In 2012, a portfolio risk factor adjustment of

US$225m was made to increase the collective

loan impairment allowances for our US mortgage

lending portfolios. The adjustment was made

following a review completed in the fourth quarter of

2012 which concluded that the estimated average

period of time from current status to write-off was

ten months for real estate loans (previously a period

of seven months was used). During 2013, this

revised estimate will be incorporated into the

statistical impairment allowance models.

Where loans are individually assessed for

impairment, management judgement is required in

determining whether there is objective evidence that

a loss event has occurred, and if so, the measurement

of the impairment allowance. In determining

whether there is objective evidence that a loss event

has occurred, judgement is exercised in evaluating

all relevant information on indicators of impairment,

which is not restricted to the consideration of

whether payments are contractually past-due but

includes broader consideration of factors indicating

deterioration in the financial condition and outlook

of borrowers affecting their ability to pay. A higher

level of judgement is required for loans to borrowers

showing signs of financial difficulty in market

sectors experiencing economic stress, particularly

where the likelihood of repayment is affected by the

prospects for refinancing or the sale of a specified

asset. For those loans where objective evidence of

impairment exists, management determine the size