HSBC 2012 Annual Report Download - page 255

Download and view the complete annual report

Please find page 255 of the 2012 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

263 -

264

264 -

265

265 -

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

|

|

253

Overview Operating & Financial Review Corporate Governance Financial Statements Shareholder Information

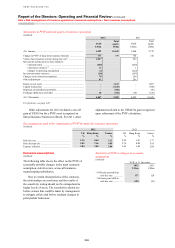

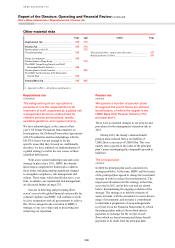

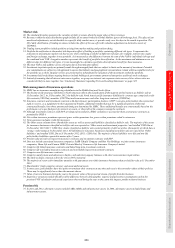

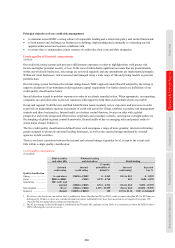

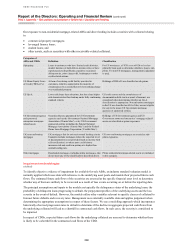

Principal objectives of our credit risk management

• to maintain across HSBC a strong culture of responsible lending and a robust risk policy and control framework;

• to both partner and challenge our businesses in defining, implementing and continually re-evaluating our risk

appetite under actual and scenario conditions; and

• to ensure there is independent, expert scrutiny of credit risks, their costs and their mitigation.

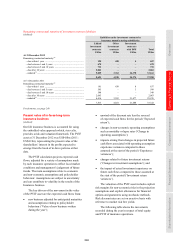

Credit quality of financial instruments

(Audited)

Our credit risk rating systems and processes differentiate exposures in order to highlight those with greater risk

factors and higher potential severity of loss. In the case of individually significant accounts that are predominantly

within our wholesale businesses, risk ratings are reviewed regularly and any amendments are implemented promptly.

Within our retail businesses, risk is assessed and managed using a wide range of risk and pricing models to generate

portfolio data.

Our risk rating system facilitates the internal ratings-based (‘IRB’) approach under Basel II adopted by the Group to

support calculation of our minimum credit regulatory capital requirement. For further details see definitions of our

credit quality classifications below.

Special attention is paid to problem exposures in order to accelerate remedial action. When appropriate, our operating

companies use specialist units to provide customers with support to help them avoid default wherever possible.

Group and regional Credit Review and Risk Identification teams regularly review exposures and processes in order

to provide an independent, rigorous assessment of credit risk across the Group, reinforce secondary risk management

controls and share best practice. Internal audit, as a tertiary control function, focuses on risks with a global

perspective and on the design and effectiveness of primary and secondary controls, carrying out oversight audits via

the sampling of global/regional control frameworks, themed audits of key or emerging risks and project audits to

assess major change initiatives.

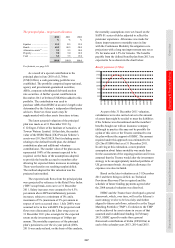

The five credit quality classifications defined below each encompass a range of more granular, internal credit rating

grades assigned to wholesale and retail lending businesses, as well as the external ratings attributed by external

agencies to debt securities.

There is no direct correlation between the internal and external ratings at granular level, except to the extent each

falls within a single quality classification.

Credit quality classification

(Unaudited)

Debt securities

and other bills Wholesale lending

and derivatives Retail lending

External

credit rating

Internal

credit rating

12 month

probability of

default %

Internal

credit rating1

Expected

loss %

Quality classification

Strong ........................... A– and above CRR1 to CRR2 0 – 0.169 EL1 to EL2 0 – 0.999

Good ............................ BBB+ to BBB– CRR3 0.170 – 0.740 EL3 1.000 – 4.999

Satisfactory .................. BB+ to B+ and

unrated

CRR4 to CRR5 0.741 – 4.914 EL4 to EL5 5.000 – 19.999

Sub-standard ................ B to C CRR6 to CRR8 4.915 – 99.999 EL6 to EL8 20.000 – 99.999

Impaired ....................... Default CRR9 to CRR10 100 EL9 to EL10 100+ or defaulted2

1 We observe the disclosure convention that, in addition to those classified as EL9 to EL10, retail accounts classified EL1 to EL8 that are

delinquent by 90 days or more are considered impaired, unless individually they have been assessed as not impaired (see page 156,

‘Past due but not impaired gross financial instruments’).

2 The EL percentage is derived through a combination of PD and LGD, and may exceed 100% in circumstances where the LGD is above

100% reflecting the cost of recoveries.