HSBC 2012 Annual Report Download - page 109

Download and view the complete annual report

Please find page 109 of the 2012 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

|

|

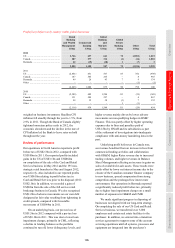

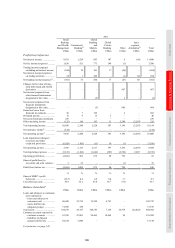

107

Overview Operating & Financial Review Corporate Governance Financial Statements Shareholder Information

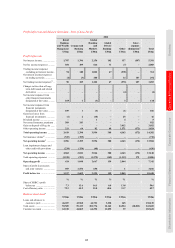

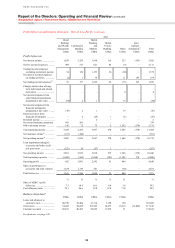

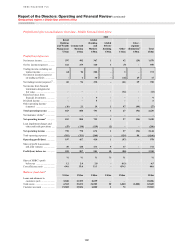

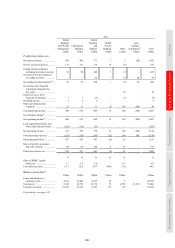

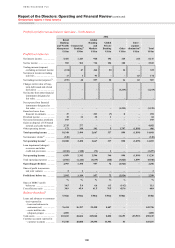

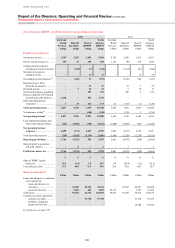

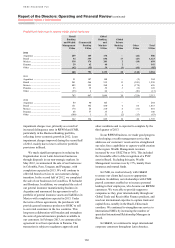

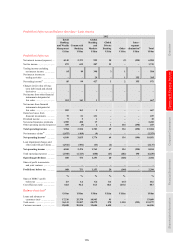

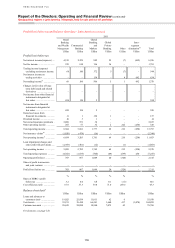

RBWM as long-term interest rates declined to a

lesser extent than in 2011. This was partly offset by

an increase from US$92m in 2011 to US$134m in

2012 of loss provisions for mortgage loan repurchase

obligations related to loans previously sold.

Net trading income increased in GB&M during

2012 as a result of the improved performance of

economic hedges used to manage interest rate risk,

which benefited from a more stable interest rate

environment. Rates revenue was higher due to

increased trading volumes. In addition, credit market

conditions generally reflected tighter credit spreads,

which led to higher income from our credit-related

products. These factors were partly offset by adverse

fair value movements on structured liabilities as own

credit spreads tightened, together with the closure of

our bank notes business in 2011, and a reduction in

foreign exchange revenue as a result of lower trading

volumes in less volatile markets.

Net loss from financial instruments designated

at fair value was US$1.2bn compared with net gains

of US$964m in 2011. We recognised adverse fair

value movements on our own debt designated at fair

value as credit spreads tightened during 2012, having

widened in 2011. In addition, there were adverse fair

value movements from interest rate ineffectiveness

in the economic hedging of our long-term debt

during the year.

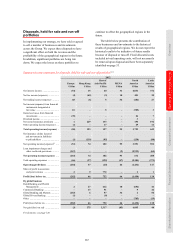

Gains on disposal of US branch network and

cards business included a gain of US$3.1bn from the

sale of the Card and Retail Services business and

US$864m from the sale of 195 retail branches in

upstate New York.

Other operating income increased by US$176m

to US$405m, reflecting lower losses on foreclosed

properties due to the reduction in foreclosure

activity, less deterioration in housing prices during

2012 and, in some markets, improvements in pricing

compared with 2011.

Loan impairment charges and other credit risk

provisions decreased by 51% to US$3.5bn, mainly in

the US, reflecting lower lending balances in CML as

we continued to run off the portfolio, and lower

delinquency levels. Loan impairment charges

remained adversely affected by delays in expected

cash flows from mortgage loans due, in part, to

delays in foreclosure processing and the higher costs

to obtain and realise collateral, although the effects

were less pronounced than in 2011. In addition, loan

impairment charges declined by US$1.3bn due to the

sale of the Card and Retail Services business. These

decreases were partly offset by an adjustment made

following a review completed in the fourth quarter of

2012 which concluded that the estimated average

period of time from current status to write-off was

ten months for real estate loans (previously a period

of seven months was used).

In CMB and GB&M, loan impairment charges

increased, mainly in Bermuda, due to individually

assessed impairments on a small number of

exposures. Credit quality in Canada remained

broadly unchanged.

Operating expenses increased by less than 1% to

US$8.9bn, primarily due to a US$1.5bn charge for

the settlement of investigations noted above.

Compliance costs increased by US$307m, mainly

due to investment in process enhancements and

infrastructure related to anti-money laundering and

Bank Secrecy Act consent orders, along with actions

to address the regulatory consent orders relating to

foreclosure activities. In addition, following a review

of our mortgage foreclosure process, we entered into

an agreement in principle with US regulators to pay

into a fund and provide other customer assistance to

help eligible borrowers who were active in

foreclosure during 2009 and 2010 and were

financially disadvantaged during the process, for

which we recognised a US$104m expense in 2012.

These increases were partly offset by the effect of

the sale of the Card and Retail Services business and

organisational effectiveness initiatives to reduce

costs as we achieved approximately US$230m of

additional sustainable cost savings primarily derived

from operational efficiencies. Average employee

numbers decreased from organisational effectiveness

initiatives and business disposals. In addition,

marketing costs fell and costs of holding foreclosed

properties declined, while software impairment

charges in 2011 did not recur.